|

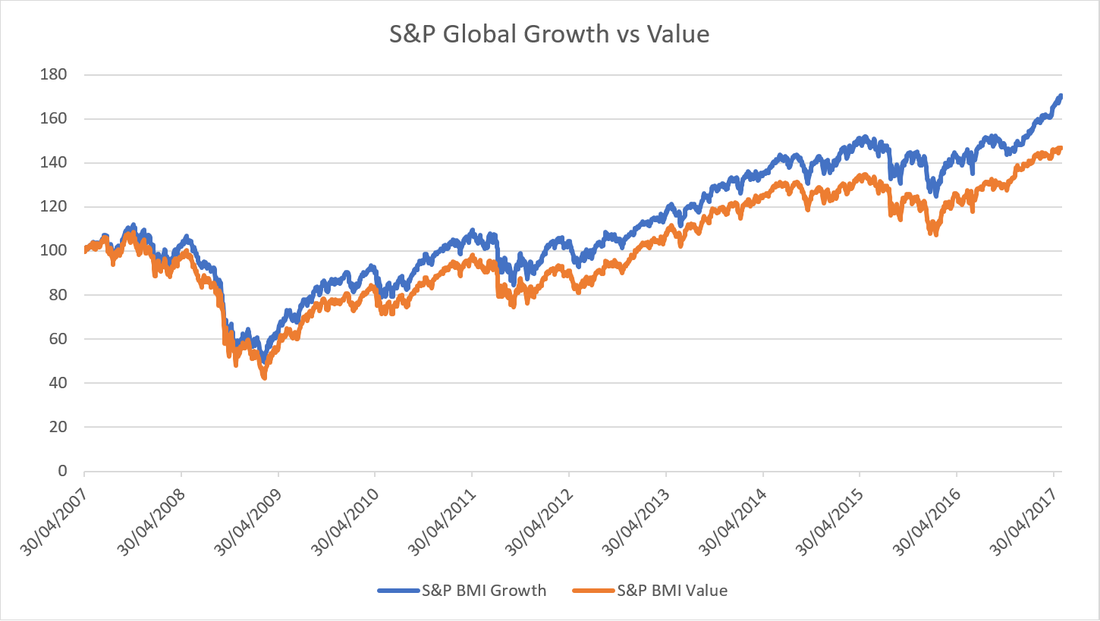

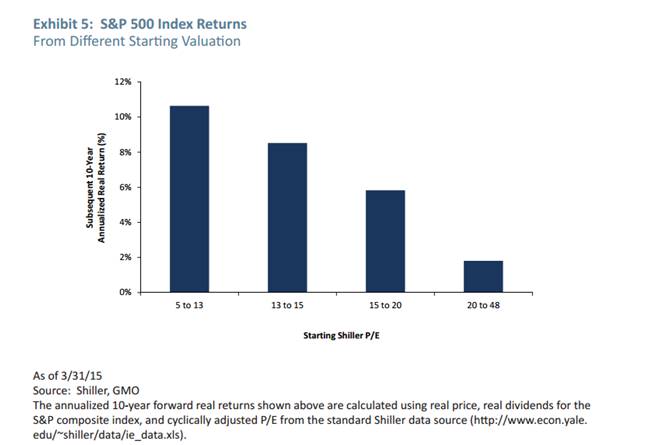

This week Robert Swift takes a look at how growth and value strategies have performed historically and how he sees them performing going forward. There is no “right way” to invest. Many approaches can work and many styles or philosophies (growth, small cap, value, contrarian etc) all have their moment in the sun. Some strategies work better than others in that they are both less volatile (work more often) and offer more opportunities to the active manager in so far as they better identify high stock return dispersions = the survivors win big and the losers lose all. The strategy which seems to work best and offer the most opportunity for active management is value. This value bias however comes at a price. While value investors expect to have the last laugh they sure miss out on a lot of laughs in the meantime. Put another way there is ultimately a risk and return benefit to being careful about the price you pay for investments, and for wanting dividends, but you do miss out on bragging rights at the cocktail party in that you probably don’t own a ‘sexy stock’. At the moment on a global basis, value is not in the sun but in the shade. We show the extent to which growth is currently more popular than value right now in the chart below. This traces the compound return of the S&P global growth index (blue) and the global value index (orange) in the last 10 years. Growth is ahead by a handy amount and so one would prefer to use a growth approach right? Probably wrong – you should never drive looking in the rear view mirror.  The logical conclusion actually, is that the value risk premium is now much higher than the growth risk premium. In other words, value stocks are more likely to outperform from here given relative valuations. The time series returns are starting point dependent so only going back 7 years would show value outperforming. It is this starting point dependency that illustrates the mean reversion of the styles. Going back 20+ years growth wins quite handily with about a +1% pa excess return over value. We try to show the benefits of having a value bias in the bar chart graph below which sorts stocks by P/E ratio and then their subsequent returns. It doesn’t look sensible to buy high P/E stocks and yet that is what growth stocks are now – on high P/Es. Value investing is possible because capitalism allows companies to enter and leave businesses. New capital will flock to industries in which there are above average returns on capital and will leave those with below average returns. Growth stock industries attract new capital which drives down returns or causes enormous cash investment to remain ahead of the curve. In such cases there is little room for dividends which are a large part of the total return equation. Value stocks tend to be the opposite. Investors like to be with the crowd and so tend to ‘flock’ to growth stocks as they run up. It can all end in tears. The challenge is to remain immune from the fear of being unpopular and even looking stupid as the growth party rocks on. More subtly some investors argue that it doesn’t matter whether growth or value wins. It is often beneficial to use both approaches with an active manager in each, since the return series are diversifying. As long as both styles avoid stock disasters, the combination of styles can be powerful. More on that in later articles.  The extent to which growth and momentum investing has gained an irrational upper hand can be seen in the following extract from a recent Bloomberg note. “Investors may have borrowed money to chase the rally in the Sexy Six (Amazon, Apple, Facebook, Google, Microsoft and Netflix), resulting in a record amount of margin debt in March, Ned Davis, a strategist at the name-sake research firm, writes in a note. * Six stocks up 9.2% on a cap-weighted basis from March 1 to May 19, versus -1.8% for the rest of the S&P 500 * “The concentration in this bull market has been extraordinary, and that could be a sign of speculation and the type of narrow leadership seen in the late phases of bull market.” - Bloomberg Value investing tends to come “at a price”. That is there are certain consequences of using such an approach and while the dividend yield is higher and the asset backing security greater, there are consequent sector exposures and periods of doubt or underperformance. We list the major characteristics of value styles below.

Valero - The world’s largest refining company benefitting from lower feedstock prices and the shale boom in the USA. Glaxo Smith Kline - A UK based leading global drug company under new direction as it seeks to emphasise its consumer products division, and to get a better payback on its high R&D budget. Cisco - A USA based company shifting from a dependency on hardware sales to a service and software business model.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim