|

The Small Cap team take a look at one of the core principles of value investing. They examine the way in which business fundamentals and interest rates impact on intrinsic value. Summary Intrinsic value is a core value investing concept which is simple and yet often misunderstood. In the TAMIM Australian Small Cap strategy we always compare a stock’s intrinsic value with its current market value when making investment decisions. Our objective is to invest when intrinsic value is far in excess of the current market value; i.e. when there is a significant margin of safety. In this article we discuss the two drivers of intrinsic value… Introduction The term “intrinsic value” gets used a lot in the investment industry. It seems to be one of those terms which investment professionals pull out to show that they know what they are doing. However, in our experience, it is often misquoted and misunderstood. So what is intrinsic value? On a basic level, intrinsic value is the value of a company, stock, currency or product based upon fundamental analysis and without reference to its market value. And what is intrinsic value not? It is not a static value - it constantly changes and evolves over time. As Warren Buffet wrote to shareholders in his 1994 Berkshire Hathaway letter,

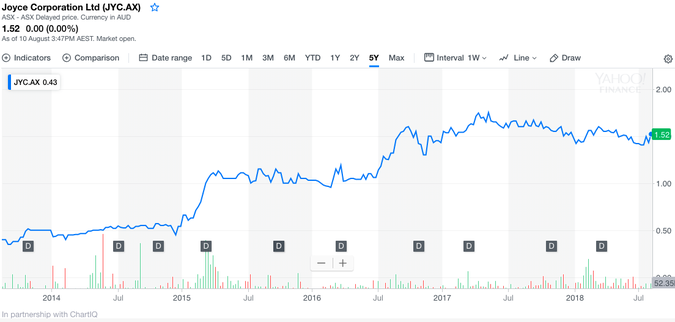

So in a simple formula: Intrinsic value = the present value (discounted by the risk-free rate of return plus an equity risk premium) of all risk-adjusted expected future cash-flows. The Two Drivers of Intrinsic Value... 1. BUSINESS FUNDAMENTALS All businesses are evolving, ever-changing entities. When valuing a business investors are simply aiming to capture a snapshot of future cashflows at that point in time, factoring in all known opportunities and risks. However, this snapshot of future cashflows is likely to change over time. Diligent value investors must be prepared to test and adjust their cashflows assumptions over time. The inherent challenge here is in reliably estimating future cashflows. Judging by the number of companies that fail to meet their profit guidance numbers, it is challenging enough for company insiders to accurately forecast their current year earnings. For outsiders’ or analysts to accurately forecast a company’s cashflows 5 or 10 years into the future, the challenge is magnified. We look to overcome this issue by investing in companies with a solid track record of generating cashflows, and use the historical cash flow data to help support our estimates of future cash flows. We look for companies where there is there is good visibility around the fundamentals of the company, and thus the cash flows the investment will deliver over time. For example, one of our newer portfolio positions holdings is Legend Corporation (ASX: LGD), a provider of consumables, tools and equipment for electrical projects. At less than 8x FY19 profits, we felt there was a significant margin of safety to build a position. When we value Legend’s future cashflows we derive an intrinsic value well above the current market value, and far above our original intrinsic value expectation. All being well we expect our intrinsic value for the stock to continue trending upwards over time. This is the beauty of high quality businesses; over time they create value for shareholders. And thus taking a long term investment view on high quality stocks makes a lot of sense to us.  Source: 2. INTEREST RATES Interest rate changes are the second driver which impact upon future cashflow assumptions because the risk free rate of return is a key input in the discount rate used to derive a present value of future cashflows. As a result, future cashflows are worth more in a low interest rate environment than in a high interest rate environment. With the 10 year US Treasury yield near to 3.0% and Government interest rates all around the world still close to historic lows, global asset valuations have been pushed upwards in recent years. The competition for yield has intensified as it has become scarcer. “Everything is expensive because this thing at the heart of the system has gone to all-time lows,” - Antti Ilmanen. When adjusting future cashflow assumptions to take into account changing interest rates, in our opinion it is important to bear in mind how current and future interest rates will impact upon future economic growth rates. This is particularly relevant now because interest rates were much higher in past decades than they are at present. This means that global economic growth was able to withstand higher interest rates in the past which arguably reflected higher underlying global economic growth. We believe it would be a mistake to simply extrapolate the growth most companies have reported over the past 5 years looking forward since interest rates are telling us that future economic growth will be far lower than past economic growth. And yet, this is exactly what the vast majority of analysts are currently assuming. The temptation to simply extrapolate is too strong for most. In our opinion, this makes most analysts’ current DCF assumptions far too high. A well thought out intrinsic value analysis will take the underlying economic growth rate into consideration. For example, Joyce Corporation Limited (ASX: JYC) is a high conviction holding in the underlying fund. We expect Joyce to report organic revenue growth for FY18 of at least 15%, driven by the continued roll out of KWB Kitchen and Bedshed stores, and a significant increase in turnover in the Lloyds Online Auction business. With significant investments made across all business units over the last two years, establishing a number of market leading positions, we expect Joyce to provide a very positive outlook for FY19 when it reports. In our opinion, significant value remains unlocked within its subsidiary investments, in particular Lloyds, so it was pleasing to see the recent strengthening of the JYC executive team with the appointment of a chief operating officer to provide additional management support and assistance with potential merger and acquisition activity. We calculated Joyce Corp’s intrinsic value according to our analysis of the risks and opportunities faced by the business. The intrinsic value was calculated as the sum of:

The sum of these components generated an intrinsic value in excess of $2.50 which was more than 60% above our average entry price. We expect this intrinsic value to continue to increase over time.  Source: We wrote more extensively on JYC earlier this year (see here). Conclusion

Intrinsic value in all businesses is a constantly moving target and requires in-depth analysis of the underlying business. In small and micro-cap companies we often come across a number of factors that depress the market price of a company on the stock exchange including low liquidity, no broker research, and a lack of profile in the investment community. However, none of these factors change the intrinsic value of a business. This presents us with unique investments opportunities where there can be very large differences between the observable ASX market price and our calculated intrinsic value – and thus a large margin of safety. We view this as core to our investment process and will only invest in a stock when the margin of safety is significant.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim