|

Given Putin's recent weaponisation of the energy supply to the EU, our fourth D, de-globalisation, couldn't be more relevant in today's global context. Find out more below...

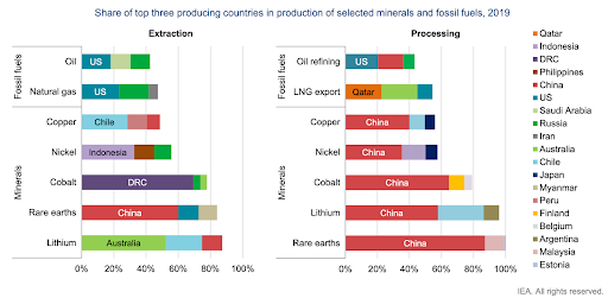

In our view, this story presents quite a poignant illustration of the interdependance of global supply chains, particularly a form of globalisation that showcases an asymmetry in relationships. More on that later. But for now, consider Germany, the fourth largest economy in the world and the arguable powerhouse of the Eurozone. The fact is that her second largest (and to date fastest growing) trading partner is China, while her largest energy source is Russia. Two jurisdictions that could not be more different on any other front other than commercial interdependence. Similarly, consider the country we live in and the fact that her largest export partner accounting for 43% of exports is China, while 25% of her investments come from the US. Two jurisdictions that seem to be headed on a collision course. We, however, believe that the very forces that resulted in the above scenarios are in the process of being reversed. Not because of any particular desire on the part of participants or economic imperatives but rather due to realpolitik. There is increasing awareness across developed and developing jurisdictions of the need to build more resilient supply chains and diversify economies. ContextTaking a historical perspective, the readership may be surprised (or not) to learn that if we use the term globalisation to describe phenomena of increasing connectivity and interdependence through trade and technology, then this is not a new phenomenon. One need only look to Pliny the Elder in the Roman Senate (1st Century AD), describing how Rome was being drained out of silver due to the penchant of Roman women for Indian silk. Or indeed, even Alexander's quest to unify the known world goes back even further. Globalisation is and has been, throughout human history, the norm with infrequent bouts of push back. So are we suggesting we see a paradigm shift and reverse course altogether? The answer is a no but with a little more nuance. We begin with a proposition: not all globalisation takes the same form. Today's view of globalisation relies largely on Smith and Ricardo’s absolute and comparative advantage. That is, the notion of economies specialising in particular production for overall gains through trade. From an economic perspective, this makes complete sense. It is what allows Russia to focus on wheat and energy production, given its abundance in land and natural resource endowments, while China has historically focused on manufacturing, given its abundance in labour. Specialisation, the argument goes, results in ever lower prices (via economies of scale and scope) and increased output. This logic has created perhaps one of the most significant expansions in living standards and output growth in human history. While simultaneously requiring commerce, growing access to new markets and decreased barriers to trade. It has also meant that supply chains have become evermore globalised, with particular jurisdictions focusing on specific aspects. Take Apple as an example. Consider Apple's iPhone and its manufacture involving 785 Suppliers in 35 countries, all specialising in specific components. This is not the issue, but what happens when the majority of suppliers, say around 350, are domiciled in China. Or going back to the example of Germany, 55% of their natural gas supply comes from Russia? Moreover, in the event of increased tensions in the political space, what then is the outcome should particular polities decide to use their specialisation or what is effectively an asymmetric relationship as a form of warfare? This is not something new, as the US's use of unilateral financial sanctions or China's threat of using rare earths supply to resolve disputes with Japan in the South China Sea in the now forgotten 2000's clearly showcased. Similarly, what may happen should exogenous factors such as a global pandemic, freeze supply chains. Even worse, when disparate responses by different polities in reaction to it cause the deflationary pressures of the globalised supply chains to be reversed? This is arguably the time we are going through. Current SituationWe recently came across an interview at the World Economic Forum with Dr Okonjo-Iweala, who happens to be the Director-General of the WTO (World Trade Organisation). She highlighted that despite the rhetoric, US-China Bilateral Trade Volumes reached the highest on record in 2021 and continued to grow apace during the previous Trump administration, irrespective of tariffs. This factoid speaks volumes about the sheer scale of the task ahead should consecutive administrations wish to reverse course. To give some numbers, since the end of WWII, global exports under the auspices of the General Agreement on Tariffs and Trade (GATT), the precursor to the WTO as mentioned above, have expanded over 340 times, while Asian exports have expanded 1100 times. The implication is that the region benefited disproportionately due to the post world war order. While this may have been somewhat a result of the dismantling of the colonial era policies that led to the captive Indian market for the British Empire and the reconstruction of Japan and China, what is immediately evident is the region's increased centrality to the global economy. What's changed? A reversal has been in the making since the second half of the Obama administration. After having been admitted to the WTO, it was increasingly clear that China was following a markedly different path from that of her regional counterparts. The historical tendency was that admittance into the global multilateral framework also translated into economic and political liberalisation. This was the case with the likes of Taiwan, South Korea and much of Asia (including Indonesia and Philippines, though to a lesser extent) but not China. On paper, it was the path of extraordinary powers of the past century, including Great Britain, which created an effectively closed economy within the scope of her empire (free trade for those within and collective barriers to those outside). Or that of the United States, which during the early 20th century had some of the biggest barriers to entry, including the introduction of the Smoot-Hawley Tariff Act that exacerbated the great depression. It was, in effect, developing its own domestic market while using trade policy to drive clear political outcomes. The now infamous Transpacific Partnership or the TPP effectively countered Chinese influence in the region but it was withdrawn by the newly elected Trump administration. The Trump era was characterised by further escalation in the tensions with China and the implementation of tariffs. The Chinese response was in part the now infamous OBOR or Belt and Road Initiative combined with the use of fiscal and financial initiatives to create its own sphere of influence. Within this already existing trend, two more events came to the front. The first was the Covid pandemic, and the second was the Ukraine invasion. COVID-19 & Ukraine - The Gamechanger?We would posit that despite the commonly accepted story line, the Covid pandemic and the Ukraine conflict only brought preexisting thematics to a front. What were previously signs of strain between two great powers (one incumbent and the other rising) has led to a conflagration across regions. Covid showcased the sheer fragility of supply chains. The Ukraine invasion highlighted the overreliance on specialisation as trade was weaponised and financial sanctions were implemented. It is, in our view, that the tendency of specialisation in trade leads to asymmetries in relationships. For example, 80% of rare earths supply comes from China, while Taiwan remains central to the global semiconductor supply chain, effectively spilling over into matters of national security. We would argue that we are potentially in the next equivalent to the scramble for Africa that characterised the checkered colonial histories of the past. That is the de-globalisation, relocalisation, and regionalisation of supply chains. This redevelopment of spheres of influence could reverse the efficiencies achieved through global trade in the past century. Again this is not new. We have seen periods of nativism creep up throughout history just pre-Great Depression and even before that, the mid-19th century during the heyday of the British Empire and the still developing former American colonies. This form of mercantilism is arguably a fundamental tenet of the legislation passed via the CHIPS & Science Act stateside and the infrastructure spending characterised in the Inflation Reduction Act (IRA). Looking elsewhere, we will likely see a rethink of barriers and the MFN (Most Favored Nation) framework that characterises the Multilateral Agreements today toward a more bilateral approach. These regions, or perhaps more aptly Blocs, in our view, will be similar to those of the past within a multi-polar (multiple powers) framework whereby the powers will act as the nodes that direct and are responsible for the allocation and direction of capital. For the investor, this has two implications. The first is the gradual de-risking of your investments in one sense since the competitive landscape for incumbents shrinks with the flipside of shrinking profit margins and earnings (i.e. higher input costs and smaller markets). The second is the increase in political risks as government policy will increasingly determine individual securities' fate and competitive landscape. On a more macro level, we are also likely to see the duplication of supply chains combined with subsidies and less efficient procurement practices with associated higher prices, which does not necessarily bode well for future inflation trends. Where are the Opportunities?Deglobalisation may create opportunities for the discerning investors amongst us. We need to consider this taking into account two factors. The centrality to the overall economy of deglobalisation and secondly the implications for broader national security within the context of a disunited world. Infrastructure We have previously alluded to the inefficiencies of US ports as an example, but we are already in the process of seeing some substantial deficits in projected and needed infrastructure (see graph below) spending globally. Especially within the transportation and power generation sectors.  Source: G20 Infrastructure Hub Energy We look to energy which has played no small part in the recent pains related to inflation. The below graph shows the primary energy production on a 5-year basis. Though our efficiency has more than offset this decline, the closing up of supply chains (and associated duplication) could intrinsically see this trend reversed (it may well become a necessity).  Source: Macrostrategy Renewables Closely related to infrastructure and energy is the speeding up of investments into renewables and the associated mobility transition. This will be increasingly central to the next leg of growth as nations such as China and India continue to invest heavily in the space. The below graph shows India's manufacturing capacity and demand for solar generation. According to the IEA, a price tag of $160 Billion per year is needed on average to meet energy production targets. On the other hand, despite being the largest producer of Wind and Solar, China looks set to continue at a rapid pace targeting 25% of domestic energy consumption from renewables. This aspect for the readership is not simply about the environment but the opportunities for growth and manufacturing capacity that could result.  Source: BRIDGE TO INDIA research Technology Here we are not referring to the market darlings that the readership may be more familiar with in the form of Facebook or Netflix but rather what we define as true technology, including the likes of Advantest (semiconductor maintenance) or even IBM. Here is where the old notion of comparative advantage might still be in play with the US and developed economies such as Japan being clear leaders. Along with outside performers such as Israel or Taiwan. We will see increasingly stricter enforcement of patents and targeted subsidies for R&D (which should hopefully see the below trend reversed in terms of investment expenditure).  Source: DSG Asia  Source: Visual Capitalist ConclusionThus, to conclude, we believe that a reversal of a particular form of globalisation that has become synonymous with the rapid rise of specialisation and a somewhat fragile supply chain is about to end. Increasingly national security and geopolitical imperatives will be prioritised over efficiency gains which we expect could result in:

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim