|

This week we address the third D in our 5 Ds. That is the change in demographics globally and the implications for economies and markets going forward...

Why Demographics?Now we're sure the readership has been saturated with doom and gloom scenarios ranging from Malthusians claims of ever-growing population being unsustainable to the aging demographic question (which implies quite the opposite and a declining population). So as always, let's take a step back and work towards a schema for understanding this particular thematic. In doing so, we will break down the question of demography and its composition into three distinct but interrelated categories:

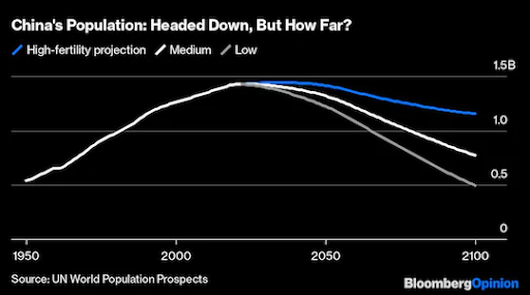

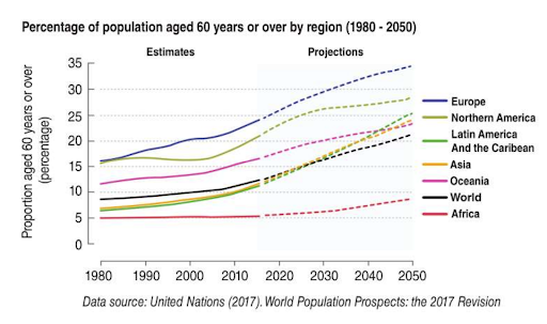

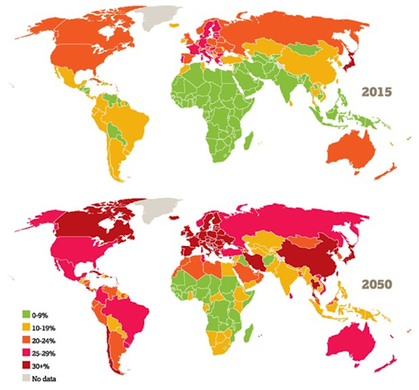

Fertility RatesWe begin addressing this particular issue by summarizing a speech by Pope Francis at the Vatican. At the beginning of this year, His Holiness got a lot of attention in the media for his lamenting that many couples are seemingly choosing to have pets over children and that forgoing child-rearing "takes some of our humanity away". Our question here, of course, is not the size of the Popes' flock but the validity of declining fertility across the planet. Is the Pope onto something here? Let's begin with some interesting facts. Fifty years ago, the median age of the world's population was 22, today it's 31, and by 2050 it will be 36. In fact, for the first time in history, the proportion of people over 60 now supersedes those below 5. According to the world bank, the fertility rate had dropped to 2.4 children per woman in 2019 compared with 4.7 in 1950 (i.e. a decline of nearly 50%). This becomes even worse when looking at cross country analysis with developed countries such as Japan now seeing steady population declines. There are currently 3 Million fewer people in that particular nation than in 2008. So this brings us to the next question, simply why? And why now? Current economic thought suggests an inverse relationship between levels of income and economic development to that of fertility. More simply put, the wealthier a society gets, the less babies. The basis for this could be in many ways intuitive. For example, in countries with lower levels of development, children may be a form of support helping supplement the family income or a form of social insurance. Similarly, higher levels of infant mortality may also perversely incentivise higher fertility levels. As development occurs and female participation rates increase, so does the opportunity cost associated with child-rearing. This may also be why nations such as China have started declining, and fertility rates have remained persistently stagnant despite the party's repeal of the one-child policy. On the latter's part, this will not be part of any official figures but rather independent modeling.  Source: Washington Post So empirically speaking to date, we have seen the facts bear out a lower fertility rate and an increasingly aging population. But why now? Answering this question would be a normative endeavor and can only be dealt with by opinion. We would suggest that there may be two factors at play. The first is the naturalistic assumption of finite upper bounds to growth in a Malthusian sense, and the second is that we are reverting to the long-term mean. Doesn't make sense? We'll take the below figure showcasing the fertility rates in the USA:  Source: Statista This graph showcases the long-term decline of fertility, with 1940-50 being the outlier due to post-war tendencies and a return of the GI Joes. A reversion to the long-run trend would necessarily imply an aging demographic. We would suggest this would be similar for much of the developed world. So does this mean we will see a future population decline? Current Trends & Potential ChangesAs with all forecasts, this may be a rather woeful exercise similar to gazing at the stars, but let's state the scientific consensus that we should reach peak population at some point in 2080, after which a period of stagnation should occur till 2100, followed by quicker declines. The UN's population division using assumptions of growth (based on historical averages) and extrapolating that out to the future assumes that the number at its peak would be 10.5 Billion people. This would be good news if one were to use Leeuwenhoek's contention of 13.5 Billion being the earth's peak capacity (for those unfamiliar with this gentleman, he was the inventor of the microscope). His guesstimate is as good as any since the formulae for expert predictions don't seem to have changed much. As a base case scenario, we can assume one thing, that the population over the coming decades should grow though at a decelerating rate (fertility). Much of this growth will come from developing nations that have yet to move up the income curve. On a more macro level and assuming the absence of great wars or catastrophic events, the population will also continue to age at increasing levels.  Source: United Nations  Source: UNDESA Population Division There are significant implications of this trend going forward, not all of which we can say will be spread uniformly. Current Trends & Potential ChangesThe first implication from an investor's perspective is related to the policy environment. Think for a moment that no major developed market cities or suburbs were ever built with the elderly in mind. Nor taxation or social security systems are designed to cope with a shrinking labor force to support an ever-growing and larger aged population. One solution to this could be the encouragement of migration to increase the younger population, but this could hardly be sustainable. Especially given the political ramifications, not to mention the fact that it may be a band-aid solution as the new immigrants are more likely than not going to revert to the long-term mean (i.e. fertility rate in the long run). We may, alternatively, see government interventions to reverse long-term trends, such as South Korea allowing parents to take an additional year of reduced work hours to top off an already generous one year of leave. The policy environment will thus be an evolving phenomenon as governments look to intervene increasingly and try to counteract societal pressures. We have already seen some extreme examples of this, with Hungary's Orban-led government announcing an exemption from tax for life to mothers with four or more children. Implications for the investor Baby Boomers as of today, control three-quarters of the world's net worth (assets) and reside primarily in developed nations. At the same time, Gen Z (born between 97 and 15) will inevitably make up the income side of the equation and the labour force in emerging markets (9 out of 10). This is a rather big call to make then it may sound at face value. Why? The investment landscape to date has been defined by a dynamic where goods for example are manufactured in low cost countries with the express intent of then exporting them back to developed markets (more often than not those countries or jurisdictions from where the capital originated). What we are positing here is that rather than this dynamic continuing to be the case, the market for said goods will be in the manufacturing countries themselves with simply the capital sources remaining the same. A sign of what is to come can be summed up by a gentleman by the name of Raghuram Rajan, an ex governor of the Reserve Bank of India who pushed for a “make for India” policy as opposed to the then touted “make in India” put forth by the then newly elected government. This aspect also ties in nicely with yet another topic we will address next week, de-globalization. Looking closer to home and towards more developed (more aged) economies, we will see significant tailwinds for capital intensity as the available labour force shrinks comparatively. A recent story we came across about Japan experimenting with robot nannies is a sign of what is to come. A shortage of carers leading to increased demand on the aging side of the equation. We posit that economies and industries will be transformed through the process along with the associated opportunities within a given index. For example, critical beneficiaries in Japan and China will be within the broader robotics sector and defence stocks. Names such as Amada, SMC and Fanuc are companies that look particularly attractive. Similarly, as the aging process speeds up, pressures will undoubtedly be placed on healthcare and aged care providers, which despite substantial growing pains, should see significant earnings growth. At the same time, policy interventions that push for increasing fertility rates, such as childcare subsidies and parental leave, will impact the investment proposition on two fronts. The first is the more obvious, childcare sector growth, but also the negative human capital risk (i.e. it could exacerbate existing labour shortages and create a new dimension for assessing human capital).  Source: AvatarMind Robot Technology Aging demographics and changes could nevertheless present opportunities for outsized returns.

On a side note: The jury is still out on the long-term implications for equities valuations in an increasingly aging population. For example, investors looking to derisk their portfolios as they move up the age bracket. On the other hand, those same investors may yet place demand for alternative financial assets such as fixed income which could lower the overall cost of capital and thus feed through into the equity markets.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim