|

This is the first article of a five-part series around Robert Swift's, 5 D's framework. These are; debasement (inflation), debt, demographics, deglobalisation, and decarbonisation. In today's article, we will discuss the economic climate that we live in, particularly focusing on inflation and how current monetary and fiscal policy affects this.

IntroductionWe begin the new series with a story. Credit where it's due, this is one we came across in a presentation given by Simon Michaux, associate professor at the Geological Survey of Finland. He tells the story of Scottish salmon and, more specifically, of the canned variety. It goes along these lines, imagine you were a Scottish consumer looking to buy the product at your local supermarket. Then ask yourself a simple question, is it more rational for the product on the shelf caught a few miles away to be packaged locally? Or to take said salmon and export it to China, to be manufactured in steel containers, packaged and shipped back to your local market? A reasonable person would say the former, but a financier would say otherwise. In actuality, the nature of global supply chains, and initially comparative advantage in labour, and now capital intensity, has meant that it is more economical to do the latter. That is to add 20,000 shipping miles to the product that may have, in fact, been caught a few miles away locally, just to land back at your local supermarket. So why are we telling you this story? It is an excellent illustration of hyper-globalisation, which is where there is virtually no barrier to the free flows of goods, services and capital. This has led to the deindustrialisation of developed economies while acting as a catalyst for the significant expansion of corporate profits and, for the investor, EPS growth. Aside from easy monetary policy, one could argue that hyper-globalisation has been the single most crucial thematic that has governed investor returns. But all of this, we feel, is about to change. The following 40 years will be somewhat very different from the last. So without much more introduction, we move on to discussing the new framework. That is, the trends that we think will impact the markets over the coming decades (known unknowns). We categorise these as being the 5 D's, again credit where it's due, and this is the framework formulated by Robert Swift. The 5 D’s are as follows:

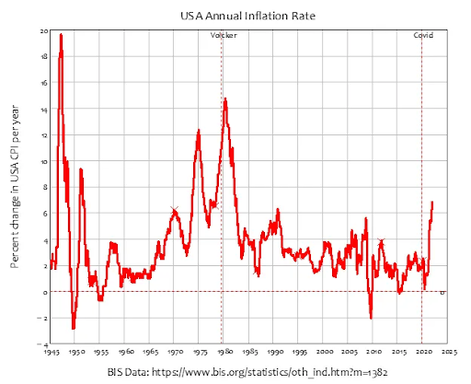

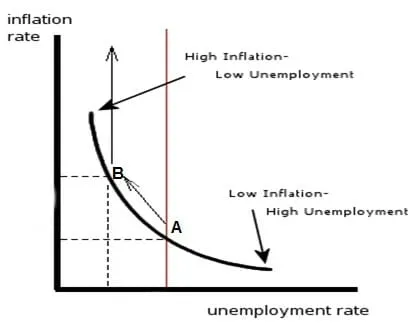

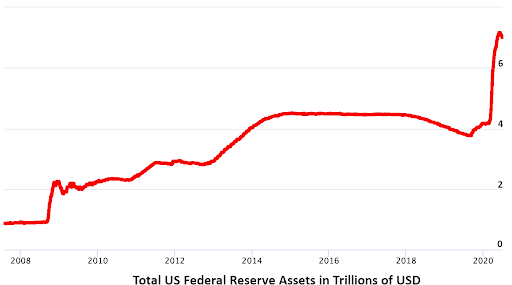

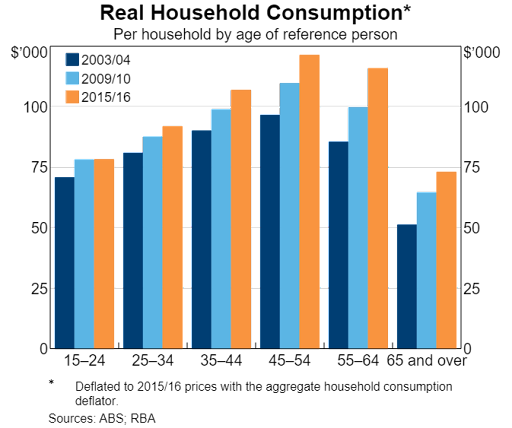

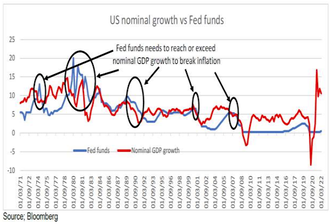

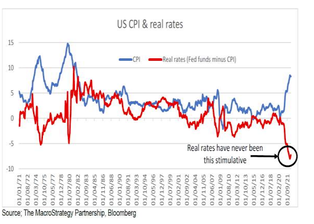

Let us begin with Debasement (Inflation). D #1: Debasement (Inflation)We're sure that the readership is somewhat aware of inflation, not to mention the so-called pundits patting themselves on the back for their doomsday calls on the monetary debasement that supposedly caused it. Close on their heels, we have the financial press making the call that this is a repeat of the '70s type of stagflationary environment. We are not fans of Milton Friedmans' notion of inflation "being always and everywhere a monetary phenomenon" nor that this is a repeat of the '70s. We believe the cause may be somewhere between the two. To gain an insight into what is happening now, let us understand what occurred in the '70s (especially given the tools being used are much the same). Today’s Economy vs the ‘70s Hindsight is an interesting phenomenon, especially given our unparalleled capacity to try and rationalise events in a rather linear, cause-and-effect type framework. This framework posits that the '70s inflation was caused by a series of policy missteps, seemingly with groundings from the post-war decade of the '60s. In addition to excessive spending of the Lyndon B. Johnson (LBJ) era vis-a-vis Vietnam and the oil shocks of the early '70s, combined with Nixon's effective dismantling of the Bretton Woods system. Seems familiar? Well, if one substitutes Vietnam for Covid, the post-war recovery with post-great recession recovery, and finally, Nixon's dollar convertibility move with QE by the Fed, one may easily see the parallels. But here is where we ask the readership to take a step back for a critical review of the facts. For one thing, we begin with figure 1, which showcases CPI as it is currently calculated (more on this particular fallacy later). We are someway from the twin peaks of 1975 and 1980.  Figure 1 - source: BIS data What is also markedly different in today's economy is the tightness in the labour market across not only the US but closer to home, while at the same time, wage growth is particularly lackluster. This particular attribute is quite important given that it implies the current inflationary pressures are NOT demand but rather supply-driven. This does not seem to be understood by the entertainment (news) industry or policymakers alike, given the policy tools in use. A helpful analogy is a notion of taking a sledgehammer to the task of cracking a nut. Inflation Fighting Toolkit: We begin with the Keynesian school of thought, which asserts that a tradeoff exists between unemployment and inflation - in other words, if inflation went up, unemployment would come down and vice versa (illustrated by the Phillips curve shown in figure 2). This is the fundamental rationalisation for the expansionary and contractionary fiscal and monetary policies undertaken to smooth out business cycles. In the '60s, it was what laid the foundations for the great societal measures undertaken by LBJ and the Nixon-era policies of the early '70s. However, what changed during that particular decade was the rise of inflation and unemployment at the same time that seemingly delegitimised the Phillips curve. The cure? Milton Friedman's monetarism, which saw inflation purely as a function of money supply, and thus, using this school of thought, the key to tackling the issue at hand may be to keep the rate of interest fixed and the money supply stable. Government policy should thus focus on the supply side and, if possible, seek to lower the tax burden (corporate or otherwise). Friedman also argued that the Federal Reserve should be abolished in preference for a computer program.  Figure 2 - Phillips Curve How Government use these theories in today’s systems: At this juncture, you may get the idea about the various policies and how they fit within the inflation-fighting framework. The solidly Keynesian nature of current central bank policy seeks to expand the money supply during recessionary periods while doing the opposite in times of economic upturn. The central bank does so while policymakers on the fiscal side of the equation often bizarrely go in the opposite direction (at least till the advent of Covid). This combination created a perfect cacophony of contradictory policies. What both sides seem to have forgotten, in our view, was the reality and mechanisms through which these various instruments work: Take Quantitative Easing, which has been a constant in the post-GFC monetary regime. What was seemingly baffling for most pundits was that despite the significant liquidity injections that this had warranted (refer to figure 3 for the FED's balance sheet), it had hardly moved the needle both in CPI and employment, at least till recently. Why? Well, for one thing, not all money supply is made equal; policymakers seemingly forgot the simple logic that increases in bank reserves do not necessarily translate into credit growth or real money supply. It may arguably get trapped with the commercial banking system. Where this changed, however, was the Covid era QE. Whereas previous rounds had only involved buying treasuries, the Fed decided to cross the Rubicon in many ways by buying corporate debt outright (legally grey).  Figure 3 - Federalreserve.gov Combine this with the significant expansion in fiscal stimulus (Keynesian style) that dispensed with the previously held views of budgetary conservatism, and you have the makings of actual inflation. We refer to the Trump-era tax cuts in the middle of the most significant economic expansion in decades based on Friedmans' ideas while dispensing such notions in response to Covid. A worst of both worlds type scenario. So this would suggest that the recent bout is a result of monetary expansion, right? The short answer is not really. The missing piece in the equation is wage growth, in other words, sustained increases (at least in nominal terms) of wages, which would then lead to sequentially higher demand and onwards in a circular manner. However, we are seeing low unemployment due to a combination of factors, including; declining or stagnant participation rates, demographics, and less bargaining power for labour - COMBINED WITH low wage growth. What was characteristic of the '70s was the disproportionate role of unions and labour movements in ascertaining wage increases along with a younger demographic (i.e. Boomers). We shall explore demographics in the coming weeks, but for now, think of the period of your lives where the highest expenditures are made or just refer to the graphs below. The clue is that it decreases sharply after the age of 64.  Figure 4 - source: ABS; RBA So what's the point we are trying to make? Firstly, the government is using policy tools that are fit for use but in a different era. Inflation is not demand-driven and is not necessarily about expanding the money supply. Yes, some of the inflationary pressures we are currently seeing may be a result of loose monetary policy and the fact that the rates have been below nominal growth for close (see figure 5) to two decades, except for pre-GFC (and we all know how that ended), and real-yields have been deeply negative for close to a decade (see figure 6). However, this would not explain why CPI has not been an issue until the past two years.

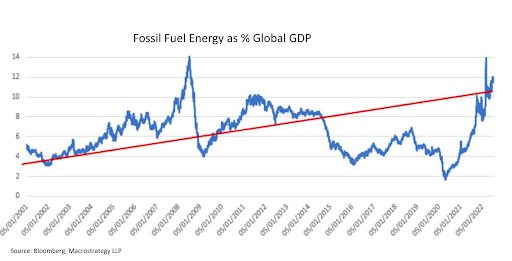

The Real Answer… We begin with the below chart (figure 7), and as the old saying goes, a picture (in this instance, a graph) paints a thousand words.  Figure 7 - Source: Bloomberg, MacroStrategy LLP The chart represents Fossil Fuel Energy as a percentage of GDP. Despite the headway made in transitioning economies away from fossil fuels over the past decade and a half, we may just have given back the gains in less than a year. On the other hand, it is a tale of policy missteps, shifts, indecisiveness and a plethora of not necessarily nice adjectives. We've spoken previously about our thoughts on energy and our contention that we will likely see peak oil as the transition occurs. But a quick refresher on the overall thesis. Energy Markets - A story of mishaps The transition towards renewables and green energy is a fundamentally different one. It represents the first time in human history that society is mandating itself to shift from a higher efficiency energy source to one with lower efficiency. One that should've required an incredible amount of cohesiveness and nuance in formulating policy. For one thing, ensuring a price mechanism enables an effective capital allocation. Instead, we did have a mishmash of distinctive mandates guided by fundamentally flawed assumptions. Ranging from direct action in Australia to ill-thought-out green taxes. Take, for example, the IEA STEPS (Stated Policy Scenarios Model) model, which presented the below as a base case as recently as 2021:

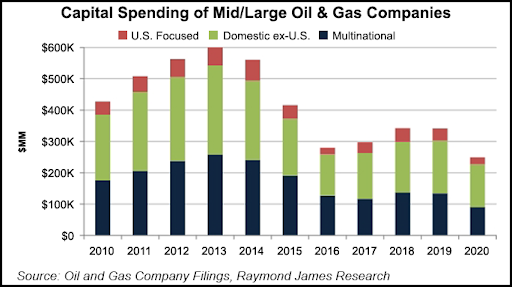

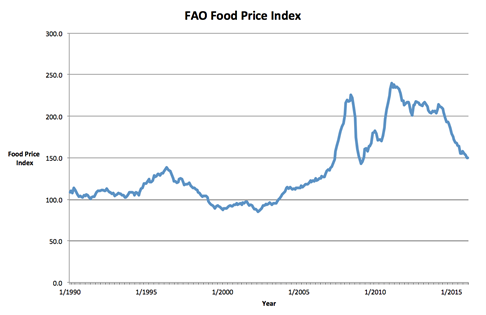

How far we have seemingly come from the above scenarios in the space of months. Using fallacies and forecast models as represented above, we have also opened up a scenario for decade-long under investment and opened up global supply chains to vulnerability. A vulnerability that saw the Eurozone’s continued reliance on one particular polity for the majority of her energy supply while at the same time experiencing gradual declines in CAPEX across traditional Oil & Gas sectors (refer to figure 8).  Figure 8 - Source: Company Filings We are by no means suggesting that renewables do not represent a perfectly viable alternative or, indeed, that traditional fossil fuels should be continued to be relied upon. We are positing that there should at least have been an awareness of the potential for steep declines in a new production for effectively multi-decade payoffs and the reluctance for exposure to stranded assets. One has to ask themselves, what sane financier looking at 0-emissions targets and uncertainty as to whether there may even be a market in a decade would finance new CAPEX? Similarly, the question also has to be asked whether the C-Suite of producers may wish to undertake any reinvestment or additional production even in the presence of markedly higher prices. While many have suggested and blamed recent woes squarely on Russia, we would like to disagree. In our view, much of the Russian supply of black gold remains online, being diverted to buyers in the form of India and China. We posit that the premia paid in spot markets due to Russia is circa. 20%. So is this scenario likely to stay, and what does this have to do with debasement (Inflation)? We recently found an article elaborating on the cost of bathroom tiles for the Australian consumer. Apparently, last month, the largest tile producer in Spain collapsed due to higher energy prices. If this is indicative of the broader market, and with Spain being the fifth largest product producer, one can imagine the cost implications for an already overstretched market (cost of production sky-rocketing 1,047 per cent over the past 12 months). But consider for a moment what goes into the CPI basket and uses for fossil fuels. Ranging from fertiliser to shipping to transportation. Consider, moreover, the implications broadly for the Food Price Index or FPI. Below is an illustration of the large drive-up from 2003 - 2007. Some of us may even remember the political implications ranging from the Arab Spring to instability across broader emerging markets.  Figure 9 - Source: Food and Agriculture Organisation of the United Nations In fact, on the last point, the readership may already be aware of the protests currently taking place in Europe with stakeholders ranging from the hard-left to the hard-right and everything in between. The cure? More stimulus measures aimed at ostensibly circumventing the pain of the hardest hit.

Looking to alternative solutions, we have the Federal Reserve going back to the same tools it has always sought along with the ECB, which is to raise target rates, which will supposedly dent demand (again, we have already posited that this is not a demand issue rather it is mainly a supply issue). If the logic is that inflation is eating away at the consumer's purchasing power, then surely it makes no sense to ensure that they are no longer employed and thus no longer able to consume at all? As stated previously, sledgehammer to a nut. We shall conclude with thoughts on what comes after the seemingly inevitable policy error. We would argue that the Federal Reserve's recent hiking cycle has created a scenario where liquidity has increasingly fled emerging markets in preference for dollar-denominated assets. With over 75 nations globally at risk of sovereign risk default at the last count, we see significant systemic risks. We feel that central banks may be the cause as opposed to the solution for inflation running away. Supply issues will not be sorted by taking liquidity out of the system or increasing the cost of capital for producers. We feel that there will be a slow but inevitable realisation of this but by which point it may be too late.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim