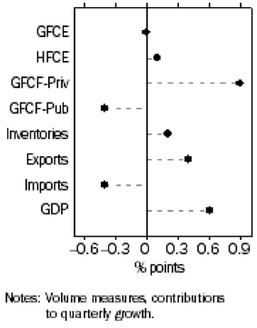

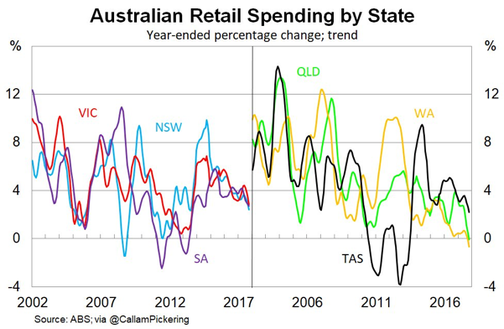

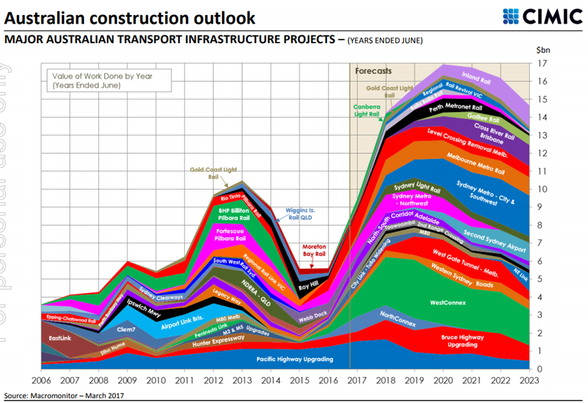

Looking inside the Australian GDP number and what the implications are for your share portfolio13/12/2017 This week Guy Carson takes a look at the Australian GDP figure and digs in to how it impacts the everyday share portfolio. Last week the Australian Bureau of Statistics (ABS) released the GDP data for the September quarter. The headline result saw an economy that grew at 0.6% for the quarter and 2.8% for the last 12 months, both slightly below expectations. The annual rate increased from 1.9% year on year rate achieved in June as the negative September 2016 quarter dropped out. Beneath the hood, there were some interesting trends within the data with strong fixed investment (infrastructure) offsetting weakness in household consumption. The chart below from the ABS splits out the different components of GDP for the latest quarter. As you can see the standout from the last quarter was GFCF – Private (Gross Fixed Capital Formation – Private) which represents private investment. This added 0.9% to the final number despite residential investment falling with infrastructure taking up the slack.  Source: ABS On the other side is the Australia consumer. Household Final Consumption Expenditure (HFCE) added just 0.1% which was the weakest result since 2008. This shouldn’t come as a major surprise and is something we have talked about for some time (see here). The trend of increased infrastructure investment, lower residential investment and subdued household spending are in our opinion likely to continue (again we wrote about this here). In order to see the economy transition away from the mining boom, the Reserve Bank of Australia cut interest rates to spur economic transition. With the worst of the mining decline now behind us, the RBA is reluctant for the interest rate cuts to continue (and at 1.5% there is a little scope for further cuts anyway). The interest rate cuts spurred a residential boom through both prices and (more importantly for the economy) construction. Further interest rates cuts are most likely off the table now and that means no further boosts for the household. It also means house price growth will slow (and potentially reverse). With no sugar hits left for households, consumption is set to be weak and has been slowing for some time. We can see this trend in the chart below looks at retail sales growth by state. The decline has been led by the mining states with Western Australian and Queensland in negative territory whilst the other states are trending downwards as well after a strong bounce in 2012 as the interest rate cuts started.  Retail sales were particularly weak with two key drivers. On July 1, households were hit with two price increases. Firstly, the large amount of household debt got hit with APRA induced interest rate increases. These rate rises were for interest only and investor mortgages. This did see a significant amount of switching from Interest only to Principal and Interest but the overall impact remains capacity taken out of the household budget. Secondly, electricity prices went up 17% across the board. The combined impact is that heavily indebted households have less to spend. Whilst the media has focused on the entrance of Amazon to Australia, it is our opinion that the weakness in household balance sheets has been the major source of weakness for retail companies to date. We do have to note thought that both of the price rises mentioned above are one off in nature. We do see households as the major risk to the Australian economy; however a stabilisation rather than a capitulation is the most likely scenario in the near term without further external cost increases. The major question for households therefore becomes how much impact does the wealth effect have? The wealth effect is the theory that when household wealth rises, people will feel richer and spend more. On the flipside, when prices soften, spending will suffer. With a majority of household wealth held in property and prices potentially starting to soften, there is the potential that household confidence will weaken and spending will follow. For us, the retail and residential sectors (as well as 2nd order derivatives) remain difficult to invest in. There may be specific opportunities but “Green Shoots” remain a distant thought. On the flip side, infrastructure investment continues to be the most likely driver of economic growth going forward. The chart below shows the range of projects and the spike in activity set to come. The projects are focused on road work and along the East Coast.  Source: Cimic Over the course of this year we have added positions across companies focused across the likes of Bridge building, surveying and scaffolding. These companies tend to be leading players in niche industries and as a result are typically ignored by larger institutions. We have been able to acquire these positions at what we believe to be attractive valuations and all cases believe the prospect for earnings growth over the coming years.

Timing the cycle is always difficult so whilst we do have an exposure to infrastructure, our major sector exposures continue to be Information Technology and Healthcare. These are two sectors that have structural tailwinds and contain quality niche companies that we believe will continue perform strongly regardless of the economic cycle.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim