|

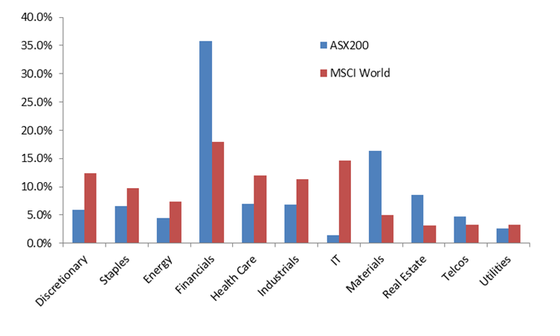

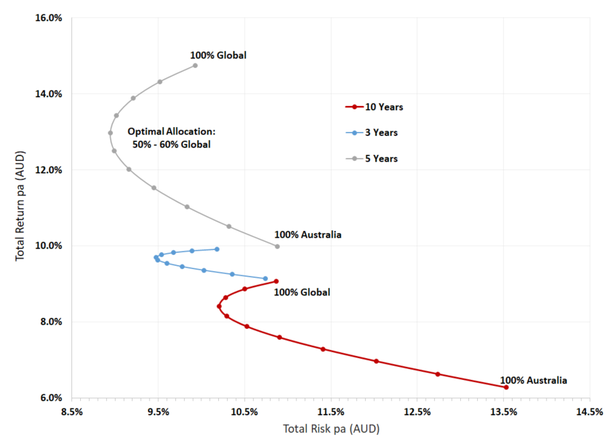

TAMIM Managing Director Darren Katz briefly takes a look at the month of July across both local and global markets. I have had the pleasure of spending a considerable period of time in the last month travelling around the country meeting with clients, potential clients and some large investment institutions. It struck me during these meetings that the Australian investment universe is rather constrained. While not a disaster, it is concerning. Of the ASX20 seven are Financials (down from nine a year ago) and four are Materials companies. The ASX20 only contains eight of the eleven Global Industry Classification Standard (GICS) sector categories. Information Technology, Consumer Discretionary and Utilities are not represented. Compared to global markets which offer quality technology and industrial businesses for investment, we miss out significantly if we focus only on Australia. Looking at the broader ASX200 we can see this imbalance clearly:  'Source: Thomson Reuters Just looking at an efficient market frontier chart we can see that over a number of differing periods it simply makes sense to ensure our retirement portfolios include a significant exposure to global equities. Interestingly if Bill Shorten is the next PM this becomes even more compelling as an investment thesis given Labour’s stated position on dividend franking.  At 31 July 2018 | Source: Thomson Reuters July was a month that pitted the concerns around trade wars against the strong earnings being displayed through company reports in the US. The MSCI World index was up 3.12% while the ASX 300 was up 1.3%. Our market lagged global peers with the US up 3.7% and Europe up 3.3%. Japan at +1.3% was more in line with Australia. Year to date Japan is down -2.4% compared to us at +5.7%. We continue to believe that Japanese equities present a very strong opportunity for investors. The month saw the ASX 200 achieve a level not seen in a decade. This was driven mainly by a strong recovery in Financials (mainly the banks) which accounted for half of index gains. Consumer Staples, Energy, Materials, I.T. and Utilities detracted from performance with six of eleven sectors recording positive gains. Even the telecom sector had a strong month up nearly 8%. As we head deeper into reporting season in Australia expectations are high and solid earnings will need to be evident to support the strong increase in valuations we have seen recently.

Australian inflation continues to be elusive, rising to 2.1% year on year in the second quarter. While this places it just inside the RBA’s target band of 2 to 3%, underlying inflationary trends are still sub-par which indicates little pressure on the RBA to increase rates. The Australian dollar was strong against the USD. With weaker inflation, and therefore a weaker interest rate outlook, one would expect a weaker AUD. Rising iron ore prices and demand for commodities has offset the widening interest rate differential between the US and Australia. Australian 10 Year yields were at 2.74% compared to the 3% experienced on the US 10 Year Treasury. Through the month, consumer and business data was stronger while the ever important retail housing market continued to soften. Retail sales were +0.4% month on month which was above expectations and employment was strong, rising by more than 51,000 jobs. In the United States we saw almost 90% of companies beating expectations through earnings season with full year earnings per share growth above 20%. Retail sales were up 6.6% year on year for June revealing a strong consumer. This represents the fastest pace of spending growth since 2012, likely driven by a strong jobs market. The unemployment rate did increase to 4% but this was likely driven by an increased participation rate with more workers heading back to the job market. June saw 213,000 non-farm jobs being created. US GDP came in at a strong level of 4.1% but this is a number that is probably distorted by tax reforms and the impact of transfer pricing bringing “growth” back on shore. With strong US economic data across growth, inflation and unemployment I would expect that the Powell Fed will continue to raise interest rates at around a quarter of a percent each quarter. As we continue to move through summer in the Eurozone, growth initially seemed to be dissipating but July activity suggests decent growth levels of approximately 2%. The composite Purchasing Managers Index (PMI) dropped to 54.3 but trade tensions did seem to ease over the month. The German PMI has shown signs of recovery despite the impact that an auto tariff could have on the economy. The Euro ended the month up 0.2% against the Greenback. On the other side of the world in Japan, stubbornly low inflation and signs of slower growth are making it tough for the BoJ. The negative rate policy was expected to be altered at the July meeting but this did not happen and there are concerns this will prove counterproductive to bank profitability. US-China trade relations did not fare as well in July. On 10 July, the U.S. Trade Representative listed USD 200 billion worth of Chinese goods that could be eligible for a 10% tariff. Several days later, China announced tariffs on U.S. agricultural products and the U.S. retaliated, stating that it may be prepared to further increase tariffs on the full range of goods imported from China (approximately USD 450 billion). While we ultimately believe that there will be no trade war the impact on business and consumer confidence may be real and negative. Heading into US mid-term elections the trade war rhetoric may have a big role to play in those being elected. The PBOC cut the reserve requirement ratio by 50bps in China at the start of July to try and encourage bank lending and cushion domestic growth from external factors. There was also a significant fiscal stimulus package announced, including tax reductions and expanding deductions on research and development spending for a wider range of companies. Elsewhere in the emerging world Turkey is causing issues, specifically at a currency level, which is having a spillover impact on other emerging market currencies. The longer I am in the investing game, the more evident it is that everyone has an opinion and that not everyone can be right all the time. Sometimes this is a function of timing and sometimes a function of simply being wrong. Investing is simple but not easy: get more things right than wrong.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim