|

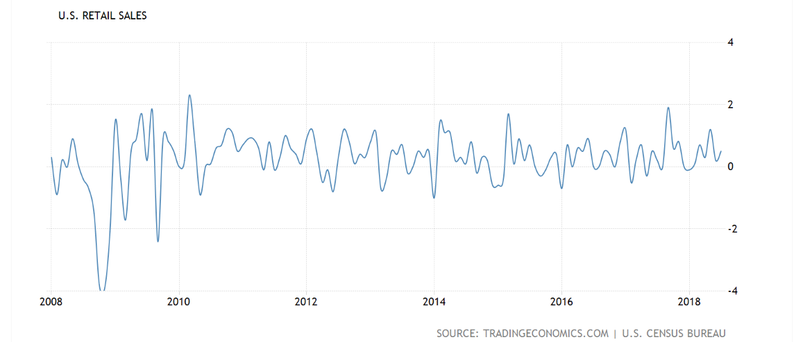

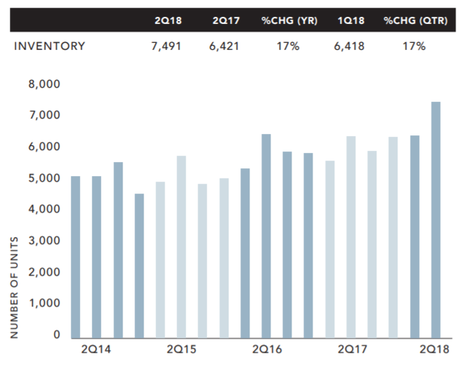

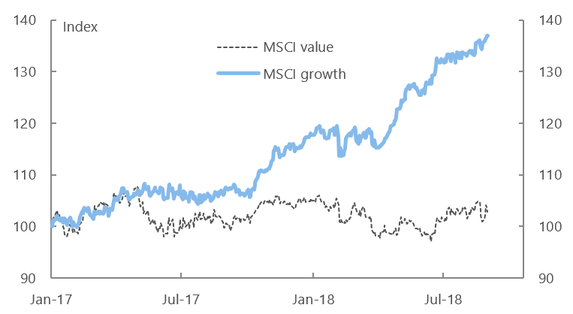

TAMIM Joint Managing Director Darren Katz takes a look at the financial world in month passed. I have just returned from a visit to the USA where I had the opportunity to spend a week in New York City and some of the surrounding towns. The last time I got to spend significant time here was literally 10 years ago during the week of the 15th of September 2008 that Lehman Brothers collapsed during the Global Financial Crisis. Wow - what a difference 10 years makes. That week in September 2008 the financial world was coming to an end, I remember going to sleep on the Tuesday evening of that week and being seriously concerned that American Insurance Group (AIG) would not exist the next day. I contemplated going down to the ATM and drawing out all the money I could because I thought there was a good chance the banks would not open the next day. AIG ultimately lost $99.2 billion in 2008 and received a bailout of $182.3 billion from the US Treasury and the Federal Reserve Bank of New York. Ultimately, the government made a profit of $22.3 billion when the money was repaid. My concern was that we were on the brink of social unrest and that if people were not able to access cash that there would wholesale rioting in the streets of New York and London. Ultimately this fear did partially unfold with riots occurring on the streets of London. Fast forward 10 years and, as I said, time makes all the difference. The streets of New York City are packed and yes it is the end of summer heading into the Labor Day weekend with the fabled retail sales but shops are full. This is a marked contrast to 2008 when the streets were busy but nobody was doing any spending. Every restaurant, coffee shop, Starbucks, Dunkin Donuts, every Broadway show and department store is packed and people are spending.  Source: Trading Economics The streets are thronging with people and, personally, one of more unbelievable observations was that there is massive construction activity everywhere. You are not able to walk one city block (and there are a lot of blocks) without seeing skips, scaffolding and building activity, from sixty to seventy story skyscrapers to smaller five to ten level apartments in the trendy Chelsea and Soho areas. Even crossing the bridge south to Brooklyn, the streets are full and activity is high. It does seem that the additional supply of units coming onto the market and soon to come onto the market is having an impact on property prices. The first quarter of 2018 saw real estate sales down 25% from the same quarter last year and the second quarter was down 14% from the previous year. Manhattan inventory increased year-over-year for the tenth consecutive quarter, up 17% annually to 7,491 listings, the highest of any quarter since 2011.  Source: https://inhabit.corcoran.com/new-york-city-quarterly-reports-2018/ The picture is not all rosy with what appeared to me to be large numbers of homeless people sleeping on the street, just about every block see’s someone begging for help and collecting cardboard boxes to use as mattresses for the evening. There is massive disparity of wealth apparent everywhere you look. On the weekend we traveled just fifty minutes north of the city to visit in White Plains, NY. Talk about a massive difference less than an hour down the expressway. This is the real America - while Westchester County, in which White Plains is located, is an affluent area, the walk around town on Saturday opened our eyes wide. When we walked into the Target and Shoprite centre, it was easy to see the difference to the “Big Apple” with lines to allow people to use their food stamps, people using the electrical outlets in the stores to charge their phones. There was plenty of poverty apparent and people seemed to be doing it tough. The biggest issue we see the US facing today is massive wealth inequality, according to The New York Times, the richest 1 percent in the United States now owns more wealth than the bottom 90 percent. This will ultimately be the defining issue of our times with social structures eventually refusing to accept this dispersion. So while New York pumps and is the jewel of Trump’s America, we pose the question will Donald be the man of the times and will he be the one to create better dispersion of wealth across the classes. My thoughts - as much as he says he is a man of the people, that is not true, he is looking after himself and until we can find another Roosevelt the disparity will continue to widen. “The test of our progress is not whether we add more to the abundance of those who have much; it is whether we provide enough for those who have too little.” Market Review: August 2018 was a volatile month with US China trade tensions continuing to boil, Italian bond market volatility, emerging market pressure from Turkey and yet another change of Prime Minister for Australia. US equity markets remained strong and US 10 year treasuries saw their yields fall to 2.86%. Growth continued its dominance over value, up 3.1% during the month versus value which was down -0.4%.  Source: Nikko Asset Management United States of America Despite global issues US equity markets were strong, with the S&P 500 rising 3.3%, as momentum was retained from July’s strong earnings results. Consumer discretionary and technology sectors were among the strongest performers. Apple became the first company to surpass a $1 trillion market cap on August 2nd. As discussed last month our concern around the US China trade rhetoric is that this could have an impact on both consumer and business sentiment but as yet we are not seeing this. Business investment spending looks robust according to the July durable goods report. The NFIB index, which tracks the sentiment of small- and medium-sized enterprises in the US, rose to a 35-year high. Almost a third of the companies surveyed are planning to increase capital expenditure. At a consumer level, retail sales rose 0.5% in July, above the consensus of 0.1%, buoyed by tax reform and a strong jobs markets. Anecdotally, as we walked the streets of New York City we did notice there were a significant number of shop windows throughout the city with job offers posted in their windows and while these were generally low paying jobs it was pleasing to see. Wage growth is not causing inflationary pressures at present and productivity measures are improving with second-quarter non-farm productivity growth at a seasonally adjusted annual rate of 2.9%. GDP growth continues to be strong with data released in late July showed that US economic growth accelerated to 4.2% annualised in the second quarter, its fastest pace in nearly four years. Europe It looks like there is a recovery taking place in Europe despite the weaker indicators from the start of this year. GDP growth for the second quarter was revised up to 2.2% while headline inflation for August increased 2% year on year despite core inflation remaining low. This indicates to us the European Central Bank (ECB) will keep rates on hold until at least mid way through 2019. Politically there are still tensions in Europe despite the trade tensions with the US easing. The new Italian government and the EU are not currently seeing eye to eye. The new Italian budget, due to be released at the end of September, is causing most of the angst with Italy’s credit rating at risk. The 10-year Italian government bond yield touched 3.20% by the end of the month which was 290 basis points above that of Germany. European equities sold off in August with the MSCI EMU index down -2.7%. Financials, notably banks with exposure to Turkey, were among the main detractors as the Turkish lira fell sharply and bond yields rose. Meanwhile, the Italian banks were also impacted by rising Italian bond yields amid worries that the new Italian government’s 2019 budget may come close to breaching EU fiscal rules as mentioned above. Automobile stocks also fell in August despite the easing trade tensions. German tyremaker Continental reduced full-year forecasts for sales and profit margins, citing slower sales as well as higher costs and warranty claims. Information Technology and Real Estate sectors delivered positive returns. The Euro fell 0.6% versus the US dollar. United Kingdom The FTSE 100 fell -3.3% for the month, making the UK one of the worst performing equity markets in August. Ongoing uncertainty around Brexit continues to dominate the UK headlines as the deadline for an agreement gets closer. Many are suggesting that negotiations are proceeding reasonably amicably. Even so it may take until November for Dominic Raab, the new Brexit Secretary, and Michel Barnier to conclude talks. Barnier stated that the EU was willing to offer the UK an unprecedentedly close relationship after Brexit. The decision by the Bank of England (BoE) to increase base rates failed to have a stabilising effect on the currency which fell 0.9% against the USD as the bank stressed that future tightening was likely to be gradual (there should be no movement until Brexit negotiations are complete at the least). The BoE judged the slowdown in the UK economy in the first quarter as temporary and weather related, GDP growth for the second quarter came in at 1.5% on an annualised basis, which was in line with expectations but a bit lower than the BoE’s forecasts. Asia The Topix was down 1% for the month after a recovery in the second half of August. The pulp & paper sector was the strongest performer as product prices remain at relatively high levels. Interestingly, the construction sector moved sharply lower. There was an unusually wide spread between defensive sectors such as foods and pharmaceuticals which have previously tended to move together. Underlying inflation in Japan remained low at 0.3%. Private consumption has been strong at 2.8% quarter on quarter, this alongside strong wage growth of 3.6% has helped stabilise GDP at 1% in the second quarter. There has been a temporary steepening of the Japanese yield curve through the month with the BoJ doubling the range of fluctuation around its 0% target to 20 basis points. August started with the US threatening to apply an additional 25% tariff on top of the existing 10% tariff on USD 200 billion of Chinese goods. Alongside this the Trump administration enacted legislation to better regulate inbound foreign investments. While this does not directly target China it still restricts the ability of the country to invest in the US. These tensions appear to be already affecting trade and output in China. Exports to the US fell 2.5% in July vs. June and fixed asset investments came in much weaker than expected, rising only 5.5% on the year for July. The Chinese authorities are aiming to counter this with measures to stimulate domestic demand. The banks’ reserve requirement ratio was cut by 50 bps at the end of June. There are also few signs, so far, of stress as Chinese FX reserves increased modestly in July to USD 3.19 trillion, which suggests that capital outflows were limited. Asia ex Japan equities posted a marginally negative return through the month with China and Hong Kong among the weakest countries. Singapore also under-performed, with consumer discretionary stocks among the weakest names. By contrast, the Philippines and Thailand posted positive returns and outperformed. In the Philippines the central bank hiked its key policy rate by 50 bps to 4% as inflation ticked up to 6.4%. Meanwhile Thailand, together with large index markets Taiwan and South Korea, outperformed peers given strong current account surpluses and foreign-exchange reserves. Australia Australian equities were up 1.4% through reporting season in August. At a sector level healthcare was the standout while financials, energy and materials detracted from returns. There were more beats than misses during the reporting period however there were also a significant amount of downgrades to forward looking earnings. As prices move higher separate to the downwards earnings revisions, valuations moved higher with forward PE’s reaching 15.9x. These levels are demanding and above long term averages of 14.4x. The big story of the month, besides the departure of Malcolm Turnbull as Prime Minister was the AUD depreciating 2.7% against the USD and 2.2% against the Euro. The Australian economy advanced 0.9%in the June quarter of 2018, above market consensus of a 0.7% expansion and after an upwardly revised 1.1%growth in the previous quarter. Growth was mainly supported by strength in domestic demand and foreign trade while fixed investment was flat. Through the year to the second quarter, the economy grew 3.4%, following a 3.2%expansion in the prior quarter and beating expectations of a 2.8%growth. This is the fastest annual expansion rate since Q3 2012.  Source: Trading Economics It is apparent that some of the price moves preceding and during reporting season are not supported by fundamentals. Historically, such periods of irrationality have not been sustained and stock prices have ultimately reverted to valuations supported by fundamentals.

All in all, the economic data for August points to a global economy that is still growing above trend, which should support corporate earnings globally. But geopolitical headlines continue to create considerable volatility around this generally positive trend. In this context it seems reasonable to remain long risk in balanced portfolios, while seeking at the same time low correlation assets to provide some protection as the cycle ages. We believe it makes sense to allocate to domestic value oriented equity investments while focusing on growth assets offshore, we also believe that value will revert to trend at some point.

1 Comment

Jason

13/9/2018 10:12:11 pm

Good insights. Thanks. Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim