|

While USA rate rises have gripped the eyes of the world, the situation in Australia presents a unique and challenging environment for policy makers. The RBA find itself juggling between multiple concerns. Inflation? Currency? Find out why below...

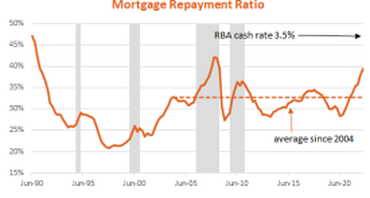

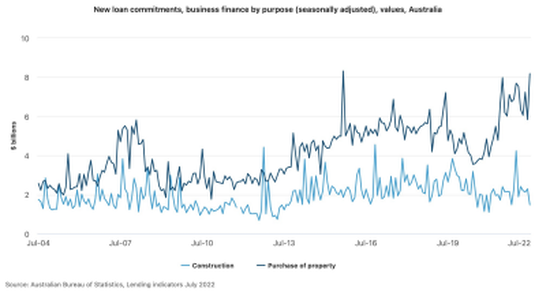

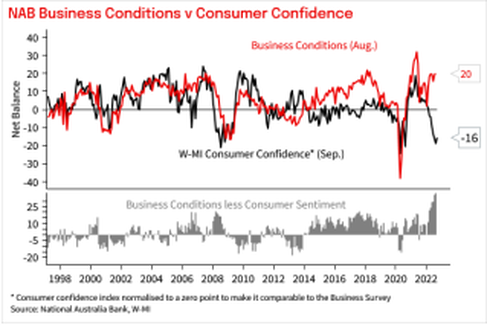

September Quarterly Macro UpdateThe Australian economy is in good shape, benefiting from high commodity and energy prices, a strong labour force and pent-up consumer demand. Some might say it's doing too well, given inflation is currently at 6.1 per cent and expected to reach a peak close to 8.0 per cent by year-end. The causes of inflation are largely outside of our control, with the Russia-Ukraine war, a subsequent energy crisis in Europe and China's COVID-19 zero policy exacerbating already existing pandemic-induced supply bottlenecks and labour constraints. Like many other central banks and economists, the Reserve Bank of Australia (RBA) was caught wrong-footed by inflation. Subsequently, the RBA has expedited the cash rate to close to a neutral setting — where it is neither stimulatory nor hampering the economy, of 2.35 per cent. The rapid pace of the hikes has caught the consumer off guard, particularly after the RBA shared publicly that it didn't expect rates to increase until 2024.  Source: Westpac The sentiment is now at crisis levels, with consumers unnerved by price hikes on everyday costs like groceries and utility bills. It should be said that what the consumer says is not what it is doing; retail trade numbers are up double-digit annually. How far will the RBA go?It’s an open question of how far the RBA will go to tame inflation. The pace of interest rate increases is the fastest since 1994 and it’s largely agreed that the full impacts won’t be felt for at least 12 months. Effectively the RBA is shooting with its eyes closed, hoping to break something but not too much.  Source: AMP Adding to the policy uncertainty is how borrowers who locked in ultra-low interest rates will respond to higher interest payments once they roll off. It’s estimated that 35 per cent of borrowers are locked into fixed loans, with most not expiring until 2023. By then, a standard variable rate will begin with six rather than a two.  Source: RBA The canary in the coal mine remains unemployment, which is currently just 3.5 per cent. There are more job openings than job seekers in the country. The risk remains that goods inflation is replaced with wage inflation unless pressure is taken off the jobs market. The RBA will be relieved that inflation expectations remain well anchored and within its 2-3 per cent target band. This is critical for two reasons. First, consumers and businesses are less likely to raise prices, mitigating against an inflation spiral. Second, the RBA can be more cautious in future interest rate moves.  Source: RBA Australia is Most Sensitive to Interest RisesOn a global outlook, Australia is considered one of, if not the most sensitive countries to changes in interest rates. Other borrowing markets — most notably the United States, use fixed loans with long tenures (10-30 years) rather than the variable rates mortgages commonly adopted in Australia.  Source: AMP Subsequently, the RBA will likely not need to raise rates relatively as much as its overseas counterparts. However, this could weigh on the Australian dollar (AUD) as savers can earn better interest rates abroad rather than domestically. Adding to issues is an exceptionally strong US dollar. The RBA risks importing inflation if it doesn’t keep up with the pace of hikes by the US Federal Reserve. Although aggressive policy moves in response are unlikely to help households either. Positively, the AUD is stronger against eight of its top ten import partner currencies this year. Monthly CPI on the HorizonAlso, unlike other countries, the RBA relies on quarterly rather than monthly inflation data for decision-making. The June quarterly consumer price index (CPI) — which counts April, May and June — wasn’t available until August 27 and couldn’t be used in policy meetings until September. Effectively, the RBA was setting policy with both backwards looking data and five months old. Positively the ABS will introduce a monthly CPI from October 26, which will account for between 62-73 per cent of the quarterly basket and be released in the following month. Bond Purchase Program AftermathDeputy governor Michele Bullock disclosed the well-intentioned but now ridiculed bond purchase program (BPP) led to a $44 billion paper loss for the RBA and could lose up to $58 billion depending on cash rate moves. In simple terms, the RBA bought three-year bonds in the market to keep the cost of debt pegged to the cash rate — at the time just 0.10 per cent — to support economic activity when the pandemic hit. However, it kept buying for too long, with the market eventually calling its bluff that it could maintain the cost of debt at almost zero. This forced it to abandon its defence of the 3-year and lose credibility with market participants. Overall, the bank now has more liabilities than assets, inferring negative equity. If the RBA were a normal business, it would not be a going concern. But because it can print its own money, it lives on. The art of central banking! Domestic Home LendingAfter exceptional gains since the pandemic’s onset, the Australian property market has begun to cool. Coinciding with the initial RBA rate increases in May, national property prices across have fallen 3.5 per cent, remaining 28.6 per cent above their trough in September 2020.  Source: CoreLogic House prices will continue to fall as the full impact of rates rises is felt by borrowers. Positively, the overwhelming majority of households are sitting on material equity buffers. The RBA estimates that a 20 per cent decline in house prices would result in just 2.5 per cent of borrowers in negative equity.  Source: AMP The more pressing issue is serviceability. Standard variable rates are rising to levels not seen for a decade and will likely head higher. BetaShares mortgage repayment ratio (MRR) — a measure of a borrower's ability to service a mortgage — reached 39.0 per cent in July, compared to an average of 32.7 per cent since 2004. Should interest rates climb to 3.50 per cent, which is below the current market pricing of 4.15 per cent, the MRR would soar to 42 per cent — the highest point since 1990. All else equal, this would result in a material decline in property prices as serviceability falls in addition to new borrower's capacity falling. This is already showing up in RBA data, with housing loan commitments falling.  Source: BetaShares Investor lending is falling relatively faster than owner-occupiers as they cash in on significant equity gains or decide the hassle of rising interest rates outweighs the potential negative gearing benefits. This is supported by data from CoreLogic, which has noted a higher-than-average volume of investment properties listed for sale.  Source: RBA Business Funding ConditionsBusiness credit growth remains elevated as corporates draw down on cash reserves and seek funding for new and existing operations. There remains a sizeable gap in the credit market, particularly in the small-medium enterprises (SME) market, working capital and other lending no longer serviced by the big banks.  Source: ABS (Construction & Purchase of Property) Notwithstanding the volatile operating environment including input cost and wage inflation, business is more optimistic about the outlook than the consumer. Due to input cost pressures and low labour availability, construction remains challenging. Building approvals fell 17 per cent in July, with developers starting new work down to a three-year low of 38 per cent. Business conditions are best in mining, and to a lesser extent in transport, recreation, retail, wholesale and financial services.  Source: NAB Non-performing loans remain historically low in terms of both default rates and actual loan losses, according to the prudential regulator. Recent updates by the major big banks support this, with the impact of interest rate increases yet to increase bad debt provisions — although it wouldn’t be unexpected if this did eventually occur. Like residential, commercial property will likely fall in value as interest rates impact capitalisation rates, which are used to determine the yield and subsequent purchase price of real estate.  Source: RBA This is further supported by the spread between the discount rate for Australian government bonds — considered to be the risk-free rate, and commercial property being at historic lows, especially in the industrial sector.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim