|

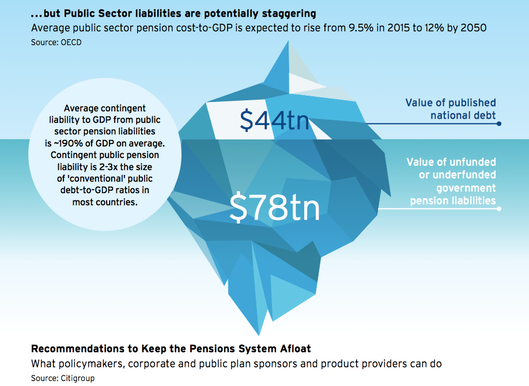

At TAMIM we believe a blowout of fiscal deficits and expenditure on a global scale is coming. This will present opportunities, winners and losers, and so it is important to understand why this will happen and how to be ready for it.  Source: Schwadron Source: Schwadron At TAMIM we are constantly striving to understand market contexts and alternate viewpoints. At the end of the day this is what makes markets. As the old saying goes, there has to be someone on the other side of every trade. After all if you’re selling equities or any asset at a given price there must be someone with a different view willing to pay that price. We made a very specific call last week when looking at the recent hiccups in repo markets. We suggested that we could see another round of Quantitative Easing in Q4 which could lead the S&P to head higher. More locally, we are also very likely to see a bout of QE. This week we shall make an ever bigger call and that is a blowout of fiscal deficits and expenditure on a global scale which in itself presents opportunities, winners and losers. Monetary and central bank policies globally have been pretty homogenous. Despite the doom and gloom pundits who predicted inflationary pressures due to these extreme policy measures, this has yet to take place. Let's face it, the ECB or the Federal Reserve buying assets on the open markets effectively creating money out of thin air should be inflationary, right? Believe it or not, those pundits are somewhat right, except that it didn’t show up through CPI or core inflation but through asset price inflation. A classic case of this is in the US Treasury markets where the issuance and pricing continues to not make sense. One reason could be that secondary markets fill in the void created (typically issuance goes via primary markets i.e. Federal Reserve to Dealer Banks & Foreign Governments and Foreign Central Banks to Secondary Market Investors). Take out foreign governments (because of geopolitical reasons) and you have everyday investors and pension funds piling in to those markets (the only reason prices could continue to bloat). We see this in the negative yielding debt that continues to blow out in the EU as well. Bond valuations go up when there is increasing uncertainty. We don’t have the time in this article to actually go into what that means for portfolio managers at pension and superannuation funds trying to obtain a nominal yield (hint: you have to move up the risk curve to maintain the same returns whether it be junk or sub investment grade). There is some logic to this madness. Investors are trying to diversify as best as they can. We’ve previously talked about the fallacy and madness of buying bonds at premium valuations to hedge out high growth equities. So the bond markets, as the TV pundits are saying, might be predicting imminent danger in the real economy while equities valuations show the opposite. The thing that the average spectator doesn’t understand is that they don’t actually see what has been happening. This is simple, asset prices and low interest blows out corporate leverage, maintaining 10% profit growth on a corporate level which then isn’t reinvested in the companies as traditional economics teaches us but rather trickles through to Asset holders in the form of dividends and share buybacks. It isn’t a problem and is perhaps rather hypocritical of us since we benefit, but it shows up in income inequality and relatively stagnant wage growth. Think about the economy being a pie, if corporate profits are growing as a relative share of GDP then the part that is missing out is labour. It is a fact of our daily politics that people don’t realise this because it is hidden from actual reality since people don’t necessarily see their consumables going up in conjunction. Instead what is more intuitive for them is to blame red-herrings or alternatives, weather it is unchecked Immigration in the US (just a small check to this reality, Mexican Immigrants neither take away American jobs nor do they as a community have greater propensity to commit crimes as the Tweeter in Chief likes to suggest). One of the real reasons for the divisions in American politics and the rise of populism across the EU, is that people genuinely feel that they have missed out and don’t see their wages rising at the same levels or at an appropriate pace as they were taught by their parents and/or grandparents. Thank God for compulsory voting in Australia where the silent majority are forced to at least whisper and the encumbered public forces some sense back into the politics (despite the parties being a relatively binary left or right). Yet even in this lucky country, I talk to clients everyday whose biggest concern is helping their grandchildren have the ability to afford a decent house.  So, where does this end up taking us? The pendulum will swing and it will swing soon. We see that monetary policy is blunted, even the non-conventional tools, though we didn’t have QE in Australia. But once the next round of QE happens in America, we think that their hands will be thrown up. Locally, where we are one cycle behind the rest of the world, a 0.25% cut in rates doesn’t make the same difference as one from 5 down to 3%. The big swing and vacuum will have to come from governments and locally we saw that in tax cuts and some infrastructure spending. Globally, we saw this with similar tax policies in the US, the sugar highs. In Europe the only thing stopping the same trajectory is Germany, who spent most of their 2000’s and 90’s on wageless productivity growth which came to buffer them somewhat at later dates but not anymore. We’ve seen almost negative yields similar in Australia, tax cuts might help the existing status quo but it doesn’t put money into people’s pockets. The US is increasingly moving in this direction. Whether you look at the Democrats who talk of the Green New Deal or College Debt Relief or even the Republican side where they won’t even start touching unfunded pension liabilities or Medicare (here we are thankful for our superannuation system). In Europe, similar problems. So what happens now? There might be a polarisation but the caveat will be that politicians can be counted on to spend, maybe not with the same gusto or coordination as central bankers but it will come. Especially when they realise that you have negative yielding debt and historically low rates of interest to be paid. Is this necessarily bad? We would argue no, definitely not. It will however mean more volatility in equity markets as they rationalise a lot more. On a longer term basis, we are actually bears when it comes to the bond markets. Most investors will be stuck holding duration risk and government spending through direct measures, such as infrastructure, backed by no increases in taxes mean only one thing. Inflation and an incentive to inflate away the real value of debt and existing liabilities. Fortunately for them, most people do not realise that inflation is another form of tax. So yes, bonds will, in the medium term, continue to be bullish as the uncertainty levels increase and equities will have the caveat of being rather more bearish (in the sense that we might not see the same strong returns we saw in the past ten years globally). If we didn’t want to be completely selfish about it, the irony is it will probably be a good thing in the long run. We can still sustain reasonable returns holding good companies that generate a decent cash flow and not mind them spending a little more on their employees and capital expenditure. In terms of how we pick and choose, this will be contingent on a heterogenous policy environment. With central bank policy we can at least be sure how different asset classes react since they use the same tools to treat every situation, whether real or not, the same way. That being said, political policy will be increasingly contingent on the intergenerational changes taking place. We recently saw a classic example of this with the climate strikes that have been taking place around the globe. Student debt forgiveness is not necessarily bad and gives much needed relief and motivation to the younger people who, as future tax-payers, are going to have to fund those unfunded liabilities of pensioners.. Infrastructure spending that creates jobs, while it might blow out deficits, can be funded at exceptionally low rates for significant long term actual benefits. Structural reforms to depreciation rules can get companies to spend more on long-term projects. Giving those incentives is much better than giving tax breaks straight off. Companies that are scared that the economy isn’t all that crash hot aren’t going to reinvest because they got a tax break, they pay it out as dividends or in the form of buybacks. We know this, we have been seeing it. For bonds, we continue to have political uncertainty in the medium term so they might still continue to rally a bit more, but it is a case of hot potato. Equities wise, value will certainly come back into vogue - we’ve been reluctant to make this call up until now - over the next six to twelve months. You will actually have to think about what you buy and what sectors you want exposure to rather than just buying the market and hoping things go up. What does this mean for us? For us, we are not touching bonds at any duration and the shorter term credit assets continue to pay us on an opportunistic basis. Our biggest play currently is to replicate bond risk profiles by buying decent real assets that can generate a solid but stable yield (i.e. doesn’t have to shoot the lights out but presents with a relatively safe risk profile) and can manage if inflation starts ticking up again as a result of fiscal largess. Believe it or not, you can buy good assets at a good price even in this property market (the key will be to look at things like tenancy duration and metrics of that nature). In terms of longer dated bonds , we will keep our answer simple, NO. If you’re buying a liquid asset whose coupon doesn’t change (unless you buy inflation indexed and good luck finding those at even half-decent yields) at sub 3 or 4% that, to us, is not a good investment. That being said, we do hope that there continues to be investors who are willing to back sovereigns at sub par and negative yields because we want to see governments getting aggressive when it comes making structural reforms and spending money that improves the real economy rather than just markets. We would just rather not pay for it by buying subpar yields ourselves when we know what the end result is (hypocrisy at its best but we’re not claiming to be a charity either). Why? We still somehow believe in the free market. Just pumping asset valuations will not be sustainable and people will begin to question the underlying assumptions and walk away. This is especially applicable to a disillusioned younger generation (and rightly so in some respects) who, whether we like it or not, will be the tax payers that fund our future needs and retirements and the pensions of the older generation.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim