|

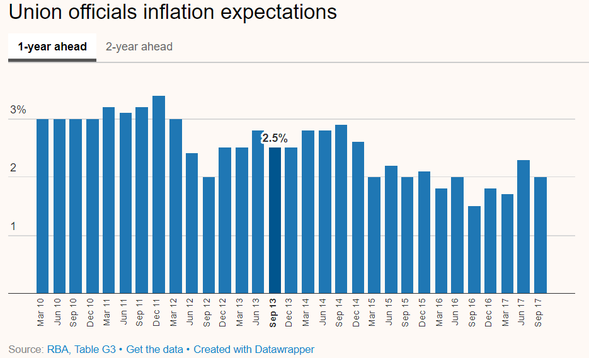

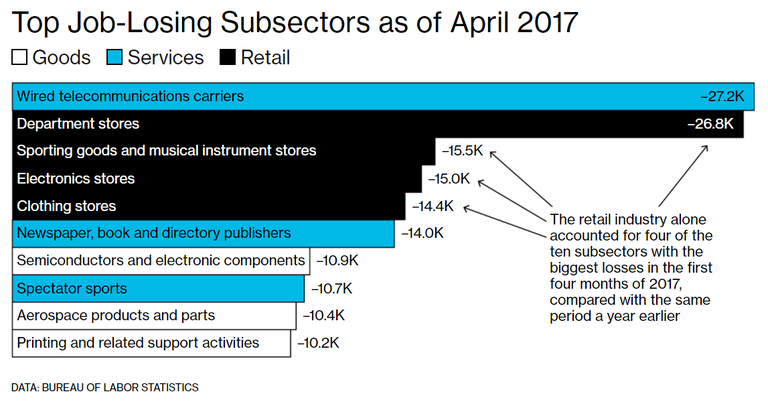

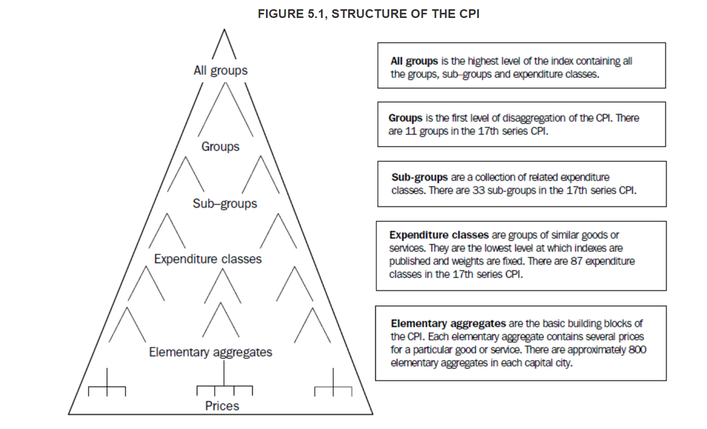

This week Darren Katz, TAMIM director, takes a look at what is happening in markets round the globe with a focus on the key driver of the moment - inflation. February saw a spike in market volatility to levels not seen since 2015 when the market had a meltdown over Chinese concerns. While Australian equities were relatively resilient at +0.4% (including dividends) the S&P ended the month down 3.7% but was down 10% at one stage caused by market panic over wage inflation. Wage inflation is seen to be a strong signal of stronger overall inflation. Anticipation of a stronger inflationary environment led market participants to believe that central banks would raise rates more than previously anticipated. The view at TAMIM is that, while we may see short term inflation occurring, primarily in the US, this is not a long term change to what we believe is a secular trend of deflation. Firstly, we believe that commonly accepted measures of inflation (see below) do not provide us with an accurate view of inflation and secondly we believe that innovation leads to disruptive forces which will be deflationary. Australia At February lows the ASX 200 was down 3.6% (not including dividends) but recovered to be down only 0.4% by month end. It was actually up 0.4% for the month when you include dividends. February was reporting season in Australia and we were happy to see that overall it was strong with over 38% of companies beating expectations. Healthcare was the biggest contributor to monthly index performance however this was offset by declines in real estate, energy and telecom sectors. Australian equities still trade at a relatively high forward price-to-earnings ratio of 15.7x at the end of February. Commentary from the RBA remains upbeat with growth and inflation targets remaining unchanged. The RBA does expects the unemployment rate to fall by an additional 0.25% to 5.25% before inflation returns to target. In Australia there is certainly no wage pressure forcing inflation higher, and the most recent wage price index increased by 2.1% year-over-year. Even union officials seem to believe inflation is not on the radar anytime soon as can be seen in the chart below.  Source: RBA The key factor to consider when looking at wage inflation over the long term is the disruptive forces of automation and artificial intelligence and their impact on wage growth. Over the coming decades job losses to technological advances will serve to reduce the amount spent by corporates on wages taking the pressure off wage inflation even further. The chart below from the US Bureau of Labor Statistics illustrates the impact of Amazon and their disruptive force on the retail industry.  So what is inflation and how do we commonly measure it in Australia? According to Investopedia, “Inflation is the rate at which the general level of prices for goods and services is rising and, consequently, the purchasing power of currency is falling. Central banks attempt to limit inflation, and avoid deflation, in order to keep the economy running smoothly.” In Australia we commonly use the Consumer Price Index (CPI) as a measure of what the inflation rate is and the Reserve Bank of Australia will use monetary policy to attempt to keep CPI within a specified target rage (2 to 3%). CPI measures quarterly changes in the price of a 'basket' of goods and services which account for a high proportion of expenditure by the CPI population group (i.e. metropolitan households). The CPI population group is made up of various groups which have different spending patterns from retirees to those on social welfare. This 'basket' covers a wide range of goods and services, arranged in the following eleven groups:

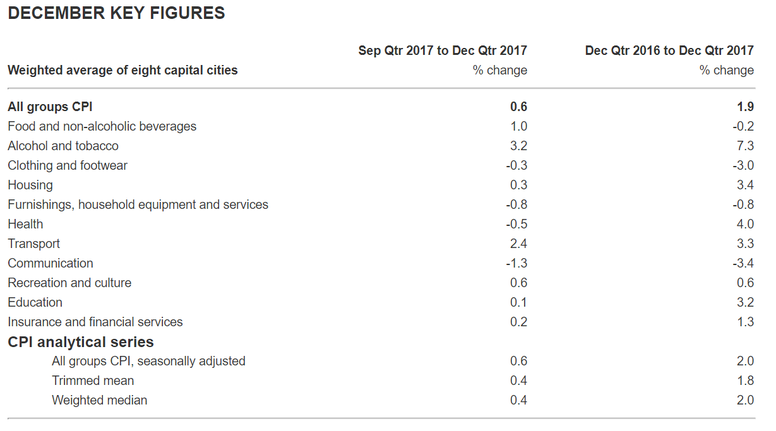

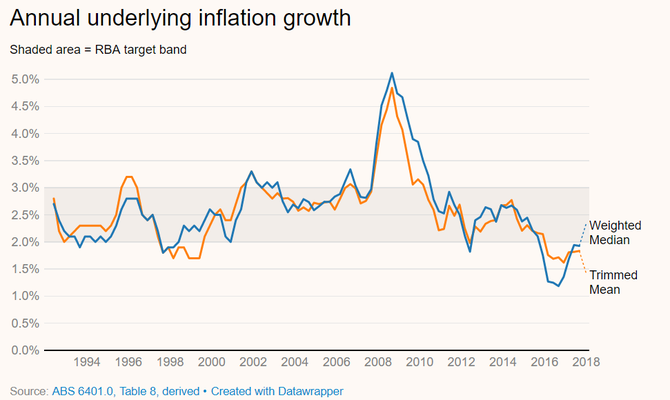

These groups are divided in turn into 33 sub-groups, and the sub-groups into 87 expenditure classes. Presentation of the CPI in the form of groups and sub-groups provides the user with quite a degree of versatility in interpreting the results. Index numbers for individual groups and sub-groups can be analysed separately as can their individual effects on the whole index  Source: ABS The problem with the calculation of price data across a basket of goods is this has to end up being an approximation and what might be a good approximation of the level of price inflation that you experience is very different to what that which someone else may experience.  Source: ABS According to the latest release of CPI figures in Australia, the annual increase to the end of December quarter is 1.9%, however, a five-year update of household spending patterns recently by the Australian Bureau of Statistics (ABS) implied the consumer price index (CPI) was overstating inflation by around 0.22 percentage points. That might not sound like much, but annual inflation is already low at 1.9 percent and, crucially, short of the Reserve Bank of Australia’s (RBA) target band of 2 percent to 3 percent.  Source: ABS Global Markets Despite a benign inflationary environment in Australia, a key concern amongst global investors is that as the economic recovery proceeds, resources will become fully utilised and inflation will reappear. The re-emergence of inflation would force central banks to reassess their easy monetary policy stance. In the January U.S. labour market report, the annual pace of wage growth rose to 2.9%. The spooked market priced in a faster pace of Federal Reserve tightening and the ten-year US government bond yield quickly rose towards 2.9%. The reality is that core inflation remains below central bank targets of 2% in many regions, including the U.S. and Europe. Brent crude oil prices fell 4.7% over the month holding headline inflation rates lower despite the stronger then expect US Jobs data. Janet Yellen stood aside at the Fed handing responsibility to Jerome Powell who will take some getting used to. Strong US job prospects and tax reform are supporting consumer confidence the result of which was steady US growth of 2.5% in Q4. In Europe, stronger economic data helped to prevent a sizeable equity market correction. Draghi, in his speech to the European Parliament, argued that the European Central Bank (ECB) must remain patient and persistent with regard to monetary policy to create conditions for inflation to return to target. So to conclude, while the markets remain uneasy and concerned around inflation this is not in our view a significant market risk. The risk that remains is the reaction of the market masses to a change in belief on interest rate policy.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim