|

A $480bn stimulus by Biden attempts to tackle the world's most pressing economic issues today that the intelligent investor can't ignore... Which companies win? Which lose? The 2nd and final part of our series reveals all...

We continue this week with the final of our two-part series by looking at the Inflation Reduction Act, hereafter referred to simply as the IRA (If haven't already read part 1; click here). While the Bill itself is a rather trimmed-down version of the more ambitious plans touted earlier in the year, it nevertheless represents a major impetus across three major categories; tax, climate and drug pricing. Before proceeding further, however, we shall begin with the obvious, the name. It baffles us how an increase in fiscal stimulus, representing around $480bn USD, could be considered counter-inflationary. One could argue that it does increase revenues (more on tax later) by $750bn USD over the next ten years, but still the effect of reducing inflation would be statistically negligible. Despite the rather creative titling (marketing) in the lead-up to the midterms, the Bill broadly targets two categories; the democratic base and seniors. On the former count, the IRA represents the largest climate change bill in US history, while on the latter count, it goes a long way in tackling increasing drug prices. With that quick summary, let us get a little more granular and, in doing so, by looking at the winners and losers (a rather helpful tool for the investor). Industry WinnersElectric Car Makers: $7,500 USD per vehicle tax credit for consumers wishing to purchase electric vehicles, which looks to be a direct handout to EV manufacturers, including GM (NYSE: GM), Tesla (NASDAQ: TSLA) and Toyota (TYO: 7203). But before you go out and buy the securities, there is a caveat; the Bill requires compliance with vastly stricter battery and critical minerals sourcing requirements. Here is a list of the requirements:

In particular, the IRA would prohibit the application of the above tax credits where a vehicle's battery contains "any" critical minerals sourced from countries such as China and Russia. Advanced Manufacturing & Minerals Supply: In addition to the above, the Bill also targets stakeholders across the supply chain with new authorisation for $40bn USD in loan guarantees which could be used to support critical minerals projects. This could benefit producers such as Albemarle Corporation (NYSE: ALB) and, for the more Aussie-oriented investors, companies such as Ioneer (ASX: INR). In addition, sticking to our point last week around increased government intervention, the Bill appropriated another $500m USD. This was done to enhance the use of the Defense Production Act (DPA), which President Biden recently invoked to support critical minerals production. Renewable Energy: Additional tax credits were also lined up for renewables, including production tax credits to accelerate the manufacturing of solar panels, wind turbines and batteries with an estimated price tag of $30bn USD. Another $27bn USD for clean energy technology to support the deployment of technologies to reduce emissions, especially in disadvantaged communities. Additionally, a methane emissions reduction program is tasked with reducing leaks from the production and distribution of natural gas. This is potentially a windfall from two angles;

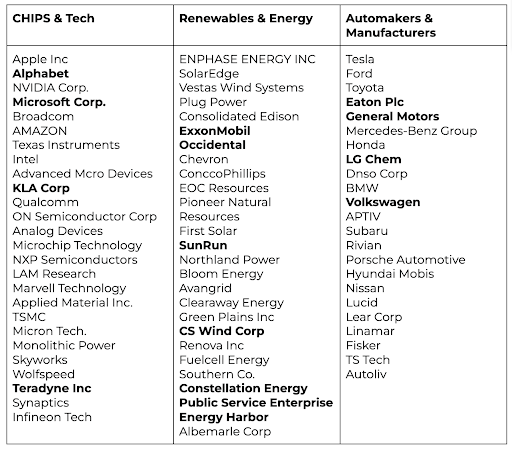

Securities that may benefit include; SolarEdge (NASDAQ: SEDG), Sunrun Inc (NASDAQ: RUN), and Plug Power Inc (NASDAQ: PLUG). Nuclear Power: Many in the readership may already be aware of our optimistic outlook for nuclear, and we remain of this view. An additional $30bn USD worth of tax credits also flows through to nuclear reactor operators, including Southern Co (NYSE: SO), Constellation Energy (NASDAQ: CEG), Public Service Enterprise (NYSE: PEG) and Energy Harbor (OTCMKTS: ENGH). What is also worth mentioning is that effectively 6% of the global supply is offline (this is what Russia and Ukraine cumulatively account for). Given the new impetus that the IRA represents for the broader sector, we think that it may bode well for upstream miners, including Energy Fuels (NYSE: UUUU), NexGen (NYSE: NXE) and, of course, our very own Aussie giant, BHP (ASX: BHP). Oil Producers: It may seem like strange bedfellows, but Oil and Gas also got a significant boost with the increased potential for more federal oil and gas sales and an existing tax credit boost for carbon capture. For the investor, however, this would potentially apply to majors instead of the junior sector. The policy tool is via tax credits and, as such, is heavily tilted towards benefiting existing incumbents (vs. subsidies or direct stimulus). Companies that could benefit are Exxon Mobil Corp (NYSE: XOM) and the Buffet favourite Occidental Petroleum Corporation (NYSE: OXY). Industry LosersFor the Australian Investor, the biggest outcomes are the implications for the pharmaceutical and technology sectors. That is if you have exposure to them stateside. Pharmaceutical Companies: In a potentially massive setback for K-street and the pharma lobby, the Bill allows Medicare, for the first time in history, to negotiate prices directly. While the initial Bill did have price caps, this aspect was scaled back after being being blocked initially. This means drug makers could potentially offset reduced Medicare revenue via increases for private insurance patients. The extent to which the latter is the case remains to be seen. For now, this may be a double whammy for Pfizer, already battling lawsuits from Moderna over Covid-19 vaccines. But overall, this could have significant implications for majors in terms of earnings growth, including Johnson & Johnson (NYSE: JNJ), Roche Holdings (OTCMKTS: RHHBY), Novartis AG (SWX: NOVN), Eli Lilly And Co (NYSE: LLY) and Sanofi SA (EPA: SAN). Tech Companies: The Bill also directly hit the bottom line for the previously high-flying tech darlings. They will potentially bear the brunt of two major tax increases in the proposal; 1) a 15% minimum tax on FINANCIAL STATEMENT PROFITS (the IRS will be using the income statement and GAAP earnings going forward), and 2) a new levy on stock buybacks (i.e. 1% excise tax). Stock Specific WinnersSo now that we have outlined the winners and losers, we move on to securities that look to be likely beneficiaries of the new impetus in Washington. In doing so, we shall begin with a broad list of publicly listed securities in three buckets:

Potential beneficiaries by sector With that broad list, we would like to take a further in-depth look into three companies that may be of interest (from each broad category). The first KLA Corp, second Occidental and finally Eaton Plc. KLA Corp (NASDAQ: KLAC)  KLA semiconductor defect inspector | Source: KLA.com Let's begin with a simple definition of what KLA does. It is a capital equipment company that supplies process control and yield measurement systems to the semiconductor industry. Think of it this way, a chip manufacturer, before installing their products, needs to test whether they work or not. This process is essentially what KLA focuses on (i.e. testing) along with yield measurement. So what are the potential benefits? Sticking to the theme of this particular series, the business will potentially in our view, be a net beneficiary of the stimulus packages by congress. In addition, there appears to be a longer-term trend of manufacturers outsourcing the semiconductor assembly and testing services, given the higher costs associated with large wafer fabrication outfits. Moreover, we feel that the business has greater earnings visibility than competitors in general (i.e. longer-term contracts). Looking at the numbers, the business maintains a dominant market share within its niche (i.e. 55%), with HoH revenue up 32% and outpacing its nearest competitors; Applied Materials, Inc. (NASDAQ: AMAT) (5.8%) and Lam Research Corporation (NASDAQ: LRCX) (6.6%). This company is one to keep a close watch on, with revenue growth guidance at 20% compared with 9% over the broader market. Occidental Petroleum Corporation (NYSE: OXY)  Source: Pixabay The first thing that plays in this business’s favour is the 50% stake that Berkshire has in it. But this is a turnaround story we couldn’t have foreseen just a few years ago. The business is up 140% for the year (outperforming the sector overall, which is up 32%). Despite this, we would like to state that the business's cash flows are growing and now stand at a yield of 12.5%. In our eyes, Occidental represents a classic case of market misallocation. The business was caught in the headwinds of ESG-minded investors who could not see through the shorter-term pain. This, combined with less than stellar spot prices and COVID-19, meant that the business’s ROIC was 1.5% in 2019, seemingly a perfect storm. It seems, however, that we have entered a new phase for the business. Debt has shrunk from $40bn USD in 2019 to $22bn USD today, and assets have continued to shrink from $107bn to $74bn USD. This is exactly the kind of story we want to see in the oil business. ROIC now stands at 14.4%, and the new policy environment makes it rather amenable for the ESG-minded investor (we are sure the business will shortly take advantage of carbon sequestration given the incentives, i.e. it has already allowed for circa. $1bn USD to this event). Eaton Corporation PLC (NYSE: ETN) Eaton is one business famous for perhaps the wrong reasons, given its tax avoidance shenanigans (Through an Irish acquisition, Eaton was able to shift its HQ to the less taxed Irish jurisdiction). Aside from mentioning such a history, it is one business that is sure to take advantage of any tax credits that may arise. For those less aware of what the business is, simply put, they are in the business of power management. Its products can broadly be categorised into four buckets

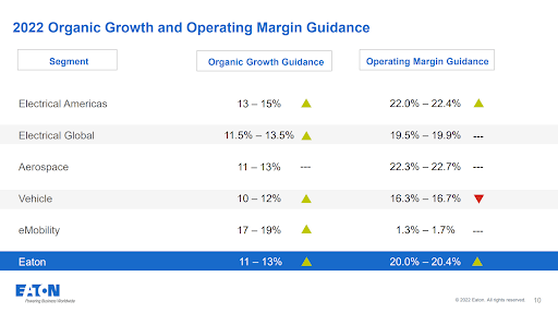

As the readership may have realised reading about the products and associated segments the business operates in, this is one firm that could benefit significantly from the stimulus measures. While we have yet to see a clear outline of the implications for CAPEX given new incentives, we would posit that the final eMobility, category which is already growing at a high double-digit pace, will be pushed even further. With that, let's look at the numbers, with the company delivering record operating margins and non-GAAP EPS earnings. The growth forecast is now 12% above 2021 levels, though the foreign exchange has significantly hit sales (i.e. stronger dollar). Operating margins now stand at 20%, while sales growth for 2Q stands at 15%, orders up 29% and a backlog up 89%.  Source: Eaton company filings In addition to strong numbers and backlog, the recent Russia/Ukraine War, and continued expansion of NATO defence budgets, could see a significant rise of orders. Disclaimer: KLAC.NASDAQ is currently held in TAMIM portfolios.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim