|

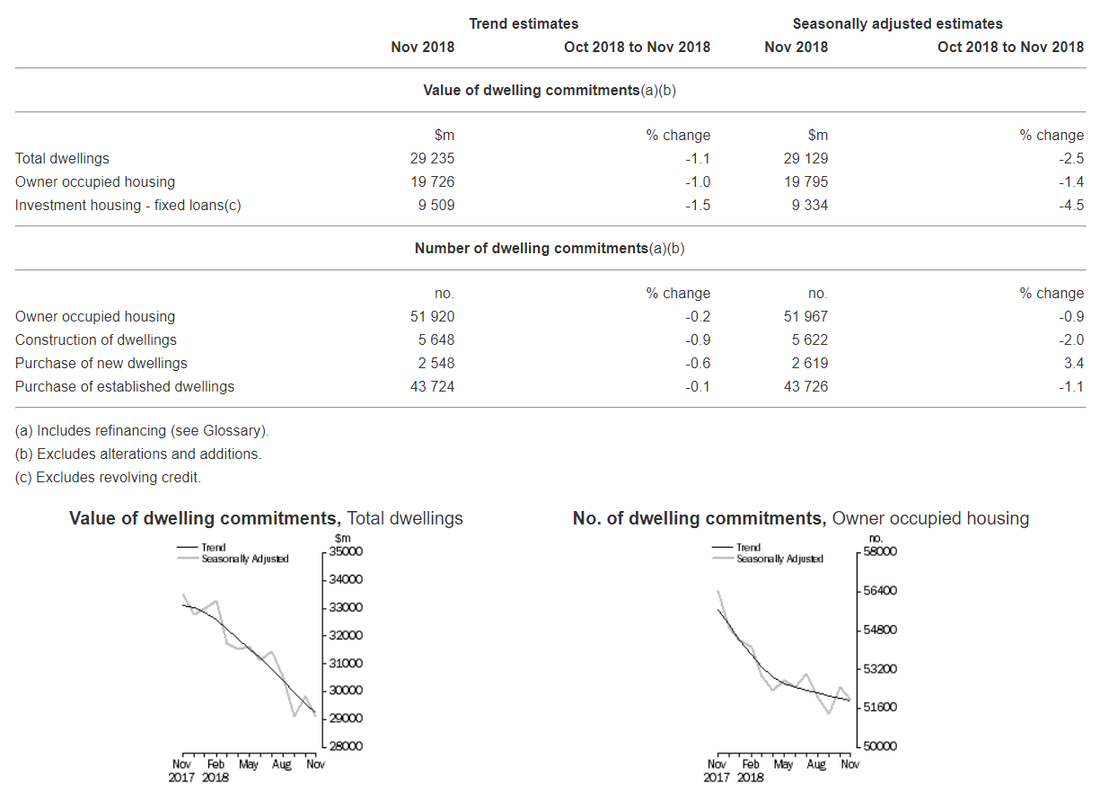

This week we would like to revisit the age-old topic of the banks. But not by traditional metrics in the sense of either assessing their stability or balance sheets, we would like to posit an alternative perspective, something that Australian investors don’t think about. This is their place in the Australian economy? Remember the economics textbooks that told us that the financial system allocates surplus capital for productive purposes? Let us begin by examining what has been going on. Australia, as we have mentioned in several other articles, is about one market cycle behind the rest of the world. Canada and South Korea somewhat are in a similar boat. We have seen how the overallocation of major financial institutions in one particular segment (i.e. residential lending) played out during the GFC. Not that we are making the mistake here of confusing that particular debacle with a credit rather than liquidity issue. On average, the Big 4 Australian banks have about 80-90% of their balance sheets allocated toward residential mortgages. On top of this, their other segments, like SME business lending, are typically backed against personal guarantees by business owners (property once again). Unfortunately, one issue for banks going forward is that they are unable to compete on anything other than a product that has been heavily commoditised (mortgages and net-interest margins). There is substantively no added value unfortunately on top of which there is no actual customer experience/loyalty left, especially post royal commission. This is despite NAB’s esteemed Chief Customer Officer (sorry Mr Baird but you did take a rather tough gig). Competitive pricing comes when the actual experience is sticky, think of loyalty points at supermarkets or travelers who stick to one airline or hotel chain. Unfortunately for banks, their quest for shorter-term profits has lost touch with the actual mainstream customer, they are no longer loyal customers. Remember a generation ago when it used to be different? When the bank manager actually had a face and advice and customers would stick with “their guy”. Now let's look at their actual business. Part of this consolidation and the simplification of their lending models has been an excessive reliance on residential mortgages. This makes sense given the fact that we did have a two-decade-long property bubble. Let us make clear that the purpose of this article is to not go bank bashing but to understand what it is that they are doing and to scrutinise Australia’s fixation with having only four well-run (supposedly) banks. A proposition that is somewhat ridiculous. The problem with an over-reliance on the property market and property buyers per se is that, yes, the longevity of the mortgages does make it sticky money but the problem for the actual economy is does it add that much value? Yes, the construction industry employs approximately 15% of the population but let us be direct, and for those of you who are curious feel free to look at a break down the statistics between mortgages for new-dwellings vs. market rebuys, how much value does the banking sector actually add? To put it simply, the vast majority of Australian listed companies list their debt overseas. In terms of SME lending, it seems to be the odd-ball segment whose lucrative nature in a time of falling interest rates gets them to push in and out. When interest rates are manageable they prefer to keep their proposition to residential lending and then push through to corporate and SME during times like this. Despite the furore around the investigation into their inability to pass on rate cuts, it is a simple ploy to avoid and drag out as they rejig their business and go-head-to-head again with business lending (call us cynical if you want). Unfortunately for them, two decades of getting rid of any human asset other than those with a residential focus has left them in a tight spot in terms of in house expertise. This might sound a tirade against Australian banks but this is a trend that is global in nature. Bank’s main line of business is no longer lines of credit, business lending, it is the game of commoditising everything that is on an economically scalable proposition. Unfortunately for the Australian economy, businesses provide employment. SME’s provide employment to the tune of 44% of the country. People buying properties might provide employment on a much shorter term basis but not on a consistent long term basis that keeps the economy dynamic. Property might be vital to the functioning of the Australian economy but on a normative basis it should not be. Financials should not be 30% of our index and decent technology propositions like Atlassian should not be finding their homes overseas. We are left with consumer credit propositions such as AfterPay or Latitude Financial, we are by no means disparaging them but it tells you a lot about this market when that remains the case. Our financial institutions (here and globally) have over complicated the issue (by going ‘back to basics), by leaving the sensible banking behind the door. Even regional banks who, despite their proximity to regional areas, are unable to create a decent enough value proposition for farmers in this country. Farmers who, by the way, employ 300,000 of this country’s labor force, employing 83% in rural areas which, despite what you might hear on the contrary, still remains relevant and vital for the Australian economy.  Source: Australian Bureau of Statistics Good Old Fashioned Banking & the Fallacy of Too Big to Fail Many of you might like to take a look at the recent Federal Reserve Regulations around tier one requirements. Basically, it is discriminating against the bigger banks by lowering the capital adequacy requirements of smaller regional banks. Although their goal wasn’t necessarily to increase competition, we believe this is a step in the right direction in terms of promoting back to basics and long term banking. Regional banks in the US are much better at actually looking into their customers and their credibility than many of the majors. Ironically, this is how the behemoth Bank of America grew out, because their major focus was on unbanked segments of the public like Italian Americans whose business many of the northeast banks turned their noses up at. On top of that, think back to how BOA actually survived the GFC, they never forgot their DNA. We would like to see more of this take place around the world. How did four big institutions, or the equivalent Big 5 in Canada, become such goliaths that they have the ability to hold a nation and its institutions hostage. These perceptions of stability are beyond us, capitalism is premised on free markets and proper good old fashioned trust-busting is about the opposite; everything that is too big should fail. This is how competition works, survival of the fittest might not be the viewpoint we take when it comes to schooling but it should be the case with free markets. The notion of having regulations which make it so exorbitantly expensive for new entrants to join an industry that, as we have touched upon, is commoditised is beyond us. Ironically the Hayne Royal Commission’s recommendations with regards to the mortgage industry would have further entrenched the position of the banks. Our view? Have less regulation and actually enforce existing regulations on banks (or firms much smaller) who are unable to pass regulatory muster. We work in an industry, unfortunately, where employees of regulatory bodies and financial institutions have a much cosier relationship than should otherwise be permissible. Imagine the furore with Julie Bishop when she floats the idea of joining the boards of a few firms that might have a conflict of interest a year after leaving politics. In the EU, the Basel reforms and the financial stability framework, while well intentioned (or so we hope), will essentially entrench the same institutions and make it exceptionally hard for new entrants or increased competition. Imagine being in an industry that is relatively easy to understand (despite the jargon the banks spout), dealing with an increasingly disloyal customer, AND has a commoditised product and yet still having an oligopoly structure. An unfortunate and gross distortion of free markets. Interest Rate Cuts

Forgive the unnecessary sarcasm but I am sure homeowners will feel exceptionally better off with the RBA rate cut by 25 bps. But we would like to ask if any of you are actually business people and tell us how you feel about your rates at this time? Especially when it comes to working capital or things of that nature. The fact of the matter is this, we run a credit portfolio where we lend to relatively small businesses (by the bank’s standards) at rates often at 9 - 10%. The fact that businesses with some credibility and cash flow should pay that much in terms of interest is beyond ridiculous. Yes, granted, we are happily jumping in to fill the void. You might say we are opportunists, not hypocrites. We do after all run a business as well. But here is our normative stance. We have previously referred to our thoughts around monetary policy having, in truth, only income inequality impact. Rather than rate cuts being passed on, we think the inquiry should expand to the state of corporate and business lending in this country. If not that, please consider a Fannie Mae or Freddie Mac Australian version where the other institutions are squeezed into corporate lending as a matter of no choice and put downward pressures on rates in actuality. This might have the added advantage of being a good long term structural reform since this would also boost credit growth into productive (rather than speculative) sectors such as businesses that continuously and on an ongoing basis actually employ people.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim