|

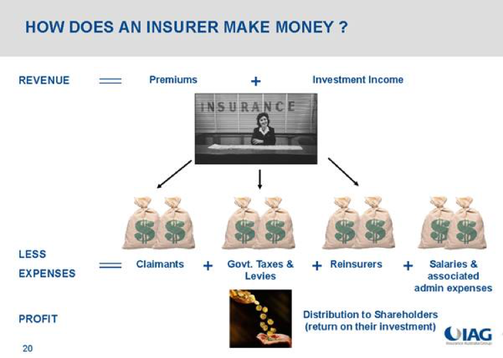

Guy Carson takes a look at the three major players in the Australian insurance space. How do they work and is there value to found in QBE, IAG and Suncorp? Australian Insurance: Is there quality and value? Guy Carson The Australian General Insurance landscape is dominated by three players: IAG, QBE and Suncorp. Over the last decade, investors in these companies have seen significantly different outcomes. In order to understand why, it’s important to look at how insurers make money and how they can insulate themselves from disasters. How does an insurer make money? The below graphic from IAG shows us the basic business model.  Source: IAG Essentially, an insurer receives income from premiums and investments and in turn faces claims as well as various expenses. The difference between the two becomes the profit. The confusing thing for investors is that whilst the business model is simple, the terminology used can be confusing. For example most insurance companies quote three different numbers when it comes to premiums:

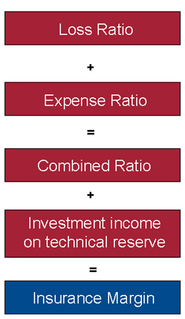

For earnings and valuation purposes it is the Net Earned Premium that matters although it is important to keep an eye on Gross Written Premium to see how the company is growing. From Net Earned Premium we can then subtract the claims received as well expenses incurred in the course of business to arrive at the Underwriting Profit (or Loss). The first important step in choosing an insurance company is ensuring it makes an Underwriting profit.  Source: IAG The great thing about owning an insurer though is that profits can be boosted by investment. The company holds a float of technical reserves (or policy holder’s funds) and can use these to generate further income. This is often referred to as an earnings multiplier.  Source: IAG Furthermore the company can invest shareholders’ funds and gain further income that way.  Source: IAG So that’s how the business model works. The question is how do we analyse whether an insurance company is performing well? For that there are a few simple ratios that help us understand how the underwriting business is performing. These are:

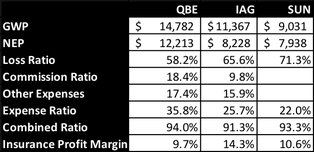

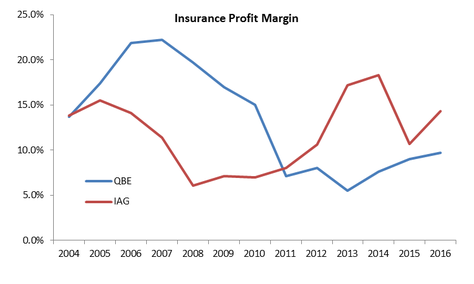

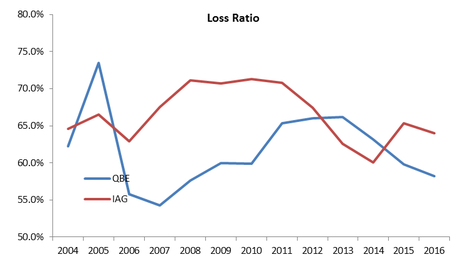

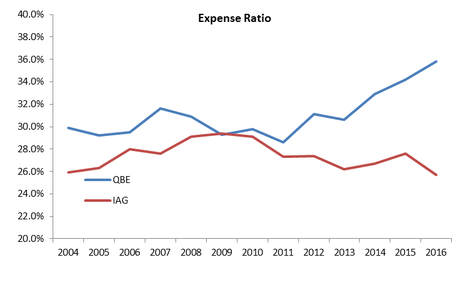

These two ratios together equal the Combined ratio. The combined ratio plus the investment returns earned give the Insurance Profit Margin. This margin describes the profitability of the business.  Source: IAG So how do Australia’s general insurance companies stack up on these metrics? The table below is a summary of the most recent annual results from QBE, IAG and Suncorp.  Source: Company filings & Thomson Reuters In the table we have separated the expense ratio into two parts for QBE and IAG – commissions and other expenses. This shows one of the critical differences between the QBE model and the other players. Companies with stronger brands tend to pay away less in commissions to sell their products. IAG in Australia and New Zealand has a number of well-known brands (think NRMA, CGU and more recently Coles Insurance). In their expansion overseas QBE took a strategy of rolling up smaller players, in doing so they have ended up with a significantly higher commission base and hence higher expense base. This additional cost pushes up their expense ratio and makes the company less profitable. In the early days of the expansion, the company appeared to be doing well despite this higher expense base. Their Insurance Profit Margin rose strongly through to 2007 as can be seen below. The drivers included increased premiums, increased investment returns and a benign claim environment.  Source: Company filings & Thomson Reuters IAG on the other hand had a different experience, after a difficult period from 2006 to 2008, the company has seen a strong recovery in their performance. The key reason the company struggled in that three year period was a rise in claims with the loss ratio rising above 70% as seen in the chart below.  Source: Company filings & Thomson Reuters QBE saw claims rise significantly from 2008 to 2011 and the share price followed suit with a steady decline. One of the problems that QBE has is that its expense ratio is consistently higher than IAGs (due to the reasons discussed above). This means that its profit margin is more sensitive to changes in claims. In our opinion, the simplest way to define quality in Insurance companies is those with lower cost bases and lower expense ratios as they can withstand disasters more effectively. On this basis, we would say that IAG is the quality insurance name listed in Australia. Particularly given that after the difficult 2006-2008 period, the company came out with a renewed focus on costs and has reduced its expense ratio significantly since then.  Source: Company filings & Thomson Reuters Of course, defining quality is only part of our investment process. We also have to take into account valuations as well. To this end, one challenge facing Insurance companies is the current low interest rate environment. Low interest rates mean the return on both the policy holders and shareholders’ funds are now lower than previous and hence the multiplier effect is no longer as strong. This suggests that insurance margins moving forward are unlikely to reach the highs of yesteryear. As a result it is also unlikely the shareholder returns of the past will be repeated.

Everything has its price though the question remains whether there is value right now. To that end we believe the market is currently pricing a solid recovery for QBE on the back of improving signs in its US business with the company trading on 13.1x forward earnings with expected growth this year of over 20% and further growth in FY18. The company can’t afford for anything to go wrong in this recovery. Meanwhile, IAG is priced fairly fully at 17.3x with earnings growth expected over the next few years of around 10% (after stripping out the impact of the Berkshire Hathaway quota share arrangement). Any increase in claims will likely weigh on the price. So in our opinion there appears to be no obvious value at the moment; however it is worth keeping an eye on the sector as share prices tend to overreact on events outside of the companies control such as weather related events. When share prices correct due to these events, they can quite often be solid longer term opportunities.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim