|

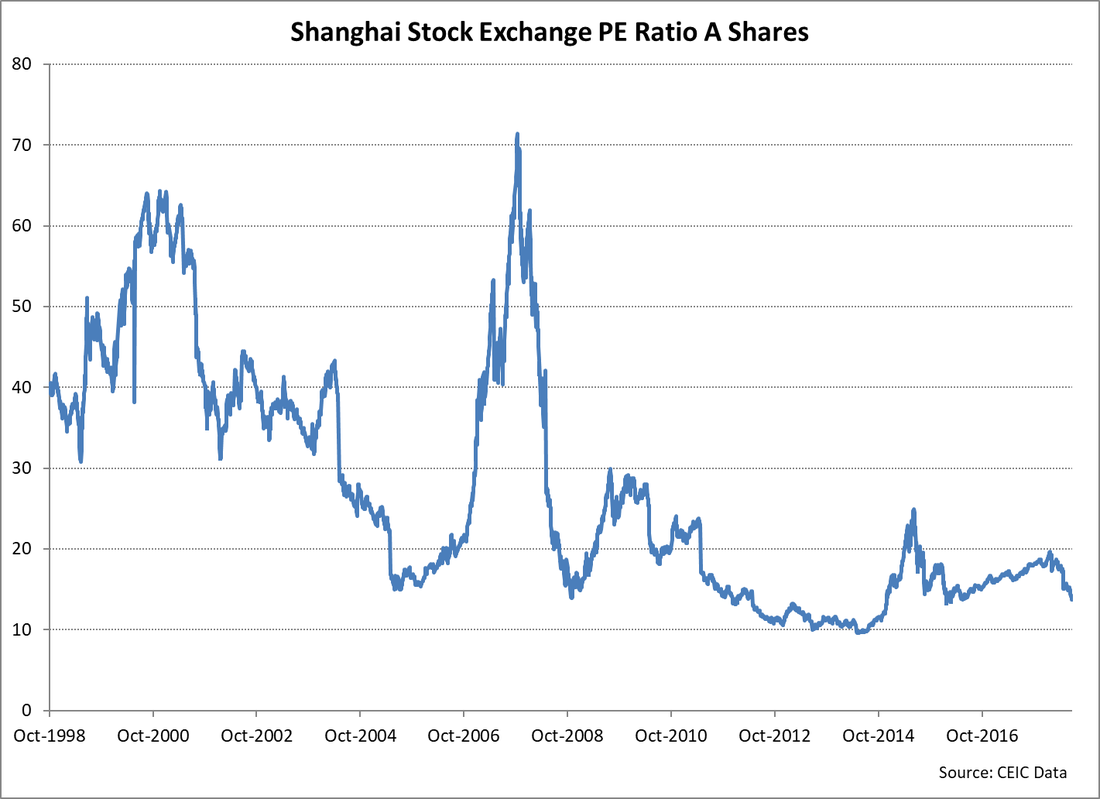

Kevin Smith, portfolio manager for the Asian Small Cap IMA reviews his 25 year history of investing into Chinese shares. Given the current interest in Chinese equities we thought the article was a timely primer to educate global investors on the history of the Chinese equity markets. A recent Barron’s article by Bradley Krom and Matt Wagner highlighted the complexity of accessing Chinese equities across the two share classes domestically and five share classes internationally. Chinese Equities: Market Access, Equity Benchmarks & A-Shares The article prompted me to look back through my own history of investing in Chinese equities which has spanned all seven of those share classes at various times in the past 25 years. The modern era for organised stock exchanges in China started in November 1990 when the Shanghai Stock Exchange was established followed a few days later by the Shenzhen Stock Exchange, by mid-1991 there were 10 companies, all state-controlled enterprises, with listed A shares on the two exchanges. Chinese companies had the choice of listing A shares for domestic investors, B shares for international investors or both classes. The first B shares listed in 1992 and I was one of the pioneer investors, it wasn’t a pleasant or profitable experience, those early to market companies available to international investors became known as the “Killer Bees”. In the period since 1992 China B shares on the Shanghai exchange have recorded a compound return of just 4% per annum versus 12.8% per annum for the A shares. The chart shows the performance of A and B shares in USD terms on the Shanghai exchange in the period since 1992. The chart demonstrates the need for tolerance of volatility to benefit from the long-term share price appreciation of A shares.  In 1993 Chinese companies were permitted to list on the Hong Kong Stock Exchange, these issues became known as H shares and for many years H shares became the main form of access to equities in China proving much more popular than the B shares. Chinese companies are not permitted to list both B and H shares, so there has been a steady migration of companies delisting their B shares to launch H shares. Today there are 3,530 listed A shares in China with a market value equivalent to USD 7,593 billion while the 99 remaining B shares have a market value of less than USD 23 billion. At the end of May 2018, 230 Chinese companies with listed H shares on the Hong Kong Stock Exchange had a market capitalisation equivalent to USD 891 billion. The H shares have proved a good environment for investment returns, together with Chinese companies incorporated outside mainland China and listed in Hong Kong known as “P Chips” and “Red Chips”. The total return attributable to H shares with dividends reinvested over the past 25 years is 10.1% per annum. There is a significant additional risk factor when investing in H shares, the premium or discount versus the A share in the same company. In most cases the A share will be the primary source of liquidity and share price performance, much of that performance can be offset or improved by a changing discount or premium in the price of the H share. At the time of writing there are 76 companies H shares trading at a discount of more than 20% versus the A shares, the widest discount is currently 83% and the biggest premium 55%. Access to the China A shares for international investors changed dramatically in 2002 with the introduction of the scheme for Qualified Foreign Institutional investors (QFII). An initial quota value equivalent to USD 4 billion gradually increased to USD 81 billion by 2015 with 279 institutions participating in the scheme. Institutions managing in excess of USD 5 billion of client assets could apply for QFII status, the approval process could at times be very frustrating. In 2005 one of my then colleagues decided to make camp at the offices of the China Securities Regulatory Commission (CSRC) in order the facilitate the final approval to invest, after several days of waiting the unorthodox approach worked. The whole process for investing was extremely cumbersome due to the involvement two government bodies, the CSRC and the State Administration for Foreign Exchange, the latter body was responsible for initial quota allocation and permission for foreign exchange transfers into and out of China. The time taken to receive any one of the required permissions could be measured in weeks, months and sometimes years. There was another problem that plagued QFII investors for many years up until 2013 regarding the opaque rules for capital gains tax, prudent international investors made provisions for taxes that lacked certainty regarding implementation for more than a decade. Investing in China A shares took a major step forward in 2014 and 2016 when the Stock Connect programme was launched to allow investments to take place between the Hong Kong Stock Exchange and the exchanges in Shanghai and Shenzhen. Transactions from Hong Kong investing in China are known as Northbound trades and investments emanating from China into Hong Kong are Southbound. Stock Connect now extends to 2,000 participating companies in China and offers market access to a broader range of investors. In the period since 2014, total Northbound capital flows (buys minus sells) have amounted to USD 77 billion while Southbound capital flows were USD 104 billion up to the end of May 2018. In the space of a few years, Stock Connect has built up an internationally owned exposure to China A shares equivalent to the build up of QFII held assets spanning more than 15 years. The development of Stock Connect has at long last started to level the playing field for international investors investing in the domestic Chinese equity markets. The gradual expansion of coverage in the Stock Connect scheme should provide an investment environment that is fair to all participants.  The chart shows Shanghai A shares price to earnings valuations going back 20 years. The market is prone to periods of extreme over valuation while the best entry points are when the market trades below 15x earnings. With the current market valuation at 13x together with the fairest level of market access being offered to international investors, I am enjoying investing in China more than at anytime in the past 25 years.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim