|

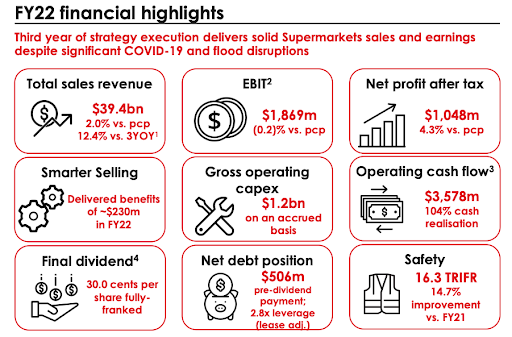

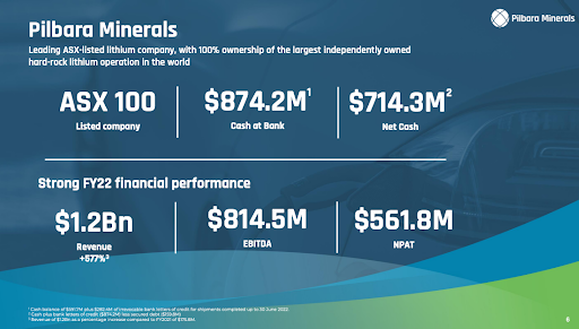

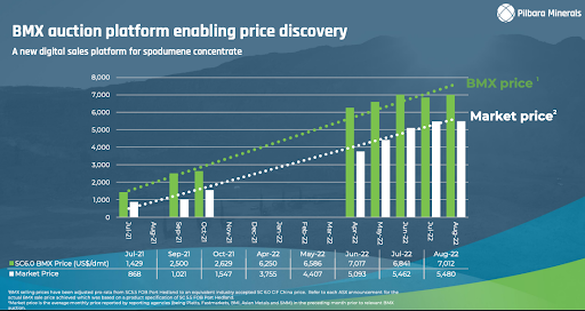

Has COVID-19 helped inflated earnings season results? This week we examine five ASX companies in different industries, with differing results... This week we analyse Coles Group (COL), Monadelphous Group (MND), Pilbara Minerals (PLS), SKY Network Television (SKT), and Viva Energy Group (VEA). So far, we have seen most companies report somewhat positive results for FY22, which isn't a shock due to the recovery from the impact of Covid over the past year. This time around, management teams aren't complaining about face masks but rather the cost of living rising and how expensive lettuce is. Most companies are beginning to see the impacts of rate hikes and falling consumer sentiment. However, FY22 results for most companies have not reflected this... Coles Group Ltd (COL.ASX) Source: Company filings As mentioned with stocks like CBA in our previous article, it's always interesting to look at the results from some of the larger ASX companies to gauge consumer sentiment and how individuals deal with inflation and other economic challenges. Coles Group Ltd (COL.ASX) saw its revenue increase 2% to $39.75bn. The supermarket division's revenue is up 2.2% to $34.62bn, and the liquor division lifted 2.5% to $3.6bn, with gross margin growth achieved in both categories. On the other hand, the cost of doing business has created pressure and eroded EBIT margins. Coles experienced $240m in COVID-19 costs which hurt the company's full-year bottom line. Coles declared an improved final dividend of 30¢ (up from 28¢) after growing its 2022 profit by 4.3% to $1.05bn. Coles saw Fresh food inflation of 4.7% driven by bakery products, reflecting higher wheat prices and fresh produce prices because of the Queensland and NSW floods. FY23 will be a vastly different trading period for supermarkets due to the new landscape. COVID-19 saw people panic buying staples and emptying the shelves in desperate fear that COVID-19 would spell the end of our toilet paper supply. However, moving forward, as consumer demand shrinks due to higher interest rates and food prices rise on the back of inflation, customers will likely be doing the reverse and shopping less frequently. Coles is now seeing a trend towards more inexpensive purchases such as canned food and frozen options. While Coles didn't give guidance for earnings or revenue, they expect to open twenty new stores in FY23 and are guiding towards a CAPEX of $1.2-1.4bn, in line with FY22. Monadelphous Group Limited (MND.ASX)Monadelphous Group Limited (MND.ASX) shares soared higher as they announced an 11% increase in FY22 NPAT to $52.5m. The company provides engineering and maintenance services to the mining, energy and infrastructure sectors. The key drivers of the rise included record maintenance revenue, coupled with strong demand across resources and energy sectors. The result is all the more impressive given higher labour costs in WA, which is an enormous challenge for labour-intensive companies in the industry. While the broader economy is facing unforgiving difficulties, the world's ferocious charge towards electrification continues to drive the mining sector. Companies like MND find themselves winners from this momentum and will continue to see elevated order books (MND have $1.4b work in hand) while also sitting on a healthy cash balance of $183.3m.  Source: Company filings The market generally does not favour engineering companies/contractors due to reasons such as; exposure to cyclicality and non-recurring revenue. Nevertheless, the sector has quietly flown under the radar in recent times. We could be witnessing the start of consolidation, with MACA Ltd, a mining contracting company, being the subject of eye-catching bids from industry heavyweights Thiess and NRW Holdings. NRW looks set to miss out after the MACA board ruled Thiess's bid superior. NRW may increase their bid or might just set their sights on another target. MND is sitting on a healthy cash balance of $183.3m, which enables the company the liberty to pursue an M&A strategy of their own. Pilbara Minerals Ltd (PLS.ASX) Source: Company filings As we've spoken about before, Pilbara Minerals Ltd (PLS.ASX) is an emerging lithium company producing spodumene concentrate with operations in the Pilbara region in Western Australia. PLS has 100% ownership of the world-class Pilgangoora Lithium-Tantalum Project ("Pilgangoora Project"), the world's largest independent hard-rock lithium operation. PLS reported its FY22 results this week, recording a maiden profit of $532.6m, up from a 21.6m loss last year. PLS produced 377kt of lithium hydroxide at a realised price of USD$2,382. PLS continues to fetch prices above the market value thanks to their digital sales platform for spodumene BMX (Battery Metals Exchange); this has seen PLS take advantage of higher lithium prices. This is amid a looming supply deficit for the battery-making material and growing demand for electric vehicles (EVs).  Source: Company filings PLS is forecasting to increase production for FY23 at 540,000–580,000dmt (Dry metric tonne) as they ramp up capacity at the Ngungaju plant. PLS said that costs are expected to be higher during FY23 due to elevated strip ratios and the ramp-up in production of the Ngungaju plant. In the Longer term, PLS are targeting the production of 1mdmt of Spodumene per annum. Given that they are achieving all their targets thus far and implemented various successful initiatives like their digital sales platform - BMX, it's in the realm of possibility for a well-run company like PLS. SKY Network Television Limited (SKT.ASX) Source: Company filings SKY Network Television Limited (SKT.ASX) reported a solid result, with revenue increasing 3.6% to $736m and NPAT hitting the top guidance range at $62.2m. Investors would be delighted to hear that SKT is finally leveraging capital management, reinstating dividends with a proposed 40cps capital return. Customer relationships were up 4% to 991k and SKT continued to invest in their higher margin streaming capabilities and other growth initiatives such as the new skybox and SKY broadband. While the advertising segment only represents $48m of SKT's revenue, we expect this number to decrease as consumer demand slows. This softer advertising market will be more than offset by the rebound in commercial sales and the growth in streaming customers. Looking forward to FY23, SKT released the following guidance:

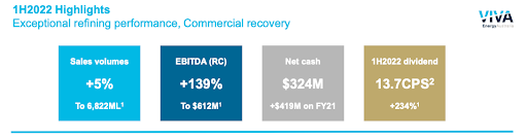

Viva Energy Group Ltd (VEA.ASX) Source: Company filings Viva Energy Group Ltd (VEA.ASX) released a strong 1H22 result on the back of higher energy prices resulting in a turnaround in profits. Viva Energy operates a refining business and supplies a network of over 1300 service stations across the country. It announced an increase in sales volumes of 5% to 6,922Ml, and more than doubled its EBITDA to $612m. VEA now finds itself in a solid net cash position of $324m, up from net debt of $95m last year. The strong results saw VEA announce a 13.7c dividend which was more than triple last year's 1H dividend. VEA's commercial business was the shining star in the results, with EBITDA from this segment increasing 55% to $164.3m. The retail segment saw increased volumes, but EBITDA fell due to higher costs and compressed margins. The higher fuel prices will continue to affect the retail segment. The bulk of VEA's EBITDA is attributed to the refining business segment. This division brought in $370.8m on the back of higher energy prices due to the Ukraine/Russia conflict, material under investment in energy supply, and lower exports from China. The Geelong refinery operated near total capacity, and VEA will continue to Progress with the Geelong energy hub securing government funding for refinery and storage upgrades. Looking forward to FY23, VEA will continue to see high margins for their refining segment from higher energy prices and strong demand from commercial sales. However, margins seem to have peaked and are beginning to soften. VEA also had to deal with a recent outage of a catalytic cracking unit (a piece of refining equipment used to convert crude oil into lighter petroleum products), putting further pressure on the company. Disclaimer: SKT.ASX, VEA.ASX and PLS.ASX are currently held in TAMIM portfolios.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim