|

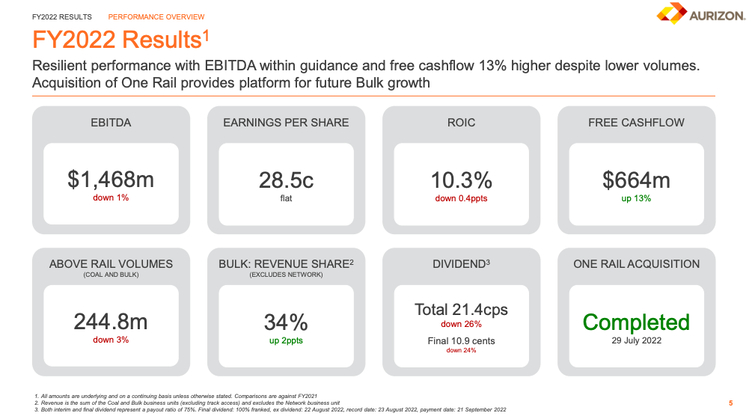

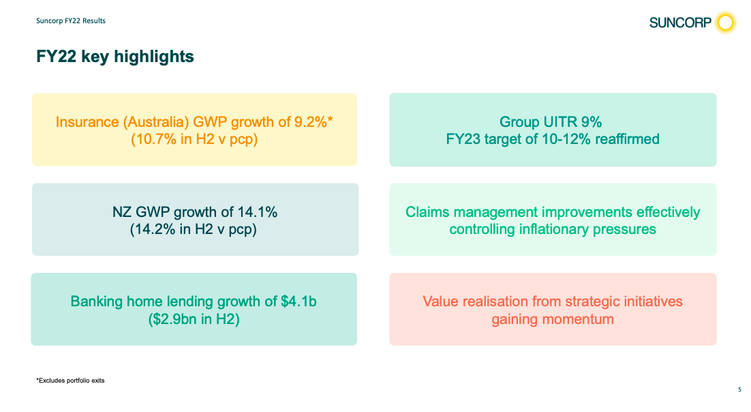

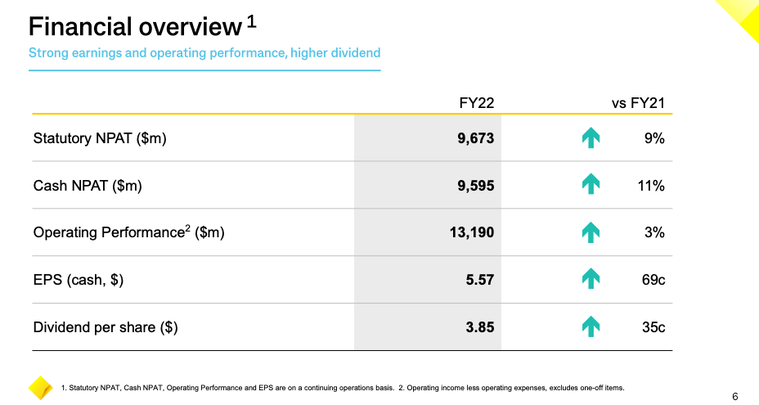

As we head into the much anticipated full-year reporting season, investor eyes will be on management commentary around inflationary pressures, how they are affecting costs and the subsequent outlook for margins moving forward. Attending earnings calls of companies from various sectors can give you an insight into how each industry is dealing with the current challenges as well as what to expect in the next financial year. Listening to the management teams of big banks, for example, will also give us a direct insight into leading economic indicators such as house prices and lending activity. Heading into the recent dip in equity markets, ASX balance sheets were far stronger than in 2020 when we saw plenty of companies going to market to raise additional capital. Given the current climate it’s expected that companies will be more cautious about dividends this year, something Aussie investors don’t take lightly. It will also be interesting to see how hawkish FY23 guidance will be given that the full impact of the current economic challenges won’t be reflected in FY22 results. This week we will be diving into the results of Aurizon (AZJ.ASX), Suncorp (SUN.ASX) and Commonwealth Bank (CBA.ASX). Aurizon Holdings (AZJ.ASX)Results  Source: Company filings AZJ continues to achieve strong cashflow in challenging environments. With most of Aurizon’s contracts secured by CPI escalators, AZJ has been a favourable stock in the current climate. AZJ saw a negative market reaction to their FY22 results following a 26% dividend cut. AZJ pivoted to the lower end of its dividend payout ratio in order to manage the recent One Rail acquisition. Despite lower above rail volumes, AZJ was still able to hit EBITDA guidance and increase free cashflow to $664m (+13%) due to the improved revenue quality from its coal segment. However, the period didn’t come without its challenges. Extreme weather events caused a number of Aurizon’s northern rail lines to shut down for up to five weeks due to the flooding. The total EBITDA impact from this weather and lower volumes was approximately $10m. AZJ also lost a major customer and had to book one-off start-up costs for a new grain contract with CBH Group. Outlook AZJ’s strategy is evolving to diversify away from coal, shifting exposure towards bulk commodities. This is an effort to decrease exposure to a dying industry as well as improve their ESG profile, allowing investment flows from the larger institutions and superfunds. Aurizon’s recent acquisition of One Rail supports this strategy by increasing Bulk’s share of revenue to 42% and is projected to be EPS accretive by 10%. AZJ will also be divesting One Rail’s coal operations through the East Coast Rail divestment, which did $137m of EBITDA last year. Management noted there is strong interest from buyers and are expecting non-indicative bids in September. They are looking to have completed the sale by Q2FY23. Looking forward, FY23 should be an easier period for Aurizon as they have already incurred the start-up costs for new contracts and hopefully won’t have to cease any more operations due to flooding. The WA labour market remains tight which puts pressure on its costs but AZJ should also see a boost to its top line from higher energy prices as they typically come in at a 3-month lag. Australia saw coal production decline in FY22 but higher coal prices should support growth in production for FY23, a tailwind for Aurizon. Moving onto grain, AZJ gives investors exposure to the food market which is currently in a tightened state as a result of the Russia/Ukraine conflict (Russia/Ukraine being responsible for supplying 30% of the world's grain). Australia exports 70% of the grain it produces and there is a significant opportunity for Australia to support the market. Aurizon has the infrastructure to enable this. Their One Rail acquisition saw synergies of $10m realised from day one and Aurizon is guiding towards 1470-1550 EBITDA for FY23. Aurizon is currently trading on an LTM free cash flow yield of 9.3% following the results. Suncorp Group (SUN.ASX) Source: Company filings Like AZJ, Suncorp’s shares also took a tumble on the news that they too were slashing their dividend. Suncorp's NPAT fell 34% to $681m and their final dividend payment of $0.17 was over a 50% decrease on last year's final dividend of $0.40. Suncorp had a tough FY22, enduring 35 natural hazard events which cost the firm $1.08bn in insurance claims. Erratic weather events are to blame for the staggering increases we are seeing in home insurance prices, yet another inflationary pressure passed onto consumers. The result was further impacted by volatility in global markets which impacted the mark-to-market valuations of SUN’s investment portfolios. Despite the challenges there was still some light in the darkness, GWP (gross written premium) growing by 9.2%. Their group underlying ITR (insurance trading ratio) excluding covid impacts increased from 7.9% to 9.8%, roughly in line with their FY23 target of 10-12%. The ITR is the insurance trading result or underwriting result plus investment income expressed as a percentage of net earned premium and is a measure of profitability. Outlook Insurance companies tend to perform better in rising interest rate environments due to the higher yield they earn on the premiums they invest. The mark-to-market impacts on Suncorp’s investment portfolio will reverse as they hold their investments to maturity and their yields will increase as they roll the capital into higher yield investments thanks to recent rate hikes. Given that 90% of Suncorp’s portfolio is invested in investment grade fixed income securities, the reversal of the mark to market prices and the higher yields will help improve their bottom line. Similar to AZJ, Suncorp shareholders are hoping for fewer natural hazard events. Whilst the FY22 period was abundant with them, who can say it won’t be the same moving forward. However, the increase in house insurance will leave Suncorp better protected heading into FY23. Suncorp recently announced the sale of their banking business to ANZ for a cash deal of $4.9bn. The transaction further simplifies Suncorp’s business and allows them to focus on their core operations, i.e. running an insurance company. We see this as an opportune time to be divesting a loan book given the expected slow down in lending; Suncorp could be avoiding an increase in bad debts as interest payments skyrocket. Suncorp may have lowered its final dividend payment on the expectation of the completion of this deal. Expected in H2FY23, this should see a significant capital return to investors in the form of a special dividend. Suncorp also reported progress on digitisation. The proportion of digital sales grew by 6 percentage points in the past year, now accounting for 42% of total sales and service transactions. Suncorp have a long term target of 70% digital/30% voice for insurance sales. This would increase efficiency and decrease costs over time. Commonwealth Bank of Australia (CBA.ASX) Source: Company filings CBA reported a strong operating result with cash NPAT up +11% to $9.595bn. However, the company saw its net interest margin (NIM) slide 18bps down to 1.9%, raising some question marks given recent rate hikes. CBA claimed the Group's NIM declined due to an increase in low-yielding liquid assets and lower home loan margins as a result of intense competition in the mortgage market. During the earnings call, management said there was an opportunity to boost NIMs by taking on more short-term funding but they elected for a more prudent and conservative approach. CBA announced a 10% increase in FY22 dividends to $3.85, bringing their total capital management initiatives for the financial year to $13bn. CBA’s operating result was driven by lower remediation costs, lower provisions, and strong volume growth in home lending which totalled $170bn. CBA reported very favourable figures in terms of bad debts and provisions. The variation on loan impairments was a $357m benefit to profits. Bad debts have been artificially low due to the previous low-interest rate environment coupled with government incentives post covid. Whilst households took advantage of low rates and government stimulus, bad debts are likely to go up in the foreseeable future. An interesting side note: Banks serve to provide capital to facilitate growth in our economy. Without lending from banks, businesses would find it harder to expand and innovate. The rising emphasis investors place on ESG is causing severe underinvestment in oil & gas supply. This is a major contributing factor to why we are seeing higher energy prices today. Additionally, banks and other financial institutions are placed under enormous pressure to stay away from fossil fuels. This is evident as CBA’s exposure to Oil and Gas decreased a further 25% to just $3.6bn in FY22. Outlook CBA’s results didn’t incorporate the full impact of interest rate increases as only two rate rises fell in FY22. About 40% of CBA’s home loan book is on short-term, fixed-rate mortgages that will expire over the next twelve months and will be refinanced at a much higher rate. This will allow for an increase in the spread and, as a result, have positive effects on their NIMs. The effects of this will take a while to flow through. On the flip side, we expect CBA’s arrears to begin creeping up due to higher interest payments flowing through to households. 90-day arrears are currently sitting at 0.49% and it’s only going to climb from here. It’s also important to look at CBA’s economic assumptions as these are the inputs that will drive their impairments and provisions. In CBA’s model, their central scenario - carrying a weight of 52.5% - assumes that the cash rate will be 1.6% in December 2023, the ultimate soft-landing scenario. This assumption is highly improbable and, while it does get set off by a conservative downside scenario, we still see higher impairment expenses which will dampen future results. While bad debts do weaken banks’ balance sheets and overall performance, CBA reported a strong capital position. Their CET1 (common equity tier 1) ratio climbed above pre-covid levels to 11.5%. CET1 measures a bank’s capital against its assets; the higher the ratio the more secure the bank’s capital position is. Their deposit funding also increased to 74% (% of total funding) which is also significantly higher than pre-covid levels (69%). This leaves CBA with a conservative capital position which makes them well positioned to deal with the challenging economic condition that lies ahead. With home lending and house pricing starting to fall, CBA will look to bolster its business lending segment. Business loans for FY22 came in at $33bn, +13.6% YoY. Banks in Australia have been notorious for neglecting business lending due to flawed Basel regulations. Perhaps the new interest rate environment will help reverse this trend as banks seek deposits from businesses which are typically at a lower cost. This allows for increased funding. We shall see. Disclaimer: AZJ, SUN, CBA are currently held in TAMIM portfolios.

1 Comment

William Pentecost

12/8/2022 08:36:38 am

Promising information. Thankyou. WJP Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim