|

This week we are providing an overview of rare earths, a group of 17 elements critical to various industries including energy, defence and aerospace. Rare earths are a geopolitical battleground, with China’s iron grip over the supply chain causing apprehension amongst Western nations. Rare earths have also gained greater investor attention in recent years as they become a key cog in the race to decarbonise the planet.

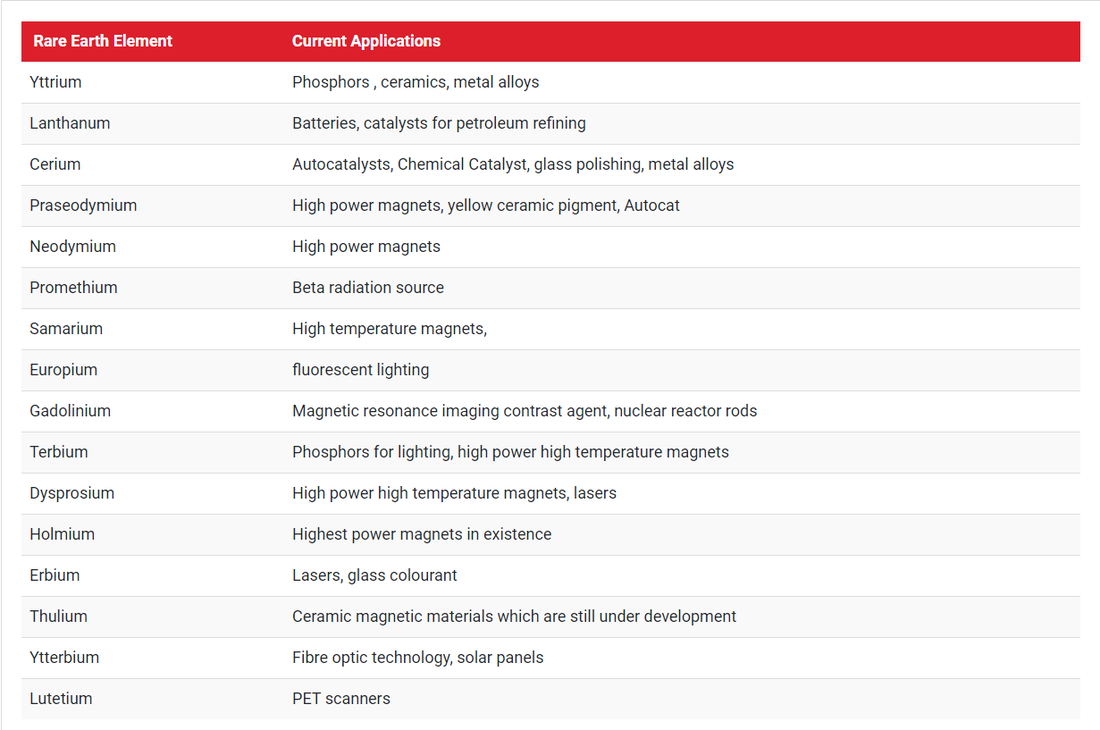

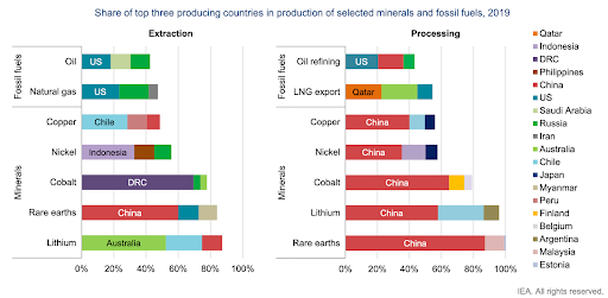

The Global Divide: Rare EarthsAt first glance, it’s hard to find many rare earth elements that roll off the tongue easily. Praseodymium certainly doesn’t. Neither does Ytterbium or dysprosium. Europium might be our best bet.  Source: Lynas Rare Earths Notwithstanding the challenging pronunciation, rare earths will likely become much more common in our everyday vernacular. The International Energy Agency forecasts demand for rare earth elements may see a 3-7x increase by 2040 to aid the energy transition, subject to policy and technology decisions. Rare earth elements are used in a range of applications including wind turbines, fuel cells, batteries and magnets used in electric vehicles. Further applications include military and defence technologies such as missile guidance systems and submarines. Rare Earths 101Contrary to thought, rare earths are not rare at all. Such materials can be found throughout the Earth's crust. What makes them special is that they are not usually found in high concentrations, limiting the number of economically viable deposits. Rare earths are typically mixed together with other elements, making refining and processing a cumbersome endeavour. There are associated high costs, in terms of energy and externalities such as greenhouse gas emissions, environmental damage and health risks. Occasionally you will hear critical minerals and rare earths used interchangeably, however, this is incorrect. Critical minerals is an umbrella term usually used by governments, that includes rare earth elements but also others such as lithium, copper and graphite. Just like Toyota is not the only car company, rare earths are not the only critical minerals. China’s StrangleholdHowever, unlike the global car market where no one competitor has a majority market share, China has an iron grip on the extraction and processing of rare earths. Its dominant position is no accident. Since the 1980s, the government has made rare earths a priority via supportive regulation and tax rebates. The industry also benefited from relatively low labour costs, with mines in other countries unable to compete. Former leader Deng Xiaoping is reported to have said in 1992 “While the Middle East has oil, China dominates rare earths”. Over time, industrialised countries became dependent on China as an exporter of rare earth alloys, magnets and metals. In 2010, China attempted to limit exports of rare earths, with the price soaring more than ten-fold for many elements. This sent off warning bells – particularly for Western nations, of China’s stranglehold on the rare earth supply chain. At the time, China’s share of global extraction was 97%.  Source: International Energy Agency The US and Australia have since boosted production, with China’s share falling to 60% today. However further down the supply chain China retains a tight grip, with 85% of refining capacity and 92% of permanent magnet production under its control. Governments are attempting to secure their own supply chains by incentivising companies to invest onshore. The US recently introduced a bill that would offer tax credits for rare-earths magnets produced onshore. Closer to home, Iluka Resources (ASX: ILU) was lent $1.25 billion by the government to build a fully-integrated rare earth refinery in Western Australia. The US Department of Defence provided Lynas Rare Earths (ASX: LYC) with US$120 million last year to build a heavy rare earths refinery in Texas. Rare Earth Companies on the ASXFor investors looking for exposure on the local market to rare earths, a non-exhaustive list of companies (not held in the TAMIM portfolios) include:

Challenges With Rare EarthsDespite the economic incentives, there are several challenges facing existing and new rare earth projects. As mentioned earlier, the process of extracting rare earths is labour and capital-intensive. Current production methods require plentiful quantities of ore for only a small amount of end product.  Source: Mineral Economics The process releases harmful waste, including radioactive water, toxic fluorine and acids. If not managed and disposed of safely, this leaves devastating impacts on the environment and surrounding areas. Bayan-Obo is the world’s largest rare earth mine, located in China. The tailing pond, which has 70,000 tonnes of radioactive waste, is not properly lined. As a result, its contents are approaching groundwater and will eventually reach the Yellow River, a key source of drinking water. Access to capital remains limited. Traditional banks find rare earths too risky and complicated, in addition to concerns over environmental, social and governance (ESG) practices. This has led to governments and even customers stepping in to fill the void. And for new entrants, there is a sizable knowledge gap. Only two companies have processing facilities outside of China and Myanmar: Lynas and MP Materials. Building supply chains takes not only immense capital and time but also technical expertise – something China has been developing for decades. Given the geopolitical and environmental challenges, some companies have chosen to reduce their reliance on rare earths. Certain Tesla (NASDAQ: TSLA) and Mercedes (ETR: MBG) induction motors utilise no rare earths. Companies are also looking to be more sustainable practices. For example, the latest iPhone has 100% recycled rare earth elements in all magnets. The TAMIM TakeawayThe ongoing tension between the West and China is unlikely to reverse course in the near future. This should buttress demand for rare earths, as nations move to future-proof their supply chains and onshore activities. New industries such as electric vehicles in addition to government-stated climate targets will further underwrite demand for these critical minerals.

If you’re looking to gain exposure to industries with underlying tailwinds such as rare earths, consider reading more about The TAMIM Global Mobility fund. This strategy seeks to capitalise on the autonomous and electric vehicle revolution, for which future-facing commodities will play an integral role.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim