|

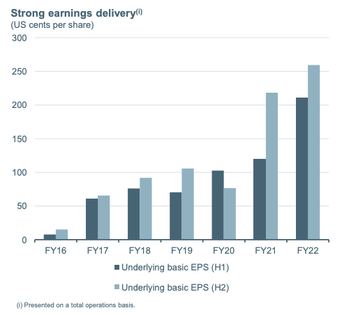

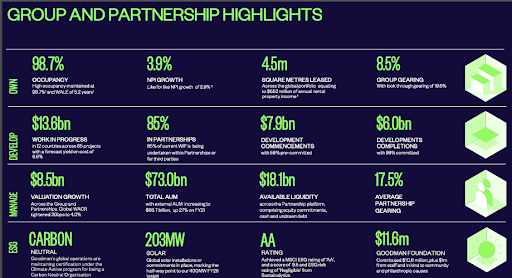

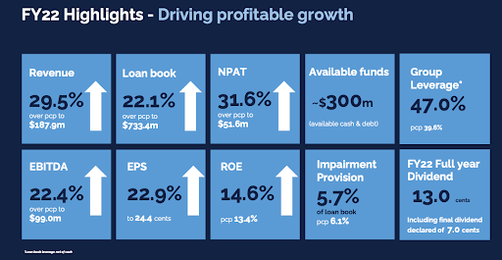

August reporting season keeps on rolling as highly anticipated FY22 results from ASX: BHP, ASX: MNY and ASX: GMG are analysed below... BHP Group (ASX: BHP) Source: Company filings Investors were focused on the earnings report of ASX’s largest listed company, BHP Group Ltd (ASX: BHP). BHP’s FY22 result would either pull the ASX higher or drag the index lower, as the company accounts for 8.5% of the total capitalisation of the ASX index. BHP reported a profit of $21.3bn, up +39% from the previous year which flowed through to a +8% increase in dividends for FY22 (325 US cents per share). Keep in mind these results don’t include BHP’s capital return from the merger of BHP’s petroleum arm with Woodside. The proceeds from the merger bring the total capital return to circa $36bn. It is important to note that BHP reported these strong results on the back of a booming commodity cycle while keeping costs under control. As part of BHP’s plan to invest in more future-facing metals such as copper and nickel, BHP is currently attempting to take over OZ Minerals (ASX: OZL) for its extensive copper portfolio. OZL has rejected BHP’s initial offer of $25 per share, and investors are awaiting their next move. CEO Mike Henry shrugged off the rejection and sees opportunities beyond OZL to grow internally and pursue other M&A opportunities. Given BHP’s performance and expansive balance sheet, we can expect BHP to be active in the M&A space regardless of the outcome of the takeover attempt on OZL. How much leverage does BHP currently have to copper? The answer is not as much as they’d like. For every $1/lb increase in the price of copper, BHP earns USD $31m in EBITDA. We expect BHP to gain far more exposure to copper through tier 1 porphyry deposits. Looking forward, inflation will be a headwind for BHP, and while the board has adequately managed costs, we expect them to be more apparent in FY23. CAPEX for FY22 came in at $6.2bn; BHP’s medium-term target is $10bn, which is a significant uplift as mining expenditures continue to rise. China’s zero-COVID policy has been a headwind for iron ore consumption, and an economic downturn puts a damper on new development, adding to potential future headwinds. China’s consumption remains a crucial driver for BHP’s most profitable mineral, Iron ore. Goodman Group (ASX: GMG) Source: Company filings GMG saw their assets under management rise by +26% to $73bn, and EPS increase +24% to 81.3 cps, ahead of guidance. Despite the strong result, Goodman kept FY22 dividends unchanged at 0.30. Goodman’s partnerships recorded $8.5bn of revaluations, which led to a +25% uplift in NTA. Furthermore, Goodman reported strong growth in rental yields on the back of high occupancy and low levels of supply, leading to higher property valuations. Their development pipeline remains strong, and they believe rental growth is outpacing construction prices. Lastly, Goodman's gearing is low and currently sits at 8.5%, which means they will absorb less of a negative impact from rising rates. In terms of the forward outlook, Goodman’s FY22 guidance aims at EPS growth of +11%. However keep in mind, Goodman typically upgrade guidance throughout the year. Money3 Corporation Limited (ASX: MNY) Source: Company filings Auto Finance company, Money3 Corporation Limited (ASX: MNY) reported a strong result, in line with guidance and expectations. In FY22, MNY reported a +31.6% increase in NPAT to $51.6m and saw their loan book grow +22.1% to $733.4m. Credit quality continued to improve on the back of government incentives and increased car prices. In line with what the company saw in FY22, MNY forecasts bad debts of between 3.5%-4.5% for FY23. So far, MNY’s funding has included a large portion of equity. This puts their group leverage at 47%, which is relatively low for a non-bank lender. MNY recently established debt warehouses, which means that MNY’s cost of funding will decrease as they gain more credibility and scale. MNY is currently sitting on $300m of funding headroom by increasing leverage to around 75% (what management is comfortable with), which will see their ROE improve. Management also flagged the opportunity to grow through M&A by acquiring loan books; this is definitely a company to watch heading toward the end of the calendar year. The New Zealand segment has struggled to see meaningful loan origination growth. However, management cited that on Monday, there was a record $1m originations in NZ, which could be a turning point. MNY declared a final dividend of $0.07 per share, taking the FY22 total distribution to $0.13 per share, representing a 5.5% dividend yield. MNY have been utilising share repurchase plans, and management said they would continue to buy back shares if the share price remained undervalued. Given that they are sitting on a large balance of franking credits, dividends will remain a focus for investors regarding capital management. While MNY is confident in its loan book quality, management is guiding toward 20% growth in the loan book for FY23. Seven West Media Ltd (ASX: SWM) Source: Company filings Seven West Media Ltd (ASX: SWM) reported a mixed set of result for investors. There was a +21% increase in revenue to $1.54bn and EBITDA increased +35% to $342m, the strongest EBITDA result since FY17. However, investors were once again left short on the capital management front; SWM is sitting on $102m worth of franking credits, and investors are eagerly awaiting the return of dividends. Unfortunately, investors will need to wait a little longer for these highly anticipated pay-outs. SWM instead announced a buyback of up to 10% of shares. The buyback does make sense, given SWM is trading on a PE of less than 4, highlighting the company's undervaluation by the market. The investment community had priced in a dividend payment, which ultimately resulted in the -3.85% decline in the stock price on the day of the announcement (16/11/22). Looking past SWM's capital management, the company's digitalisation continued to grow, with digital earnings now making up over 40% of the group's earnings. Despite the current economic downturn, SWM still forecasts demand to be strong from advertisers. Quarter 1 saw advertising markets down 2%, excluding the impact of the Olympics and SWM are forecasting to grow digital revenue in line with FY22 growth with FY23 capital costs to fall within $1.20bn and $1.22bn. SWM remains in a strong capital position with leverage currently sitting at 0.7x; this allows them to increase leverage should any growth CAPEX, or M&A opportunity arise. Disclaimer: ASX: GMG, ASX: MNY and ASX: SWM are currently held in TAMIM portfolios

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim