|

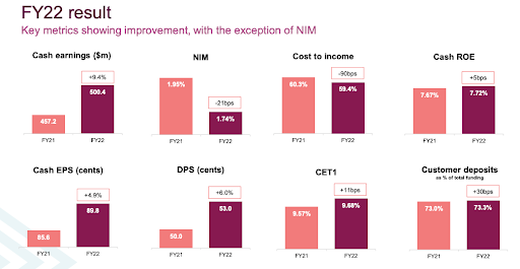

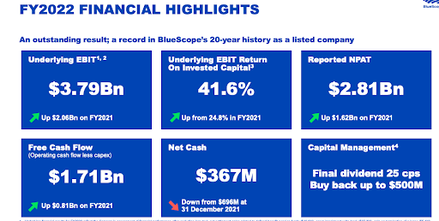

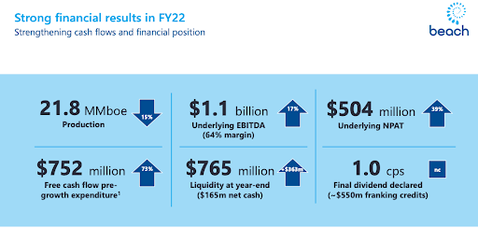

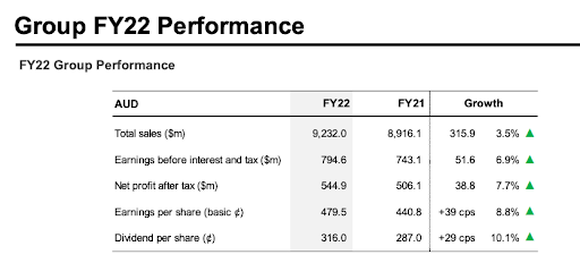

Upon reaching the middle of reporting season, investors continue to analyse company's FY22 results. Today, we take a deep dive into the results of ASX: BEN, ASX: BLS, ASX: BPT and ASX: JBH. Bendigo and Adelaide Bank Ltd (ASX: BEN)Bendigo and Adelaide Bank Ltd (ASX: BEN) recorded a +9.4% increase in full-year cash profit to $500m, which saw the company’s total dividend increase +6% to 53 cents per share (from 50cps FY21). Bendigo saw a net positive from credit expenses and wrote back provisions relating to Covid-19. Bendigo’s results were similar to CBA, the operating result looked strong, but their net interest margin (NIM) decreased by 21bps to 1.74%. Like CBA, Bendigo blamed this on competitive pressures and their funding mix. Bendigo forecasts a 27bps benefit to the group NIM in FY23 and a 46bps benefit over the next three years. What can we make of these forecasted numbers? While these numbers are material given the 21bps decline in FY22, surprisingly, they aren’t as strong as one might think. This gain in NIM is primarily due to Interest rate rises. However, the other result of rate rises is an upsurge in arrears and bad debts. Currently, arrears and bad debts are artificially low thanks to government incentives post-covid. However, without these incentives and interest payments increasing, so will arrears and bad debts.  Source: Company filings Investors didn’t take kindly to Bendigo’s results, with the share price declining sharply at the market open, dropping by over 8%. It will be interesting to keep an eye on ANZ and WBC, as their results should be released in October/November (their financial year ends 30th of September). Both companies will likely also see group NIM fall under pressure due to competition; however, by the time of reporting, they will have been the recipient of the recent rate hikes. Bluescope Steel Limited (ASX: BLS) Source: Company filings Bluescope Steel Limited (ASX: BLS) delivered a bumper FY22 result seeing their revenue and NPAT rise +47.5% and +135.5%, respectively. This result was a record for Bluescope’s 20-year history as a listed company. The development was driven by their North Star mill in Ohio, which makes steel for white goods manufacturers, the automotive industry, and the agricultural sector. This cornerstone asset resulted in a +181% boost in underlying EBIT to $1.9bn. On the back of these positive results, Bluescope announced a 25-cent final dividend and an additional buyback program of up to $500m. Bluescope will invest over $700m USD to expand their thriving North Star operation. The expansion will add 500ktpa of steelmaking capacity. Looking forward, Bluescope expects a weaker result in FY23, with Underlying EBIT in 1H FY2023 expected to fall in the range of $800M to $900M. This is mainly due to significantly lower Midwest US steel spreads and weaker Asian steel spreads. Beach Energy (ASX: BPT) Source: Company filings Beach Energy (ASX: BPT) saw its shares sell down quite aggressively, despite achieving a +39% NPAT increase in the wake of high energy prices. The market's negative reaction can be attributed to BPT's 15% fall in production to 21.8 MMboe (millions of barrels of oil equivalent), in conjunction with a production outlook for FY23, which is far below consensus. Furthermore, Beach Energy is guiding towards 20-22.5 MMboe for FY23 at a unit operating cost of $12-$13 per barrel of oil (boe), an increase from FY22 ($11.74). Beach Energy remains unhedged, which gives investors a pure play on Energy prices. JB Hi-Fi Limited (ASX: JBH)JB Hi-Fi Limited (ASX: JBH) recorded a solid operating result for FY22, seeing a +3.5% boost in sales to $9.232bn and a +7.7% increase in NPAT to 554.9m. JBH also increased its FY22 total dividend by +10.1%, surprising investors. With interest rates rising, central banks seek to reduce consumer demand to battle inflationary pressures. Interest rate increases sharply impact discretionary stocks (like JBH) as the sector relies heavily on consumer sentiment. However, these drivers often have a delayed impact on company economics.  Source: Company filings Furthermore, Global Chipmaker Micron revealed their concerns pertaining to an oversupply of electronic chips in some sectors, mainly due to the decrease in consumer demand and thus production. JBH saw its inventory rise 20.9% to prepare for supply challenges, but they find themselves exposed to any sudden drop in consumer demand. Therefore, while JBH has been a tremendously well-run business over the years, investors should remain cautious when looking at consumer-driven stocks during challenging economic conditions. While markets are forward-thinking, the current financial results include figures from when the economy looked very different from how it does now. Disclaimer: ASX: BEN is currently held in TAMIM portfolios.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim