|

Another week of earnings results showcased the strength of Australian corporates while also alluding to a more difficult environment in 2023... The third week of the annual August reporting season usually sees a notable increase in earnings results. This year was no different, with three of Australia’s best-known companies providing a solid set of results and valuable insights into what to expect in 2023. BHP Group (ASX.BHP)Australia’s largest company achieved its second-biggest profit and subsequently announced its largest annual dividend to shareholders. The market liked the result, sending the BHP share price 4.86% higher on the day to $40.76. Key numbers from FY22 include:

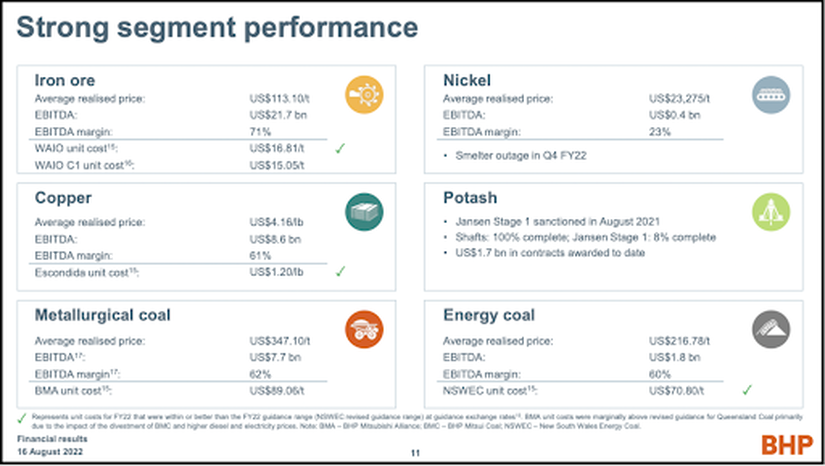

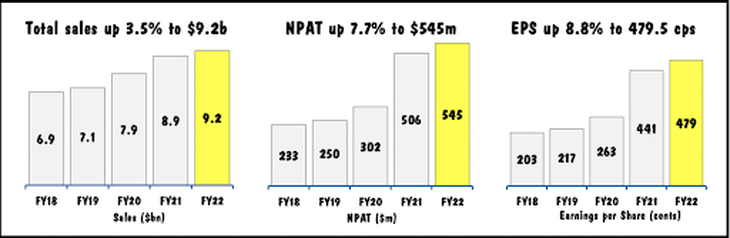

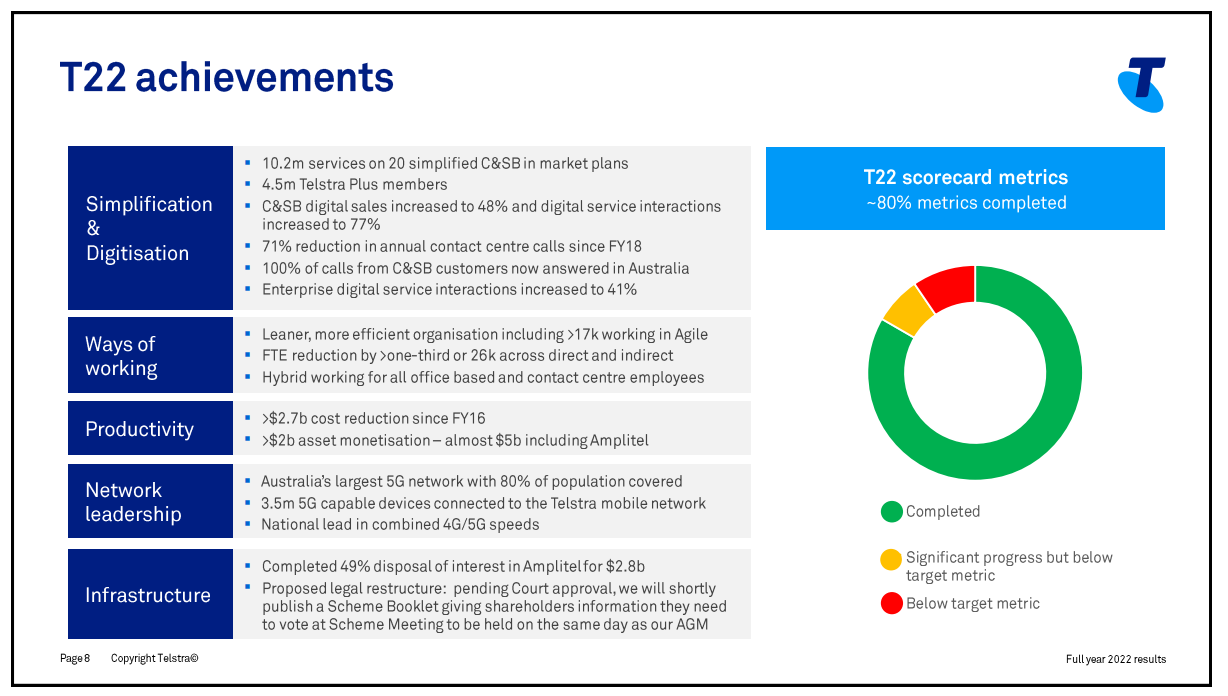

The result showcased that BHP is firing on all cylinders. It recorded no fatalities for the third year while high potential injury frequency fell by 30%. Governments, via royalties and taxes, received US$17.3 billion. Shareholders, representing about 70% of all Australians via direct ownership or superannuation, benefitted from US$36.0 billion in returns. Coal was the standout performer. Underlying EBITDA soared from US$288 million to US$9.5 billion as prices tripled due to tight supply and the European energy crisis. Copper earnings fell slightly to US$8.5 billion from lower volumes, and higher costs at Escondida were offset somewhat by a rising copper price. Iron ore profits fell 17.6% to US$21.7 billion, largely due to declining average realised prices.  Source: BHP FY22 Results Presentation On the operations front, margins inched higher to 65% despite overall unit costs increasing 13% due to a combined US$3.0 billion in extra costs. Potash exploration at Jansen Stage 1 is tracking to plan, while Western Areas expansion is racing ahead. The miner also completed the divestment of the petroleum division to Woodside (WDL.ASX), unified its dual-listed corporate structure and sold off coal assets. BHP is financially robust, with net debt down to just US$0.3 billion from US$4.1 billion in FY21. This will support a planned step-up of annual capital and exploration expenditure from US$6.1 billion to US$10.0 billion over the medium term. It will also enable BHP to pursue M&A opportunities, including the recent (and subsequently rejected) AU$8.3 billion bid for OZ Minerals (OZL.ASX). Looking to FY23, nickel and copper production is expected to increase materially and to a lesser extent, metallurgical coal. Iron ore and energy coal production are expected to either increase or fall marginally. Unit costs will again increase as the lag effect of inflation and increased labour costs flow through. BHP will face a tougher environment going forward. The miner expects a slowdown in advanced economies from higher interest rates and geopolitical uncertainty. BHP is particularly concerned about Europe’s energy crisis and the subsequent impact on commodity demand. China is expected to be a source of stability as the government stimulates the economy for future growth. JB Hi-Fi Limited (ASX.JBH)Despite cycling unique pandemic-induced demand in the prior year, JB Hi-Fi managed to increase sales and profits during FY22. Notable financial results include: • Revenue of $9.2 billion, up 3.5% • Net profit after tax of $545 million, up 7.7% • Earnings per share of $4.79, up 8.8% • Final fully franked dividend of $1.53 per share, up 42.9% Zooming out over two years, JB Hi-Fi has demonstrated strong cost control and benefitted from operating leverage (when profits rise relatively faster than revenue and cost growth). Sales have increased 16.5%, while profit has soared 80.1%. Online sales now represent 17.6% of total revenue compared to just 5.7% pre-pandemic. Including the half-year dividend of $1.63, the business has paid $3.16 in dividends in FY22 in addition to a $250 million share buyback.  Source: JBH FY22 Full Year Results Of the company’s three divisions, The Good Guys stood out, increasing operating earnings by 12.5%. The core JB Hi-Fi Australia business increased earnings by 4.0%. JB Hi-Fi New Zealand achieved a 51.7% profit jump, albeit this is off a very small base. Despite a relatively small increase in sales, inventory finished 20.9% higher. Recently, retailers like Kogan (KGN.ASX) let inventory blow out, leading to discounting and cash flow issues. Positively, inventory and sales have grown in tandem since 2019, alleviating potential concerns. Management also mentioned it had run inventory lower during the pandemic due to supply chain constraints and that current inventory is “all new stock”. While constraints still exist, access to stock is “definitely starting to improve”. After completing a strategic review of the New Zealand business, the retailer believes there is a significant growth opportunity to expand abroad. Subsequently, a new Managing Director has been appointed to refresh the existing store network, open new outlets and relaunch the online website. The big question looming over JB Hi-Fi and other retailers is whether demand will now reverse. The pandemic brought purchases as workers shifted to work-from-home and households splurged on new appliances. Cost of living pressures, including inflation and interest rate increases, are also reducing discretionary budgets. The latest Westpac-MI consumer confidence report indicated that households are 27.3% less likely to buy a major household item than twelve months ago. Somewhat surprisingly, sales have failed to dip. JB Hi-Fi Australia and The Good Guys grew sales growth 9.7% and 7.8%, respectively in July. However, it’s worth keeping in mind that various state-based COVID-19 restrictions impacted trading in July 2021, likely flattering the 2022 numbers. Foreshadowing what might be on the horizon, JB Hi-Fi New Zealand sales fell by 0.9%. The New Zealand central bank has raised interest rates relatively faster than its Australian and international peers. Telstra Corporation (ASX.TLS)Announcing Telstra’s FY22 numbers was likely a bittersweet moment for outgoing CEO Andrew Penn. The telco increased its dividend, albeit modestly, for the first time since 2015, the same year Penn was appointed to the top job. It has been a turbulent seven-year ride (more on that below), with the National Broadband Network (NBN) rollout creating a cumulative $3.6 billion hole in Telstra’s bottom line. Key financial results from FY22 include: • Income of $22.0 billion, down 4.7% • Net profit after tax of $1.8 billion, down 4.6% • Final fully franked dividend of 8.5 cents per share, up 6.3% • Total dividends of 16.5 cents per share, up 3.1% The fall in revenue and profits was largely the result of reduced one-off NBN receipts. Telstra has been receiving payments from the NBN to offset lost earnings; however, FY22 will be the final year of compensation. The performance of the underlying business was strong, with underlying earnings before interest, tax, depreciation and amortisation (EBITDA) increasing 8.4% to $7.3 billion. Earnings from the mobile segment, which accounts for more than 54% of group profit, jumped by 21.2%. Telstra also completed its T22 program, removing the business’s $2.7 billion in costs. The infrastructure division (InfraCo), which will be spun off later this year into its own entity, showcased stellar profit margins of 67.4%.  Source: TLS FY22 Results CEO & CFO Briefing Materials Returning to Penn, much of Telstra’s success today stems from his T22 strategy announced in 2018. Everything is 20/20 in hindsight, but at the time, shareholders loathed him for dwindling profits and subsequent dividend cuts in 2017 and 2019. He has reset the cost base, created more technology-enabled telco and handing over Telstra to current CFO Vicki Brady in far better shape than he received it. Nonetheless, challenges remain, including the lack of profitability in internet Consumer and Small Business products. The division achieved EBITDA of just $55 million despite $4.5 billion in revenue. Other issues include an underwhelming underlying return on invested capital of 7% and inflation-induced cost increases, particularly on planned network upgrades and fibre rollouts. Telstra has guided for income of $23.0 to $25.0 billion and underlying EBITDA of $7.8 to $8.0 billion in FY23. The business also reiterated its medium-term goal of low-mid single-digit earnings growth until 2025. The bigger dividend cheque is mainly symbolic given it represents just a 3% increase on FY21. However, it signals that after years of falling returns, Telstra is ready to return to growth.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim