|

REITs: Have you considered an allocation? REITs provide an easy way to get exposure to property. We discuss how this investment thematic works, and two ASX listed REITs we see good potential in going forward...

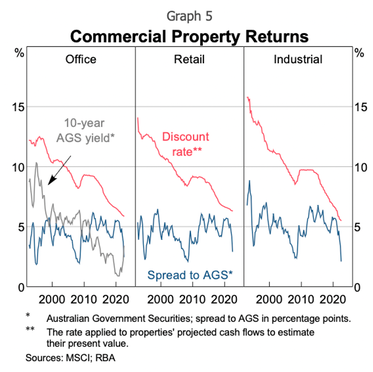

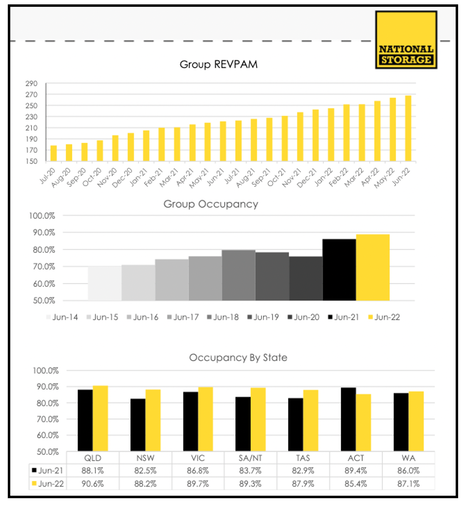

REITs: What's the buzz?Before diving into two of the A-REITs (Australian Real Estate Investment Trusts) held in the TAMIM Listed Property portfolio, we thought it would be timely to provide our thoughts on current property valuations. We, like you, read the news headlines around property prices falling off a cliff as the RBA and other central banks increase interest rates to combat inflation.  Source: Reserve Bank of Australia Undoubtedly property, like all asset classes, will be impacted by rising rates. When interest rates increase, so does the discount rate (known as the cap rate) applied to cash flows from the asset. Future income is subsequently not worth as much, and the net asset value (NAV) corrects to reflect the lower return profile. Interestingly, we have yet to observe this in the deals we are currently being presented, with a clear bifurcation between what sellers expect and what buyers are willing to stump up. The increasing debt cost also means a more significant share of income is needed to repay interest costs, which can impact distributions. Similarly, potential buyers face a drop in borrowing power, as they can no longer serve as much debt, placing further downward pressure on values. The Market has Already ReactedGiven what we have described above, you might ask if it is the time to invest in a listed property. First and foremost, the listed property fund aims to provide capital growth and attractive income distributions. The share prices of REITs might gyrate, but investors are still paid to be patient via quarterly distributions. The second is that property is a long-term investment rather than something to trade in and out of. These assets are owned for decades and inherently benefit from tax advantages such as tax-deferred distributions. Furthermore, tenants are on long-term leases with embedded inflation or fixed-rate annual rent escalations. We are not looking to realise or sell assets in the near term and, therefore, can look through the near-term volatility. Thirdly, the market has already moved to try and ‘price-in’ the impact of higher interest rates. For example, Australia’s most prominent office manager Dexus (ASX.DXS) is trading at a 40% discount to NAV. We are not naive to the headwinds, chiefly greater work-from-home, sufficient supply in CBD areas and rising discount rates. However, the market has already reacted to this news and largely priced in any potential revaluation. All of this gives us confidence in the listed property sector. We do acknowledge, though, that all property is not equal. Investments that look attractive to us are low-gearing or hedged debt, high occupancy and conservative distribution policies. Notwithstanding the aforementioned discount to NAV, we are cautious about commercial property in Melbourne and Sydney. It will take time for this cycle to play out and for buyers and sellers to settle where fair value sits in a higher interest-rate world. 1. Vicinity Centres (ASX.VCX)Vicinity Centres is a retail property REIT owning and managing 60 assets across Australia. It has a well-diversified tenant base, with an average lease tenure of 5.1 years and 94% of leases with at least a contracted annual increase of 4%.  Source: Vicinity Centres In its most recent quarterly update, retail sales across the portfolio increased by 21.2%, underpinned by solid growth in luxury, apparel and footwear. Despite visitations recovering to only 92% of pre-pandemic levels, spending per visit has increased by 30%. This implies shoppers are more purposeful with in-person shopping rather than simply browsing. Leasing spreads - which measure the change in rent from existing leases to new ones - are improving after falling into negative territory during the pandemic. Given retailers have had the whip-hand in lease negotiations over the past two years, this is a positive outcome and highlights the strength of Vicinity’s portfolio. Occupancy is also strong at 98.4%. CEO Grant Kelley announced last month he will retire. While disappointing, the positive is he will remain in the role until June to ensure a smooth handover. The company reconfirmed full-year guidance, including adjusted funds from operations (AFFO) of 10.9-11.5 cents per share, of which more than 95% is expected to be distributed. This places the company on an implied distribution yield of 5.7%. Vicinity Centres has a NAV of $2.36 per share compared to a share price of just $1.91, equal to a 19% discount. With a weighted average cap rate of 5.3% and low gearing of 25%, we think the current price could represent good value. 2. National Storage REIT (ASX.NSR)Readers will recognise National Storage REIT as the bright yellow self-storage provider. The company operates 225 centres and is the largest operator of storage nationally. Despite this, it only commands a market share of around 10%, with the remainder largely fragmented. Storage is an attractive commercial property segment, given the diversification of tenants and leases. It has been a beneficiary of the work-from-home shift, as households increasingly look for alternate spaces. It has also benefitted from the limited supply of dwellings and rentals. This gives the NSR meaningful negotiating power.  Source: National Storage REIT Since listing in 2013, it has pursued a strategy of purchasing or developing new sites to grow the network, resulting in a 28% increase in earnings per year. Management also strongly emphasises technology to streamline operations and reduce costs. Customers can purchase storage on the spot via its online portal. Moreover, occupancy and storage rates are optimised by offering discounts to entice new customers and price increases for lower-yield occupants. The key metric for NSR is revenue per available room (RevPAR), which measures occupancy multiplied by the price of each unit. We saw an increase of 1.2% in the first quarter despite a marginal fall in occupancy. This isn’t much of a concern given 89% of its centres are 80% full, with 35% at 90% or above. The business expects earnings of $133 million or 11.1 cents per share in FY23, implying a minimum growth rate of 5% on the prior year. The distribution is expected to be 90-100% of earnings, implying a distribution yield of around 4.5%. The business’s 23% gearing ratio is below its targeted range, and the cap rate is 5.86%. It is worth noting that NSR trades at a 4.2% premium to its NAV of $2.34. However, given the strong track record of growth and 34 active development projects, we believe it should grow into the valuation and continue its strong performance. Disclaimer: DXS.ASX, VCX.ASX & NSR.ASX are currently held in the TAMIM Property Fund: Listed Property portfolio.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim