|

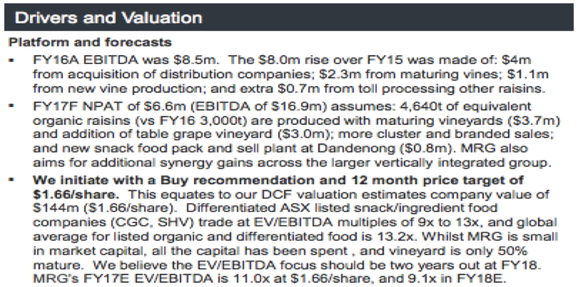

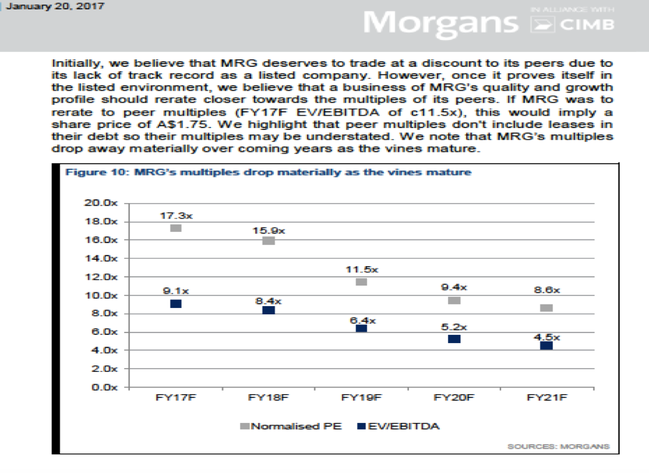

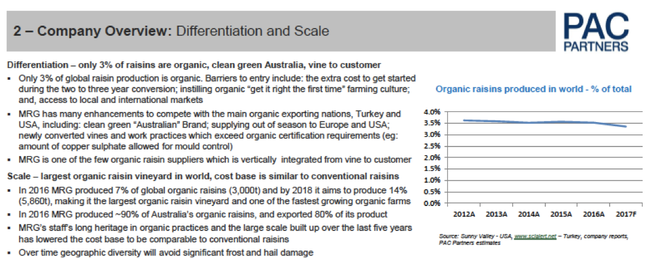

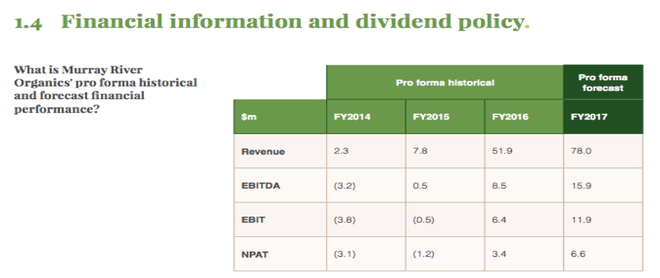

We made the mistake of investing in the Murray River Organics (ASX:MRG) IPO at $1.30. The stock has fallen by 73% to $0.35 in the company’s turbulent 6 month listed history, and we sold out at $0.65, 50% below the IPO price. Rather than sweeping this under the carpet we see this as an opportunity to learn some valuable lessons. In this article we share around some humble pie. Why we invested in MRG in the IPOa) Industry tailwinds The trend of growing demand for natural and organic foods has been well entrenched for many years, and we believe provides strong tailwinds for over the long term:  Source: PAC Partners b) Compelling relative valuation MRG’s prospectus forecasts suggested the company was listing at an EV/EBITDA of 11x versus the global average for listed organic and differential food stocks of 13.2x, and the multiples would drop off materially in the coming years as MRG’s vines mature:  Source: PAC Partners, Jan 2017  Source: Morgans, Jan 2017 c) Scarcity factor In addition to the industry tailwinds MRG appeared well positioned to take advantage of the current global under-supply of organic raisins:  Source: PAC Partners, Jan 2017 What happened next...1) IPO concluded successfully in December 2016 based on the FY17 prospectus forecast: $15.9m EBITDA, $6.6m NPAT:  Source: MRG prospectus 2) MRG’s H1 result – on track & re-affirmed prospectus forecasts. 3) First profit warning May 4th: new FY17 forecast $12.5-13.5m EBITDA, $4.2-4.9m NPAT: “The FY17 pro-forma revenue is expected to be down by $10 million, with approximately half of this reduction being attributed to the previously communicated 5-6 week delay in harvest season caused by an unusually cool and wet spring, coupled with more recent wet weather. The other half of the reduction is attributable to slower than anticipated uptake in sales following delays to the refurbishment of the Company’s Sunraysia processing facility, during which dried vine fruit could not be processed, as well as a lower contribution from Cluster sales following the previously communicated write-down of some Cluster inventory.” 4) Second profit warning May 22nd: new FY17 forecast $6.5-7.5m EBITDA, $0.1-0.8m EBITDA: “The reduction in sellable dried vine fruit from the 2016-2017 crop, due to the recent and previously announced cold and wet weather experienced in the Sunraysia region, has resulted in the Company revising its estimated FY17 pro forma EBITDA to be in the range of $6.5-7.5 million and pro forma FY17 NPAT in the range of $0.1-0.8 million.” What we got wronga) Management This is the most humbling mistake for us to own up to since we are so focused upon identifying management teams who are honest, competent, shareholder friendly and motivated. The great thing about investing is that everyone is faced with mistakes upon occasion, and thus has a choice how they deal with them – we can all chose to either learn a lesson or not to. The background to our experience with MRG’s management dates to the pre-IPO presentations when we saw them present. We thought the CEO came across as competent, honest and knowledge-able, and were of the opinion he would be a great leader for the business looking forward. We then met him again at a conference a few weeks after the IPO and were again impressed for the same reasons. We were reassured that everything was on track and the company’s prospectus forecasts would be achieved. This meeting was the week before the company announced its first major profit warning. Yes, you read that right. Management were presenting to investors the day before the profit warning with the message that everything was on track. This is why this job can be so humbling. We clearly misjudged management on all levels. We don’t want to dwell on the negatives about MRG’s management in this article but it is clear they didn’t tick any of the boxes we were aiming to tick. b) Our assessment of weather risk Weather risk will always be a key consideration when investing in an agricultural exposed company like MRG. We did indeed consider this risk in depth before investing. At the time we took comfort from management and broker reassurances that the prospectus forecasts already factored in short term risks including weather. This was a big mistake on our part as poor weather ended up being a primary contributor to MRG’s subsequent profit warnings which made it painfully clear that weather risk had not in fact been factored into the company’s prospectus forecasts. c) Our assessment of the company specific risks Beyond the challenging weather conditions, the company mentioned the refurbishment delays at the company’s Sunraysia processing facility as being a major problem since dried vine fruit could not be processed as a result. In addition, there was as a lower contribution from Cluster sales following the previously communicated write-down of some Cluster inventory. Both of these issues have had a significant impact on the company’s sales and earnings in MRG’s brief listed life, and we clearly under-estimated both of these risks. We both issues relate to our judgement of management as there was an underlying assumption that management were on top of these logistical issues ahead of listing. MRG certainly has revealed an unusually long list of problems to the market in its 6 months on the ASX. d) Investing in the IPO rather than awaiting some listed trading history Arguably most of our mistakes in this example would have been avoided if we had avoided buying MRG in the IPO and had awaited some listed trading history, preferably at least a few years. By watching the stock as a listed entity for a period we would have had a far clearer picture of the company’s key risks. e) Under-estimating the implications of the company’s unusually short escrow period This was an unusual one. MRG had a very short escrow period for pre-IPO shareholders which meant there was a massive increase in the supply of stock hitting the market at exactly the wrong time, into bad news. In hindsight we should have asked ourselves why the management team and brokers would support such a short escrow period. We are not suggesting that management were aware of all of impending problems when they wrote the prospectus but it does look as if there was pressure from some pre-IPO shareholders to create an exit point as soon as possible. This is the opposite of what we are normally aiming for; a long term and committed shareholder base. Lessons learnt:

Conclusion:Learning from your mistakes is one of the greatest opportunities all investors face. As a result, we wear our scars proudly and look to learn as much as possible from our mistakes. Investing in the MRG IPO was arguably our biggest mistake in the underlying portfolio’s 2 years and 2 month trading history. We won’t be making the same mistake again.

1 Comment

28/6/2017 10:59:02 am

Outstanding transparent review. The fact that TAMIM is prepared to lay all cards on the table in this way is refreshing to say the least, and should serve to give anyone confidence in your honest, ethical approach to business. Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim