|

With August at an end, eye-catching results reveal a fascinating story of the future ahead... Check out our 4 takeaways from reporting season below...

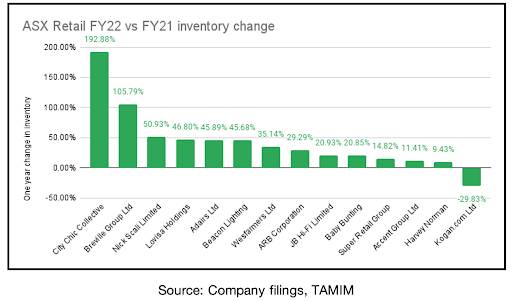

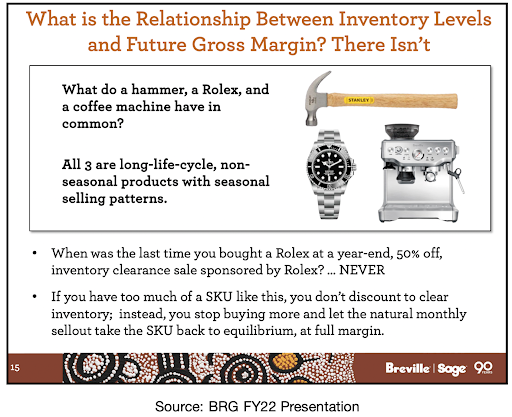

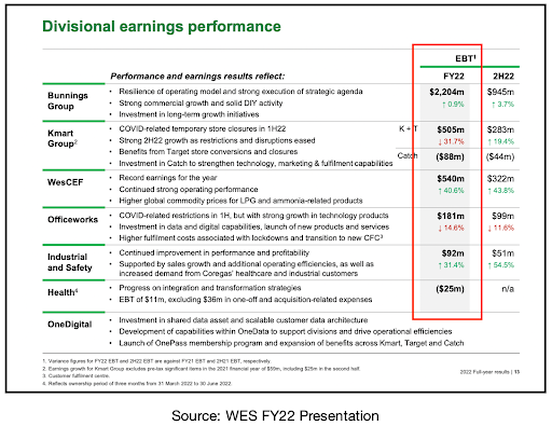

The annual August reporting season has come to a close, with the majority of companies either meeting or exceeding expectations. Here are four takeaways from the results and why we think they are relevant to investors. Also, if you haven't already, check out our thoughts on individual company results including BHP, Telstra, Coles and Pilbara Minerals. Higher for longerThe energy crisis engulfing nations has led to cosmic profits for Australian companies. According to data from the ABS, profits before tax from mining exceeded the combined earnings from all non-mining sectors by 65%. In normal times, non-mining profits average about double that of the mining sector. There looks to be little respite for businesses and households. Russia has ceased Nord Stream gas flows to Europe, which looks to be a cunning negotiating tactic to encourage a lifting of sanctions by the West. China is approaching a concerning number of cities under COVID-19 restrictions, in addition to damaging floods and the deflating of its property bubble. OPEC announced a marginal reduction in supply, responding to a 30% decline in oil prices. The usual cure to high prices is high prices. But supply is yet to kick in after years of low investment and likely won't at all in the case for fossil fuels like coal.  Whitehaven Coal CEO Paul Flynn summarised the current situation nicely: “Energy security is expected to remain a global priority, and it's likely to take many years for global supply-demand dynamics to re-balance. High-quality, high-CV [calorific value] thermal coal will be required through the multi-decade energy transition”. It's hard to see a bear case for energy over the near-term other than a severe global recession that curtails demand. Like all cyclical industries, prices will return to a more normalised level as new supply, either in the form of new projects or new types of energy, begin production. It's fraught with danger forecasting that cyclical highs will persist in commodities. But judging by the current status quo, it doesn't look to be abating anytime soon. Houston, we have an inventory problemComing into reporting season, all eyes were on how much inventory retailers had accumulated. Investors were broadly negative about the sector, given that spending will likely drop off from the pandemic-induced bump as interest rate hikes and inflation reduce customers’ purchasing power. A worst-case scenario would see a business purchase too much stock and subsequently be forced to discount it to free up cash. It was a mixed bag. Online plus-sized retailer City Chic nearly tripled its stock year on year. On the flip side, Kogan reduced inventory by 29%, albeit it had its own self-inflicted blowout 12 months ago. The median ASX retailer increased inventory by 32% on the prior year.  Interestingly, premium household appliance maker Breville spent seven slides of its investor presentation explaining why a doubling of its inventory was justified.  It compared the durability of its coffee machines to Stanley hammers and Rolex watches. Call us pessimists, but if you’re spending $2,799 to make a latte at home, you probably want the latest model, not something manufactured two years ago. Moreover, a 20-year-old Rolex will more likely than not appreciate in value. A used coffee machine usually ends up at your local Salvation Army. The key takeaway here is that it seems unlikely that all retailers will be able to clear the excess inventory without either some level of discounting or further cash flow problems. Remember, cash held up in stock cannot be used for other activities like paying wages or reinvesting in the business. Many retailers have run into trouble not for having an inferior product but for failing to manage working capital appropriately. More jobs than workersSpeaking to any hiring manager and they will tell you the war for talent is brutal. There are now more vacant positions than unemployed people in Australia, indicating a mismatch of skills. Dan Murphy’s this week went to the extreme action of offering on-the-spot interviews until Sunday to attract casual staff for Christmas. The situation is set to worsen. ANZ announced job advertisements increased 2.0% in August reaching their highest point since 2008. Coles CEO Steven Cain said, “We need more skilled and unskilled people to do all the jobs that need doing at the moment; otherwise it will drive further inflation.” He makes a pertinent point. Even if energy and food prices retract, inflation won’t go away until labour pressures are relieved. It’s not all negative though. As we discussed last week, certain companies will benefit from the labour shortage, including the current portfolio holding PeopleIn, which provides recruitment services for the healthcare, technology, finance and industrial sectors. The conglomerate is not deadConglomerates have been out of favour with investors for some years now. It’s considered an opaque organisational structure, usually supported by one stellar division bunched together with a collection of other mostly average segments. Reporting leaves a lot to be desired, meaning investors and the market fail to understand the company leading what’s termed a “conglomerate discount”: when the value of the total company is less than the sum of each individual division if it were a stand-alone listed business. Subsequently, investors have forced conglomerates to divest under-performing or non-core interests. General Electric — the world’s biggest company as recently as 2009, is now splitting itself in three after dwindling returns. Locally, the most recognised conglomerate is Wesfarmers with operations spanning retailing, health, mining, chemical and industrial processes.  Despite earnings falling by 2.9%, Wesfarmers marginally increased its dividend in FY22. However, the underlying divisions performed with far more volatility. Kmart Group profits plunged 39.7% while earnings at Officeworks fell by 14.6%. Fortunately, this was offset by strong results in its chemicals and industrial divisions, with profits up 40.6% and 31.4% respectively. Herein lies the big benefit of conglomerates, it shields the company from annual performance fluctuations. Imagine the market reaction if Kmart was a standalone retailer with profits down two-fifths. By remaining part of a bigger entity, earnings fluctuations are smoothed out; therefore, dividends are more reliable and consistent. BHP, Nine Entertainment, Seven West Media and News Corp are other examples of domestic conglomerates that have outperformed the market since 2020. Yes, the risks mentioned above remain for all five companies. But when run efficiently, conglomerates can be an effective structure in times of volatility.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim