|

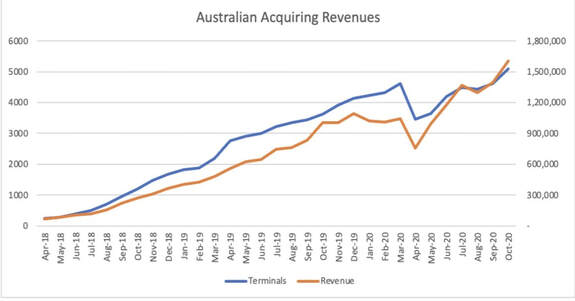

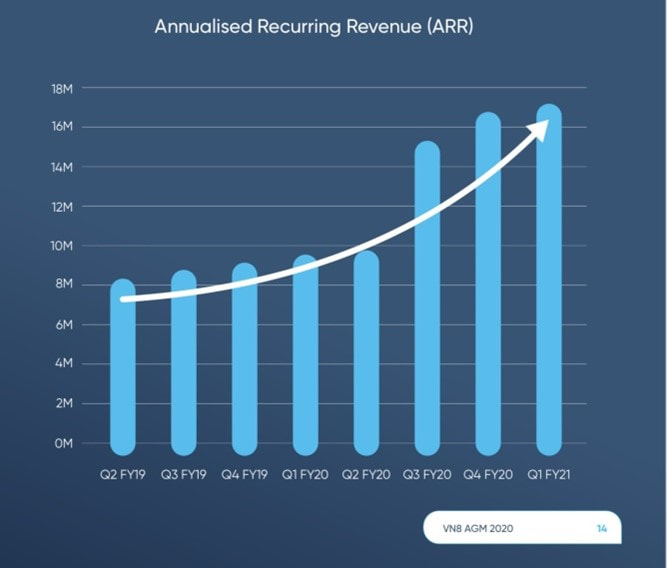

Coming to the end of 2020, Ron Shamgar provides an update on a number of the companies held in TAMIM's Australian equities portfolios. After a strong 2019, this year had been shaping up to be another good year until the pandemic hit Australian shores. The companies below are amongst the holdings that have helped the portfolio deliver a strong year despite the challenges in the stock market. Smartpay (SMP.ASX) reported its 1H FY21 results during November. The period of March to September coincided perfectly with the Covid lockdowns and downturn and yet the company managed to deliver an 8% increase in revenues, to $14.5m, and just a 6% decrease in EBITDA, to $3.6m.  Source: SMP company filings Source: SMP company filings More importantly, the Australian division is growing strong and was up 67% to $6.3m but, at the end of October, is currently annualising over $19m in revenues. The SMP thesis is all about the high growth Aussie business, with 5,000 terminals which we believe can double in a year. That alone, we believe, will drive good profit growth and we value SMP at about $1.00.  Evolve Education (EVO.ASX) reported its last September half year end result in November as it moves to a calendar year end from next year. 1H EBITDA was $12.3m and in line with guidance. EVO also announced a $35m debt refinance which provides for $20m of acquisition capacity in Australia, which could add $4-5m of EBITDA. The NZ centers are seeing good occupancy rates and the cost out program is ahead of budget. We estimate $23m EBITDA in CY21 and further acquisition of childcare centers in Australia. We value the company at 23 cents. Vonex (VN8.ASX) is a small but growing telco provider targeting small businesses with in-house developed phone system solutions. The company has finally turned profitable and, with the recent acquisition of 2SG, has expanded its wholesale network of resellers to sell its Optus mobile and wireless solutions and other telco software products.

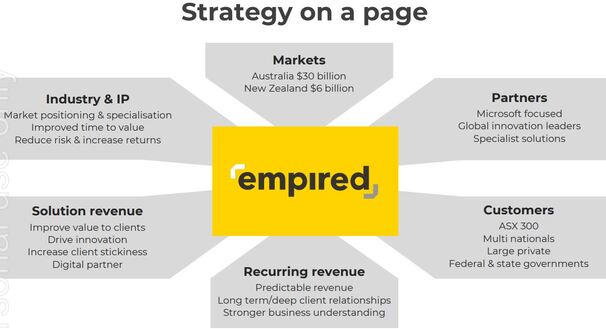

Source: VN8 company filings We took a position in VN8 at 11 cents a year or so ago and we believe the company can grow both organically and acquisitively with the recent addition of an experienced M&A executive from another listed telco. Management has indicated that the sub-$10m revenue telco segment is ripe for consolidation as larger listed peers are looking for bigger deals. We value VN8 at 30 cents and are already up approximately 150% since our initial investment. Resimac (RMC.ASX), a top three holding, reported a 1H profit update significantly ahead of market expectations but in line with what we have been predicting all year long. 1H NPAT is now on track to be up 100% to $48-$53m. The result reflects AUM growth to $12.7bn at the end of October, continued low cost of funding and disciplined cost control. We estimate that RMC will report $90-$100m NPAT this year, a significant profit milestone that not many ASX listed companies ever achieve. This places RMC on a PE of just 8x. With a similar business coming to market soon in Liberty Financial, we believe investors will continue to rerate the stock to the same multiple as its peers while RMC is growing faster than other listed companies. We value RMC at $3.00. Empired (EPD.ASX) provided a strong update at its November AGM and is now expecting $89m 1H revenue, $16.5m 1H EBITDA ($4.8m of JobKeeper included) and operating cash flow conversion of 90%+. This should see EPD with a positive net cash balance by Christmas, which has allowed management to declare dividends from February next year.  Source: EPD company filings With a stronger balance sheet and good momentum we expect more large contracts to be announced in the next few months with acquisitions to resume next year. We value EPD at 90 cents. Additionally, with the sector consolidating recently, we believe EPD may end up in the crosshairs of an international suitor in the near future. Probiotec (PBP.ASX) is a contract manufacturer and packing business to the vitamin, pharmaceutical and, more recently, food and beverage industries. PBP announced the acquisition of Multipack LJM for $52m in November. LJM will add $70m of revenues and makes PBP one of the larger packing and pharmaceutical contract manufacturers in Australia.  Source: PBP company filings From FY22 we estimate the combined group will generate $190m of revenues, $33m of EBITDA and $19m NPAT. The acquisition is 40% EPS accretive as management has utilised debt and script. PBP is currently trading on FY22 PE of 10x and a dividend yield of 2.8% while offering good growth and further M&A upside. We believe the stock is worth about $3.50. Disclaimer: All stocks highlighted in this article are held in TAMIM portfolios.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim