|

Ron Shamgar provides an update on a selection of stocks that feature in the TAMIM Australian equity portfolios. Some old favourites, some enticing newer positions. Read on to find out more.  Author: Ron Shamgar Author: Ron Shamgar EML Payments (EML.ASX) EML provided a trading update in May, which was received well by the market with the shares appreciating 30% in the ensuing three weeks. The highlights were:

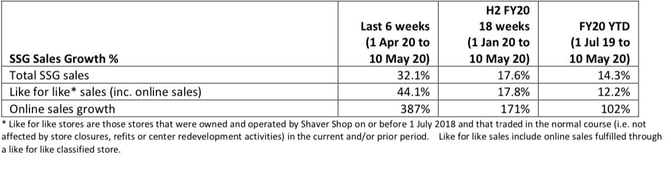

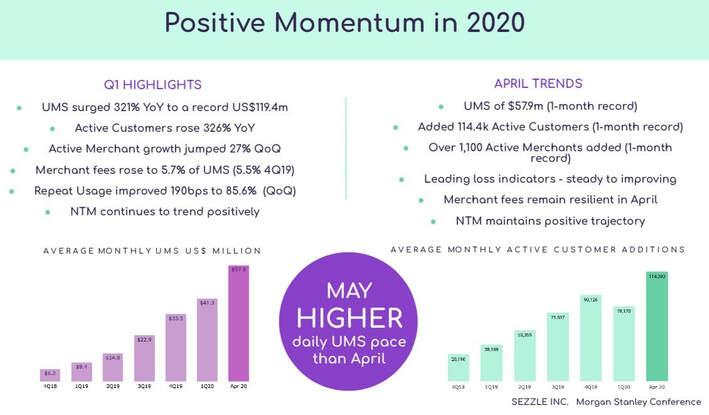

There is no doubt that Covid-19 has benefited EML by bringing forward client intentions to transform their digital payment strategies.  Source: EML The only drag on EML for now is their mall gift card division which was down 53% in April but saw a material improvement in May as shopping centers across Europe began to reopen. We expect gradual month on month improvement as more malls across North America resume operations. The largest risk to EML is another round of lockdowns. With EML trading at over $4.00, the stock is at about fair value on a twelve-month outlook. On a longer term 2-3 year view we still believe EML is cheap and can, assuming they execute, double over that period as more new programs are launched and further acquisitions are taken by a management team that has proven to be sensible and savvy during uncertain times. EML is owned in the TAMIM Australia All Cap portfolio. Shaver Shop (SSG.ASX) Shaver Shop provided a strong sales update in May with record sales growth during the worst economic downturn in Australia’s history. The performance was led by online sales growth as consumer’s preference for online shopping took off during the lockdown period.  Source: SSG company filings During the six weeks between April 1 and May 10 online sales increased 387% with total sales increasing 32% and 2H YTD sales up 17.6%. These sales results should lead SSG to report record profits this year and we forecast a strong net cash position to finish the year. Pleasingly, this sales growth was driven by many new customers and an emerging female customer base that are finally embracing the SSG product offering for themselves. We value SSG at around the 80 cents mark. SSG is owned in both the TAMIM Australia All Cap and Small Cap Income portfolios. Sezzle (SZL.ASX) Sezzle is a new position we initiated in May at around $2.00 a share. SZL is one of the leading (top three) Buy Now Pay Later (BNPL) companies that is benefiting from fast growth in the North American market. The business is led by a conservative and innovative management team and SZL, unlike some of its other peers in the sector, is a pure play on the largest and most lucrative BNPL opportunity: the US market. As of the end of April, SZL boasts annualised total transactions value (TTV) of $1.1bn, 1.25m customers, 14,000 merchants with all metrics seeing acceleration. Compared to market leading Afterpay (APT.ASX), SZL is generating similar revenues per customer and yet the market is willing to value APT customers at 4x more than SZL. On all other metrics, such as EV/Revenue and Market Cap/TTV, SZL appears to be undervalued by a factor of 3-4x when compared to APT.  Although we do believe APT deserves a premium due to its larger scale and track record, we believe the valuation gap will close over time. Furthermore, in June (forgive us for dipping outside of the month of May), Zip Money (Z1P.ASX) acquired SZL’s competitor in the US, Quadpay, for $400m. Following the deal being announced, Z1P saw its now combined market valuation increase by a whopping $1.6bn. SZL and Quadpay share similar metrics, which in our mind highlights even more how undervalued SZL is. We value SZL at about $4.00. SZL is owned in the TAMIM Australia All Cap portfolio. Vita Group (VTG.ASX) VTG reported an update that Telstra stores have remained open but have seen lower foot traffic and supply chain disruption, resulting in lower revenues. Business demand has remained relatively steady as customers transitioned to work-from-home arrangements. VTG’s clinics commenced re-opening and have a strong pipeline of pent-up demand. Cash flow has been tightly controlled, with all capex projects not underway being deferred until conditions improve. VTG’s financial position is strong and management does not anticipate any requirements for new equity or debt financing. Whilst there will be some negative earnings impact from COVID19 in the short term, we believe the longer term impact on the business is likely to be minimal. Prior to Covid-19, VTG was on track to report 15 cents EPS and pay a 10 cent fully franked dividend. We believe this earnings profile will now be delivered in FY21. At the current price of $1.10 the upside for next couple of years is substantial. VTG is owned in both the TAMIM Australia All Cap and Small Cap Income portfolios. National Tyre & Wheel (NTD.ASX) NTD is a tyre and wheel wholesaler in Australia, New Zealand, and South Africa. The group has exclusive rights to import and distribute Cooper and Mickey Thompson branded passenger, SUV and light truck tyres. We took a position in the company in May as we anticipate tyre demand to increase as car usage becomes a preferred method of transport. In addition to people being increasingly wary of being confined in close quarters with strangers, public transport while enforcing social distancing is simply not equipped to handle a full-scale return to work. NSW’s "No dot, no spot" system, for example, has reduced capacity drastically.  Source: NTD company filings We are attracted to NTD’s undemanding valuation with a net cash position, asset backing of 48 cents per share (compared to the current share price of 35 cents), forecast cash EPS of 5 cents (PE multiple of 7x) and an estimated dividend yield of 10% grossed up for franking credits. During May NTD reported better than expected trading conditions with EBITDA guidance of $9m, net cash of $6m and a reinstatement of their dividend policy. We expect NTD to capitalise on the current environment and look to acquire other tyre distributors to add scale and volume in the lower price point of the market. We value the company at about 50 cents. NTD is owned in the TAMIM Small Cap Income portfolio.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim