|

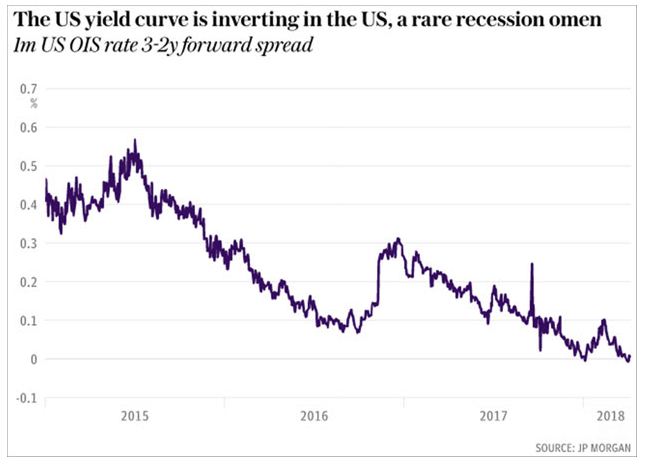

This week TAMIM Joint Managing Director Darren Katz takes a look at what to expect in the coming quarter. Given the firms investment view he points out a number of key investment thematics to keep an eye on while also digging into asset allocation. The first quarter of 2018 is over and we all survived it, just about. We see the world at an economic inflection point. From an economic perspective the developed market and probably more specifically the US with a real GDP of 2.6% looks strong. US economic growth has been driven largely by US consumption which comprises 69.1% of the GDP figure. As can be seen in the chart below, the US economy has continued to strengthen from its 2008 lows. Housing starts, a key indicator of economic strength, are now at an annualised rate of 1,236 (thousands) which is just below its 20 year average of 1300.  Source: JP Morgan We are seeing similar optimistic signs in Europe as demonstrated by the chart below showing Eurozone unemployment with a rate at 8.6% as of January 2018. This is a level not seen since the GFC in 2008. Asia continues to deliver growth to the world through its Chinese engine however political risks are heightening through changes to their internal structures which abolish the 5 year term limit on the Presidential and vice Presidential positions. This will allow President Xi Jinping to rule for as long as he wishes (for a good description on how China is ruled see this article) .  Source: JP Morgan Through the March quarter we have had 3 significant shocks to the global economic system. Volatility There has been a significant spike in volatility with the Vix having broken out of its unnaturally low range of 9 to 12% moving to over 35% in February on the release of US wage data that the market perceived to be higher than expected. The view on this was that there could be a strong response from the Fed in relation to increasing interest rates. On the last 10 occasions the Vix has spiked above 35% since 1990 the median return 6 months post the volatility spike of the S&P 500 was +9.1% and +16.8% after 12 months. While we are not suggesting this time will be the same, it is important to figure out if the spike was caused by an external shock to the system or a genuine recessionary problem with the economy. While headline CPI in the US has certainly moved back towards 20 year averages, core CPI has remained fairly stable and even tended lower across the last 5 years.  Source: JP Morgan Trade Wars Donald Trump has been taking on the Chinese in what we believe is a bid to strengthen protection over US business intellectual property rights when dealing with China as discussed in our recent article (here). Unless you are Mexico or Canada, the impact of US tariffs and Trump’s rhetoric, if they are actually applied given that many countries are actually exempt, is fairly low as can be seen in the below chart showing the impact of exports to the US as a share of GDP.  Source: JP Morgan Trump and the Tech Impact: The impact of Trump’s attacks on Amazon have been been strongly felt with the share price of Amazon down over 10% since mid-March. Facebook (share price down in excess of 10% since February) faces its own woes going forward and it remains to be seen whether the US congress will seek to implement stronger regulatory oversight on the company and its control over data. A significant proportion of the rise in US equity markets over the past 12 months have come from the FAANG’s. The share price of Netflix as an example is up over a 100%. This means that heading into the remainder of 2018 we should be looking to different market segments for return generation. We have been positioned towards more defensive value focused equity investments globally with key thematics remaining infrastructure, defense spending and good value technology business away from the FAANG’s. Equities  Source: JP Morgan Over the second half of 2017 and the first quarter of 2018 we have seen prices of Australia's key resources decline substantially. As mentioned previously this is a key driver for the AUD USD exchange rate. Weaker commodity prices in particular iron ore prices tend to result in a weaker AUD. While it may be unusual for us to start our equity discussion on resources and currency’s the exchange rate has a significant impact on your investments which are located outside of Australia. The weaker AUD has seen most global equity markets generate strong returns in Australian dollar terms however when we look at each market in local currency terms the picture is not quite as rosy.  Source: Financial Times The first quarter of the year saw Japan down strongly by 4.7% while US equities were down 0.8% in local currency terms. One could almost be excused for asking what all the newspaper headlines were about in February given the US equity market return. This hides the fact that markets had a significant and sharp move upwards in January and a significant reversal and then recovery in February. In Australia the ASX 200 was down -3.9% while the Small Ords was not as bad at -2.8%. Weakness in the Australian Equity market was broadly spread with banks, energy and materials all down. Tech and healthcare were left to fly the flag for positive returns. Forward PE’s are slightly elevated at 14.9x versus the historical 15 year average at 13.9x in Australia. In the US, forward PE’s on the S&P 500 are at 16.4x versus their historical 20 year average of 15.8x and the current bull market which started in March of 2009 has seen a 290% return over 108 months. It is pleasing to see that corporate earnings trends across Australia, the US and Europe are all trending positive with synchronised global growth a reality. Japan continues to trade significantly below its 20 year forward PE average and therefore continues to look attractive from a valuation perspective.  Source: JP Morgan Fixed Income As global central banks in developed economies start to or continue to slowly raise interest rates, we favour refraining from being invested in both government and corporate bonds. There will be a time in the cycle to return to these investments but this is not it. We are seeing the US yield curve flatten to levels not seen prior to the GFC in 2008, this is a result of the long rates reducing and the front end of the curve going up.  Source: JP Morgan In Australia we have seen a similar flattening of our yield curve over the last 12 months. At TAMIM we continue to favour gaining exposure to the diversification benefits of fixed income through the purchase of high yielding loan portfolios. We have moved away from exposure to consumer loan portfolios unless the platform providers are offering first loss provisions towards the relative safety of secured and senior debt within the business sector. Property Within Australia we still continue to see property yields compress as Australian interest rates remain low and banks seem to have regained their appetite for lending against property. We are finding high quality assets very hard to come by but are encouraged by some interesting opportunities we are seeing in the retail segment specifically focused on neighbourhood shopping centers. Conclusion We are safely able to predict the return of volatility in 2018 as volatility has already returned to the equity market, triggered by concerns about inflation and trade protectionism. At Tamim we continue to state our insistence that portfolios need to remain well-diversified. The solid global growth environment continues to underpin our constructive view of risk assets, including equities, corporate credit and targeted segments of the property market. Inflation, protectionism and politics are risks worth monitoring, but we believe they are unlikely to have a sustained market impact this year. Adopting a defensive strategy would be premature. Cash is certainly not king as a $100,000 investment in a term deposit is only yielding just north of a $2,000 annual return. Looking at the chart below we are reminded that a balanced and diversified portfolio across both bonds and equities over a 5 year time horizon would have delivered you a return range of between 1 to 21% thereby eliminating the downside risk of capital loss considerably.  Source: JP Morgan

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

May 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim