|

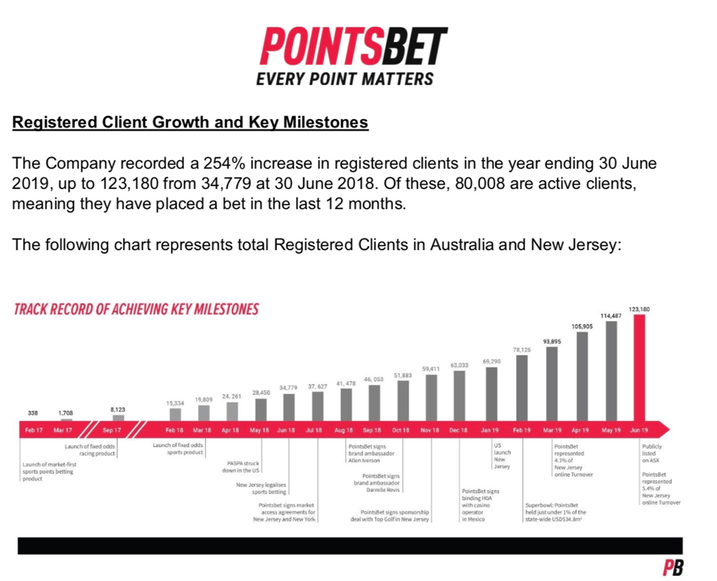

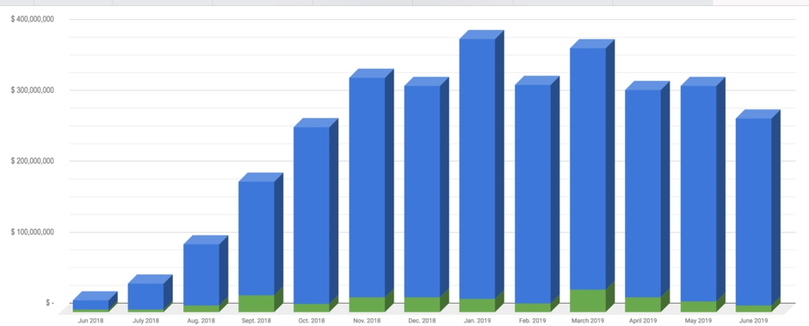

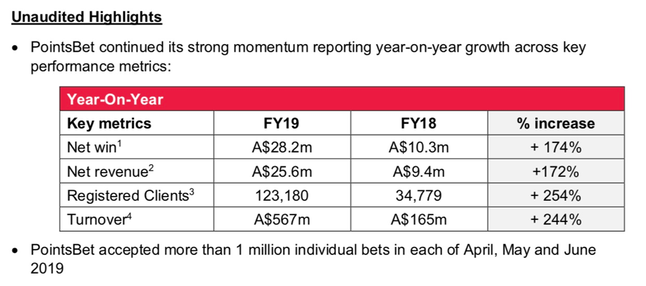

This week we revisit PointsBet (PBH.ASX), one of our holdings in the TAMIM All Cap IMA portfolios. We spotlighted PBH a little over two months ago following their IPO. The stock is up 50% since then. In this article, we will try and place a valuation on PBH and in doing so we also make some comparisons to market darling Afterpay (APT.ASX). If you find that unusual, then you should read on. When we first wrote about PBH (see here) we detailed our investment thesis and why we think the business presents Australian investors with a possible “once in a lifetime” opportunity to capitalise on a huge market opportunity that is fast emerging in the US sports betting market. PointsBet has seen substantial progress since IPO. The company announced a deal with Penn National Gaming - $3bn and NASDAQ listed - for market access to a further five US states including Ohio, Indiana, West Virginia, Missouri and Louisiana. All together now, PBH has access to a total of ten US states with a population of 81M people!  Source: PointsBet company filings In New Jersey (NJ), where PBH has been operating since January 2019, the company has taken 5.4% market share in a very short time. Based on market estimates and a monthly betting turnover in NJ of $450m (AUD) per month and growing, we estimate PBH is currently annualising over $250m of bets. This is after only six months of operations and in the first full year since sports betting was legalised in the one state – pretty amazing if you ask us! Monthly turnover in New Jersey since Sports Betting bill introduced 12 months ago. All figures in USD.  We estimate that by 2023 the majority of US states will have legislated sports betting bills. Since there are only a limited number of licenses available in each state for operators to access on long term deals, these licenses are extremely valuable and strategic assets that are not currently showing their true future value on the balance sheet. The market opportunity for sports betting in the US is estimated at between $200bn - $300bn a year at full roll out in all states. If PBH’s success in such a short period in NJ is any indicator, it is possible that in five years from now, for PBH to be handling between $5bn - $7.5bn in bets annually. Sports betting book makers usually make an average of 5% net revenue margin on total bets. PBH, in the above scenario, could make an average of $300m in revenues. So, how do we value such a business? Although there are a wide range of possible outcomes, we can make some assumptions to gauge a possible valuation. If we look at global gaming companies, and there are many, the average earnings margin can be anything from 20% up to 40%. If we stay conservative and take the lower value and apply it to PBH’s future revenue estimates above, we get an EBITDA of $60m at the midpoint. Applying a 20x multiple (reasonable for such a high growth business), and we get a possible valuation for PBH in excess of a billion dollars or approximately $10.00 a share. That is 3.5x higher than today. Another way of looking at PBH is to compare it to market darling Afterpay (APT.ASX). At first glance, comparing an instalment payments provider to an online sports betting bookmaker, seems odd but, in our mind, both businesses share some similarities that may deserve closer valuation multiples. The APT business model is based on the network effect. This is where the more retailers that sign up to the solution, the more customers that want to use it and vice versa. Arguably, each retailer will only offer a limited number of instalment solutions at the checkout. Hence this market structure is similar to PBH where there are only a limited number of sports betting licenses for each US state. This means both companies enjoy a first mover’s advantage. The revenue model of both companies relies on clipping a certain margin of total transactional value. APT’s average margin is approximately 4% of total sales financed but, after bad debts are deducted, net revenue margins are about 2% and could possibly decline over time. In comparison, PBH also makes a net revenue margin on total bets made on their platform. The historical net revenue margin for all book makers in Nevada has averaged 5% historically (2.5x APT’s margin). This is in line with PBH’s current margin.  Source: PointsBet FY19 results Although APT began its journey in Australia, the majority of the current valuation is based on its initial success in the US market and the prospect of that success continuing into the future. Similarly, PBH began in Australia but their future is predicated on success in the US. Both companies arguably have similar market size opportunities in the US in the hundreds of billions of dollars of turnover. Back in 2017 APT was turning over very similar figures to PBH and was trading at a market valuation of $750m.  Source: Afterpay FY17 results Currently APT has 4.6m customers generating $4bn of transactions. Average spend per customer is $900 pa. PBH has 120,000 customers and currently total betting turnover at circa $600m. Average bet per customer is $5,000 pa. The market cap of APT is about $6bn and forecast revenues this year are $215m. By comparison, PBH’s market cap is just under $350m and is making $28m in revenues this year. Both companies are currently loss making and well-funded for growth. If we apply some of our forward estimates on PBH’s future revenue, take into account the large market opportunity, and strategic value of each market access sports betting license, it is feasible that PBH in future may gain something like the valuation APT is currently enjoying. Some food for thought. Enjoy the weekend.

1 Comment

Ruth Alvarado

26/8/2019 12:52:39 pm

I do not understand what all the fuss is about Afterpay, their business model has been used in South American countries for many many years. These days you can pay in instalments even your utilities bills. I think Afterpay as a company and share prices are overvalued. Just my humble opinion!!! Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim