|

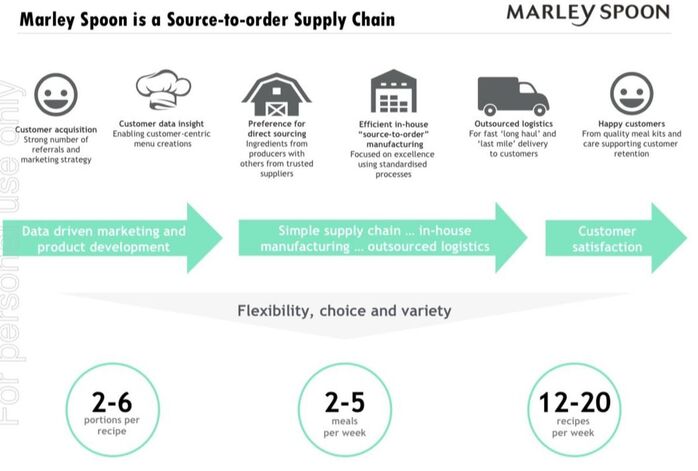

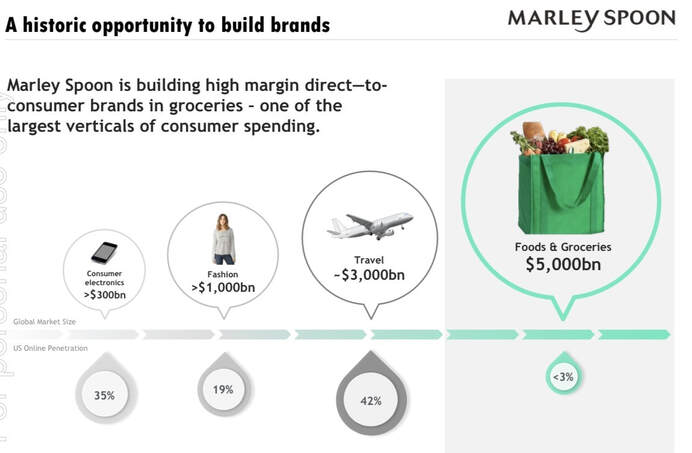

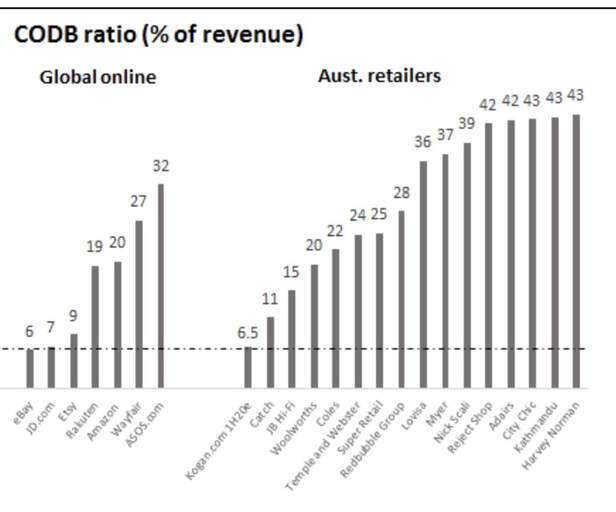

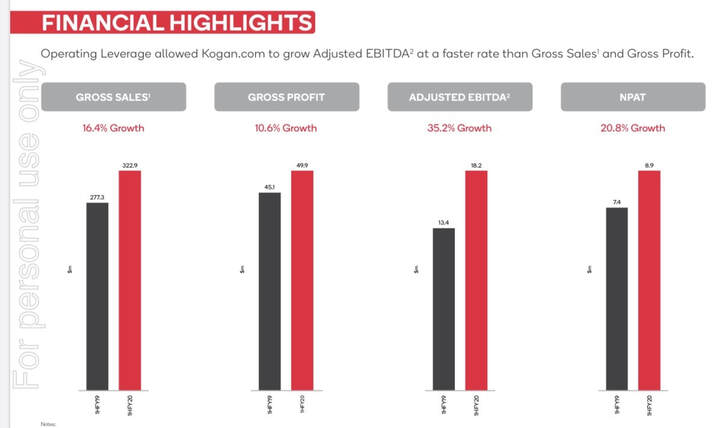

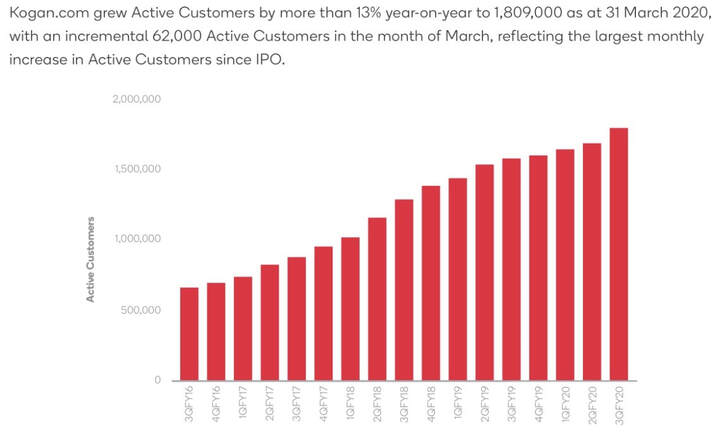

As we venture further into the evolving Covid-19 situation, we are searching for companies that are benefiting from current conditions. This week we discuss two such companies that are seeing robust and unprecedented trading conditions. Find out which stocks below. Marley Spoon (MMM.ASX) is a global subscription-based meal kit delivery business. Founded in 2014, the company operates across Australia, the US and Europe. The business allows for consumers to choose between two brands online, Marley Spoon and Dinnerly, that offer a selection of easy to cook dishes across a diverse menu set.  In a nutshell, consumers can go online and choose their meals, for as little as $10 a portion, and receive a box full of ingredients ready to cook weekly. In 2019, MMM had over 180,000 customers, delivered 22m meals globally and generated $200m in revenues.  Source: MMM company filings Consumers tend to cook at home three to five times a week and MMM solves some of the biggest issues of cooking at home. MMM combines the convenience of a regular home delivery, little wastage (as only the exact amount of ingredients are delivered), and easy to follow cooking instructions. Perfect for the time-poor professional of today. Over 91% of customers continue to use the service after only six orders. The food and grocery market is worth $5tn globally, yet only 3% is transacted online. MMM has ample runway to continue growing.  Source: MMM company filings Historically, MMM had a high amount of customer churn and marketing spend. The Covid-19 situation has seen a huge surge in customer demand as, with people now staying at home more than ever, the delivery aspect is even more appealing. The service is seen as a safer and more convenient way to shop for groceries. With the onset of the crisis, through Q1 2020, MMM has already seen revenue growth of 40%. We expect the current quarter to see a significantly higher, if not similar, growth rate compared to Q1 (we are estimating closer to 60%). In fact, based on our discussions with management, we expect marketing spend to drop materially as the company cannot keep up with new customer signups. This should lead to the group turning profitable this year. We are forecasting at least $350m of revenues and $25m of EBITDA. Based on its largest competitor (Hellofresh) and our forward estimates, we value MMM at $1.65. Kogan (KGN.ASX) is a leading online consumer electronics retailer and marketplace. KGN has built a strong brand over the years with the entrepreneurial and charismatic founder, Ruslan Kogan, as a major shareholder. With a 1.8m person customer base, KGN has, over the years, also built a services marketing division under its own brand, selling anything from mobile and electricity plans to insurance cover.  Unlike most e-commerce businesses, KGN is highly profitable, has the lowest cost of doing business industry-wide (less than 7%), and positive net cash on the balance sheet ($20m net cash). In 1H FY20, KGN delivered $320m of sales and $18m of EBITDA. In addition, KGN pays a 2.5% fully franked dividend yield. We expect FY20 EBITDA of $35-$40m.  In the current Covid-19 situation, KGN is seeing record growth in sales and customer numbers. This is driven by higher demand for home office equipment (some TAMIM staff are included in the new customers here) as working from home is more prevalent, consumers shopping online while spending more time at home, and the search for cost savings on utility services and the like.  We expect the current trend to only accelerate and continue for the remainder of the year. Atlassian employees, for example, have been told they are working from home until at least June and have been given a $500+ allowance just to buy office equipment. That is just one example of a company facilitating this, there will be countless white-collar workers buying equipment personally too. In Q3 FY20, KGN has already reported 30% sales growth with March alone seeing 50% growth. Customer numbers hit a record 1.8m, with the company reporting its strongest monthly uplift in active customers during March.  In our mind, Covid-19 is likely to accelerate growth trends with a structural shift to the online space. Thus, as an online focussed player (unlike JB-Hifi etc.), we see KGN as disruptive and a clear winner. Most retail peers are currently experiencing store closures, laying off staff and suffering financial pressure - while KGN is hiring and awarding staff $500 bonuses.

In this crisis, KGN is doing what savvy businesses do. Utilising a once-in-a-lifetime opportunity to reinvest heavily into further discounted marketing so as to continue scaling its brand and the business in general. KGN is currently trading on approximately 12x EV/EBITDA for FY21. We value $KGN at about $8.00. The TAMIM Fund: Australia All Cap portfolio holds both MMM and KGN.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim