|

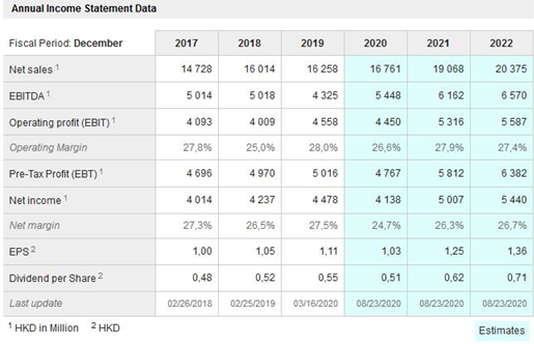

Kevin Smith highlights one of the stocks in the Asia Small Companies portfolio, one of the world's leading integrated glass manufacturers with a stock price that is up 71% over the last 12 months. Xinyi Glass Holdings Limited (XYG) was founded in 1988, is headquartered in Hong Kong and listed on the main board of the Hong Kong Stock Exchange in 2005. As one of the world's leading integrated glass manufacturers, Xinyi Glass manufactures high-quality float glass, automobile glass and energy-saving architectural glass. XYG has a sales network covering 140 countries with nine manufacturing bases in China's most active economy zones: Pearl River Delta, Yangtze River Delta, Bohai Economic Rim, Chengdu-Chongqing Economic Zone and Beibu Gulf Economic Zone. XYG, with a market capitalisation of over HK$ 36 billion and an annual revenue of over HK$ 16 billion, now has a total industrial area of over 6.89 million square metres and 12,912 employees. Accounting, Strategy and Governance Comments Accounting The XYG accounts are audited by Pricewaterhouse Coopers in Hong Kong and have been assessed as “true and fair” with respect to the requirements of the Hong Kong Financial Reporting Standards and the disclosure requirements of the Hong Kong Companies Ordinance. The most recent audit made note of the carried over amount of trade receivables of HKD 1,451,494,000 and the provision of HKD 41,481,000. The auditor concluded that the “judgements made by management in respect of the provision for loss allowance assessment on trade receivables to be supportable by available evidence.” XYG has a relatively low tax rate, 15.4% in the most recent interim results. This tax rate is sustainable as a result of qualification as a high tech enterprise in China which has a long-term tax rate of 15%. Key Data for Xinyi Glass  Source: Market Screener Strategy By volume 77% of XYG’s sales go to the property sector accounting for 49% of revenue, while 11% of volume and 28% of revenue is derived from the automotive sector. Demand from the property and automotive sectors are of great importance to the prospects for XYG, both sectors are recovering from the disruption caused by the Covid-19 pandemic. The float glass industry has recovered from the Covid-19 lockdowns and prices have recovered to the 2019 levels helping to deplete high inventory levels. Given the limited supply situation, prices have scope to continue rising through the next two years. Capacity for float glass is expected to fall 1% in the current year and remain below the 2019 peak during 2021 and 2022. XYG has scope to increase capacity by 15% in 2021 and 7% in 2022 which will boost domestic market share from 10% to 12%. One of the keys to increasing domestic market share in China is XYG’s first international manufacturing plant that will come on stream in early 2021 in Malacca, Malaysia. The Malacca plant will feed product into international markets allowing more of the domestic production in China to stay in the home market. We expect industry margins will improve as the costs of energy (44% of costs) and raw materials (37% of costs) have fallen. The price of natural gas, one of the major energy sources for glass furnaces, has dropped by 5% in 2020. Meanwhile, soda ash is the most expensive raw material used in glass manufacturing and has fallen 25% in the current year. We expect the pricing of key raw materials and energy to remain weak to stable in the next year. XYG is taking stronger control of the supply of raw materials with a new silica sand mine due to come into production by the year end. This mine is a first for XYG and the company expects to improve the stability of supply, costs and quality of raw materials into their manufacturing process. Governance XYG operates in full compliance with the corporate governance code in Hong Kong and the requirements of Appendix 14 of the listing rules. The Board comprises 13 Directors of which 5 are independent non-executive Directors and a further 4 are non-executive Directors. All Directors serve a fixed term of three years. The company published an ESG Report in July 2020. The CEO and Chairman have been active in buying shares in the market during 2020, buying 3.378m and 8.116m shares respectively after the release of interim and annual results. The company also bought back 6.22 million shares in January 2020. XYG has maintained a dividend payout ratio at around 50% in the past two years, up from 26.5% five years ago. Looking forward, the company is likely to maintain the 50% payout ratio which provides a good balance between the investment requirements of the business and returns to shareholders. Value, Momentum and Quality Comments XYG scores extremely well on our measures of value, momentum and quality. XYG has a ranking in the top 1% of all companies in the region in our analysis. There are 20 industry analysts providing coverage of the company. Following an initial decline in forecasts in the early part of 2020, subsequent forecasts for profits and revenues have resumed a rising trend. XYG trades on a forward price earnings ratio of less than 10x and a yield in excess of 5%. Given our view of the strategy for XYG that will see rising production levels, higher selling prices and lower to stable production costs, we expect the trend for rising earnings forecasts to accelerate through the balance of 2020 and 2021. Kevin Smith, also of Delft Partners, is portfolio manager of the TAMIM Asia Small Companies portfolio. Click here to learn more.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim