|

This week we present a piece by Hamish Carlisle, from Merlon Capital Partners who power the TAMIM Australian Equity Income IMA, re-examining Telstra. Note: this article was originally penned on August 17, 2018. We provided some detailed thoughts on Telstra about one year ago. Over the last year we note the following developments: Telstra has under performed the broader market;

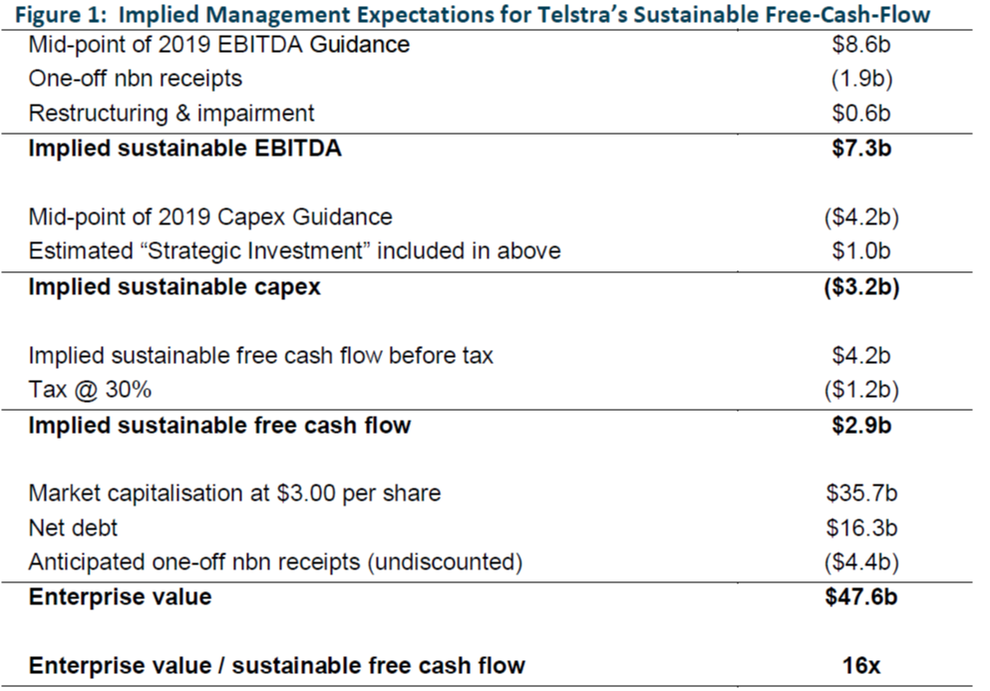

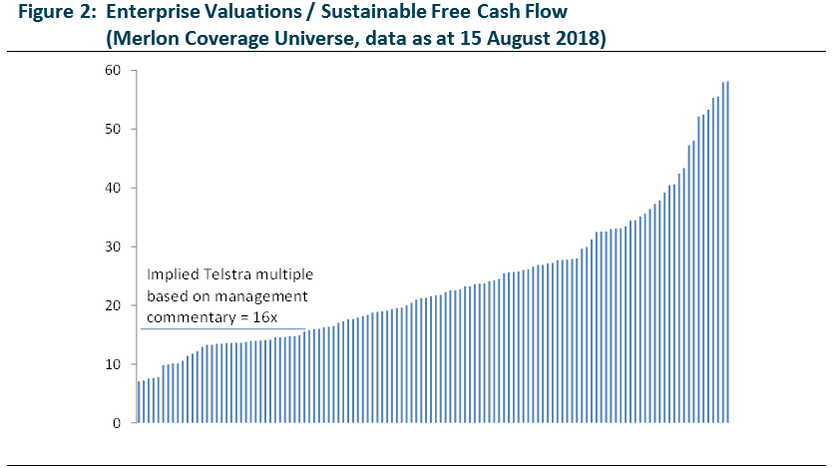

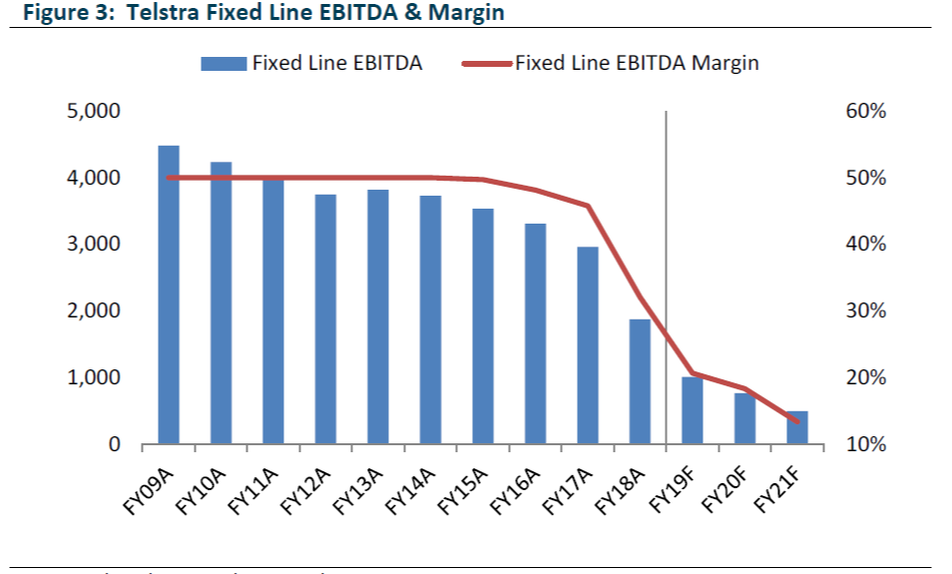

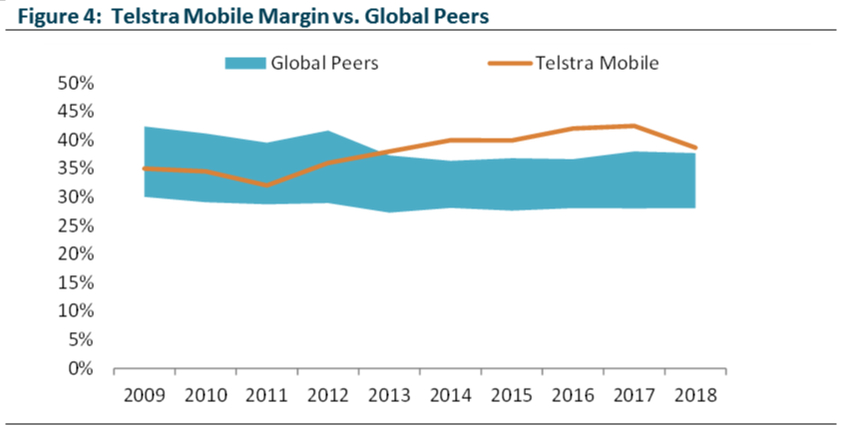

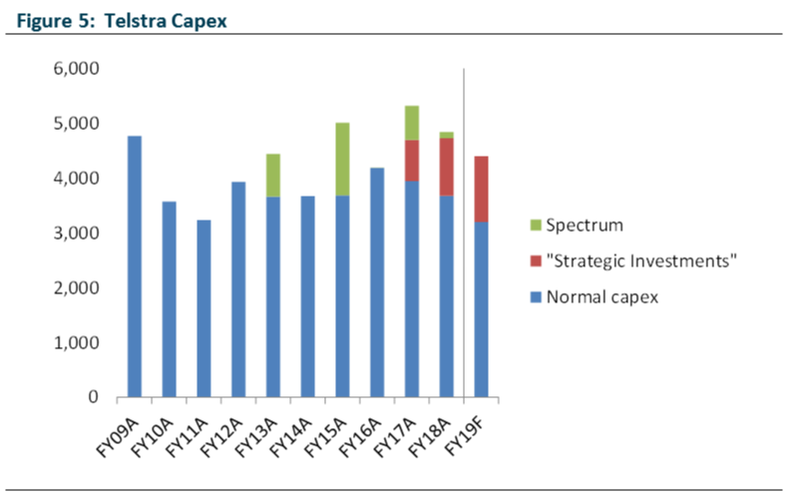

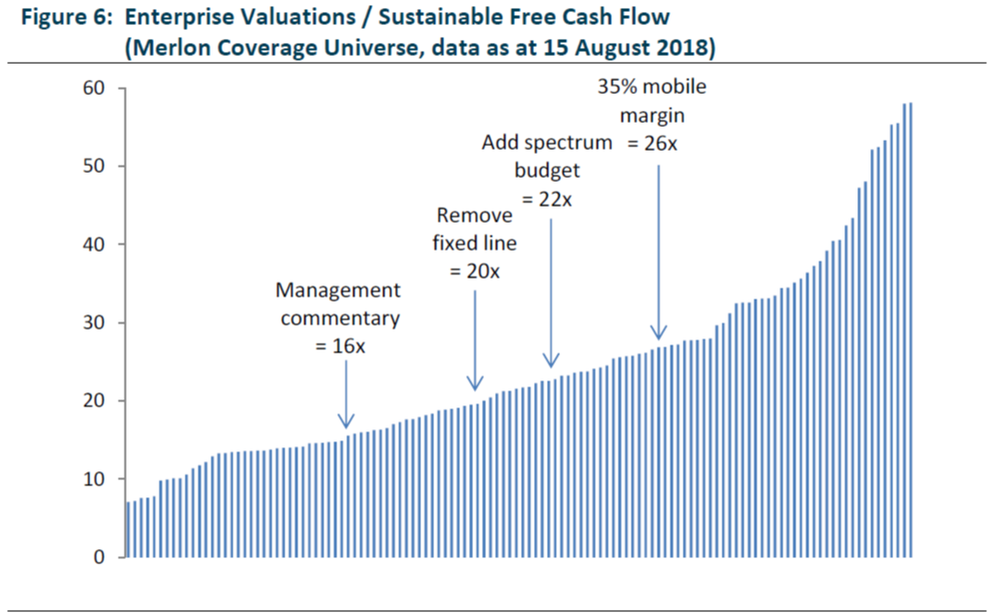

As a value investor we are not averse to investing in businesses that face growth challenges. The caveat of course is that market expectations have to be sufficiently low to make such companies good investments. If these types of businesses can halt their declines they can become great investments. The question remains with Telstra is whether expectations are sufficiently low and whether the company’s pace of contraction is close to moderating. Regauging Market Expectations As we have indicated previously, comparing a company’s share price with some measure of intrinsic value can give some indication as to whether market expectations are optimistic or pessimistic. Merlon’s preferred measure of intrinsic value is to compare a company’s enterprise (or unleveraged) value with its sustainable enterprise-free-cash-flow. To give a guide to management’s expectation of Telstra’s “sustainable free-cash-flow”, Telstra’s 2018 result announcement reiterated its 2019 guidance.  Source: Company 2019 full year result presentation, Merlon Capital Partners Taking into account anticipated one-off NBN receipts this would imply the company is trading on approximately 16x sustainable-free-cash-flow. This is cheaper than the 20x multiple we calculated in September last year and cheaper than the median multiple of 21x for all companies we cover suggesting to us that the market is skeptical about the management estimates of profitability and cash flow.  Source: Bloomberg, Merlon Capital Partners Key Issues A key tenant of Merlon’s investment philosophy is that markets are mostly efficient and that cheap stocks are always cheap for a reason. We are focused on understanding why cheap stocks are cheap. To be a good investment, market concerns need to be priced in or deemed invalid. We incorporate these aspects with a “conviction score” that feeds into our portfolio construction framework. In the case of Telstra, we flag three key issues: 1 - Telstra generated $1.9 billion in EBITDA from its fixed line business in 2018. This earnings stream is likely to deteriorate to a negligible amount over time but still probably contributes to the 2019 guidance estimate above. We note that margins for re-sellers are typically in the order of 5 to 10 percent but that NBN margins are currently tracking at levels below this. We also note that large segments of Telstra’s customer base are paying rates significantly higher than contemporary NBN products. In short, we don’t think 2019 will be the bottom for Telstra’s fixed line business;  Source: Bloomberg, Merlon Capital Partners 2 - Telstra’s mobile business is extraordinarily profitable by global standards. In 2018 the Telstra mobile business generated an EBITDA margin of close to 40 percent. While the company’s guidance no doubt builds in some margin compression, we again note that large segments of Telstra’s customer base are paying rates significantly higher than contemporary offers. At the same time, TPG has not yet launched in the Australian market;  Source: Bloomberg, Merlon Capital Partners 3 - Telstra’s capex aspirations could be optimistic. The $3.2 billion sustainable capex implied by management guidance would be the lowest in a decade for Telstra. We acknowledge that the company has no capex associated with its fixed line network as the NBN rolls out but arguably it has not spent much here over the last 12 months so the 10 year comparison is still valid. Further, we are unconvinced it is appropriate to exclude spectrum payments when considering sustainable capex;  Source: Bloomberg, Merlon Capital Partners Valuation Scenarios – Preparing for the Worst We can deal with issue 1 (legacy fixed line profits) simply by excluding the fixed line business from our analysis. We estimate that the fixed line business will generate about $0.5 billion in free cash flow during FY19 which would take the sustainable free cash flow estimate above down to about $2.4 billion and increases the market multiple to approximately 20x. This is not particularly cheap. Issue 2 (elevated mobile margins) is more subjective and best considered as a sensitivity. It is quite conceivable to us that Telstra’s mobile margin could revert to 35%. This would take about $0.3 billion from free cash flow. Not a disaster but a meaningful downside risk worth considering. Issue 3 (optimistic capex expectations) is also subjective. Our analysis of global network operators and telco re-sellers has consistently led us to conclude that Telstra’s capital expenditure should be significantly lower as a re-seller of fixed line services rather than vertically integrated network operator and that Telstra spends an unusually high amount on capital expenditure. This gives us some hope that management can deliver on its aspirations. Against this, we can’t explain why Telstra has had so much difficulty reining in its capex budget in recent years. One explanation is that Telstra’s capex is simply capitalised opex. In the least we feel it prudent to factor in a budget for spectrum payments which have averaged $0.3 billion per annum over the past decade.  Source: Bloomberg, Merlon Capital Partners The conclusion we draw is that the market’s caution is probably warranted. Simply removing legacy fixed line businesses and including a sensible spectrum budget would bring the Telstra valuation multiple into the middle of the pack for Australian listed companies. Using more conservative – but certainly reasonable – margin scenarios for the mobile business would start to make the company look expensive. What About the Cost-Out Opportunities? As highlighted above, Telstra’s strategy has dramatically pivoted from aspirations of becoming a global technology company to a cost-out and product simplification agenda. The company is targeting $2.5 billion in cost savings between 2016 and 2022 and claims it has delivered approximately $0.7 billion cumulatively so far. That leaves $1.8 billion in savings from here. Offsetting this $1.8 billion cost save agenda are the following items:

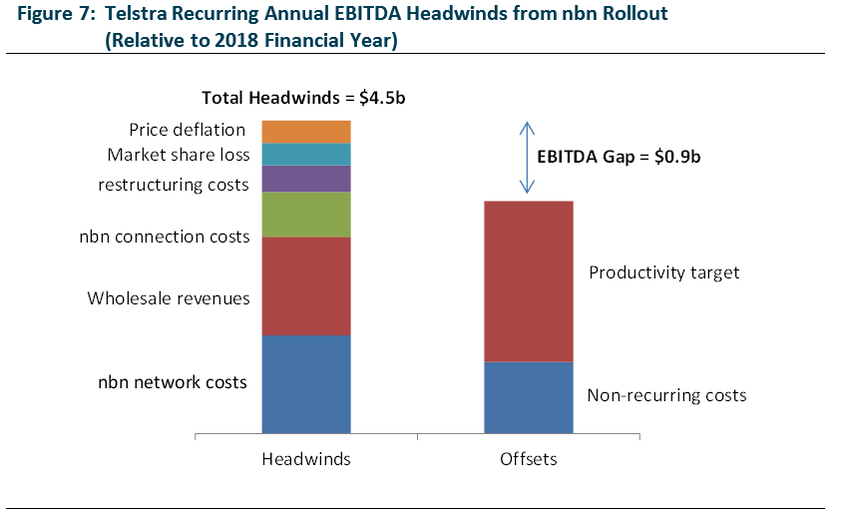

Taking into account all these factors we observe an EBITDA gap of approximately $1 billion which roughly reflects the company’s anticipated step down in EBITDA during FY19. The good news is that this appears factored in to guidance. The bad news is that it doesn’t leave much headroom if things go wrong.  Source: Company reports, Merlon Capital Partners Portfolio Positioning

It is clear to us that following recent underperformance, repositioning of the strategy and rebasing of expectations that Telstra is a more attractive proposition than it was a year ago. However, we do not regard the company as particularly cheap when we adjust for legacy fixed line cash flows and include a sensible ongoing budget for spectrum purchases. Further, we can envisage a scenario where mobile competition intensifies further than anticipated. We don’t think announced (and yet to be delivered) cost programs will offset the various headwinds that the company is dealing with. As such, we don’t own Telstra.

2 Comments

john pearce

27/10/2018 07:47:38 am

useful article which will be reviewed in 1-2 years

david buckwalter

1/11/2018 08:28:40 pm

If I wasn't a long time invested in Telstra I would not own them. Soon as they get to my cost if they do I am out the door. There are a lot of dividend stock with grouth out there to replace telstra. Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim