|

With Reporting Season coming to a close a few weeks back the managers behind the TAMIM Australian Equity Small Cap IMA take a look at some of their previously disclosed stocks and how they fared over what was a rocky few weeks at the smaller end of town. A summary of the half year results from a selection of our previously disclosed positions is detailed below: Konekt Limited (ASX:KKT)(February return: -1%) HY17 result highlights - (*) normalised

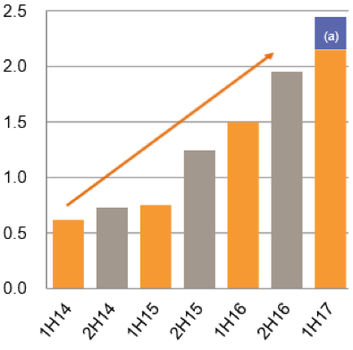

Comment:KKT, a leading provider of workplace injury management and prevention services reported a strong half year result. Operational highlights included a significant panel appointment in the Commonwealth government sector and being re-appointed as a service provider to two major financial institutions. KKT continued to benefit from the increased scale of the business with underlying EBITDA margins increasing from 10% to 11%, resulting in significant earnings growth. KKT’s increasing EPS trend (by half year) is shown below:  Source: KKT Investor Presentation 15 Feb 2017 KKT noted it is well positioned going into 2H17 with good momentum in the business. KKT has forecast total FY17 revenues of between $51.0m to $53.5m, which is a 14% to 21% increase over FY16. As advised in our January update, KKT is currently re-negotiating a major customer contract, and until the outcome of that is known, its share price is likely to remain weak. We therefore suggest a significant amount of caution with respect to KKT. Joyce Corp Limited (ASX:JYC)(February return: -5%) HY17 result highlights - (*) normalised

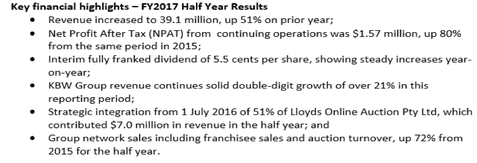

Comment:Joyce Corporation, an investment company that owns the Bedshed Franchise, Australia’s largest kitchen renovation company and a leading online auction company, reported a strong operating result relative to the previous corresponding period. The key highlights from its result are summarized below:  Source: JYC Results announcement 24 Feb 2017 JYC advised that the group is poised for further growth and the underlying business units are continuing with their solid performance into the second half, with the Chairman noting that “The Company is in an enviable financial position with profitable businesses, low debt and substantial growth opportunities which provides a strong level of security for our shareholders." Fiducian Group (ASX:FID)(February return: 10%) HY17 result highlights - (*) normalised

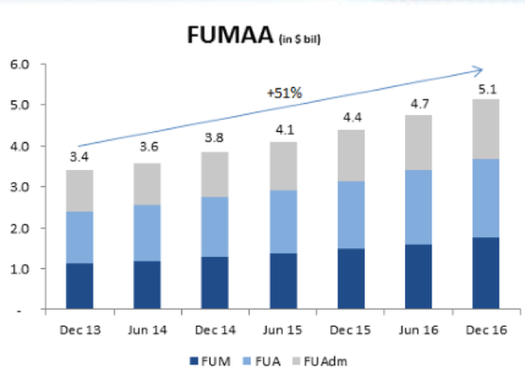

Comment:Integrated financial services company FID reported an increase in its underlying after tax profit in HY17 of 23%. Its total funds under management, administration and advice (FUMAA) increased 16% to $5.1b over the 12 months. FID’s increasing FUMAA trend is illustrated below:  Source: FID results announcement 17 Feb 2017 With 41 offices throughout Australia, FID is now a substantial national financial services business, benefitting from increasing recurring revenue. FID is well placed to continue to build scale organically and through acquisitions, and to leverage its integrated service offerings to “deliver consistent double digit earnings growth in coming years”. FID noted that they have recorded double digit annual EPS growth in 13 out of the 17 years it has been listed. SDI Limited (ASX: SDI)(February return: -25%) HY17 result highlights - (*) normalised

Comment:Global dental product manufacturer, SDI, produced a disappointing profit result at the lower end of its previous guidance range ($2m NPAT). While sales of its higher quality non-amalgam products are growing, its older amalgam products are declining faster than expected and previously guided for, such that SDI is expecting only marginal total sales growth over the course of this year. Adverse currency movements have further reduced profits relative to the previous period, resulting in significant earnings volatility.  Source: SDI results announcement 23 Feb 2017 SDI have forecast sales growth in Non-Amalgam products to increase by approximately 10% while Amalgam sales (~30% of total sales) will decrease by 13%, equating to a total sales increase of approximately 2% for FY17. Pioneer Credit Limited (ASX:PNC)(February return: 3%) HY17 result highlights - (*) normalised

Comment:Debt purchaser PNC reported a solid result and evidence of further pleasing execution on its development. Vendor partner relationships appear strong with PNC now having secured (under contract) full year PDP investment of at least $53m (up from an initial guidance of $50m) within the half-year, representing solid market share gains. The business is expanding (& diversifying) well, with customer numbers having increased to over 160,000 and its first NZ portfolio secured during the half.  Source: PNC Investor Presentation 24 February 2017 PNC has re-affirmed its forecast FY17 NPAT of at least $10.5m, while its investments made during the year are likely to position it for a particularly strong FY18 result. Elanor Investors (ASX:ENN)(February return: -4%) HY17 result highlights - (*) normalised

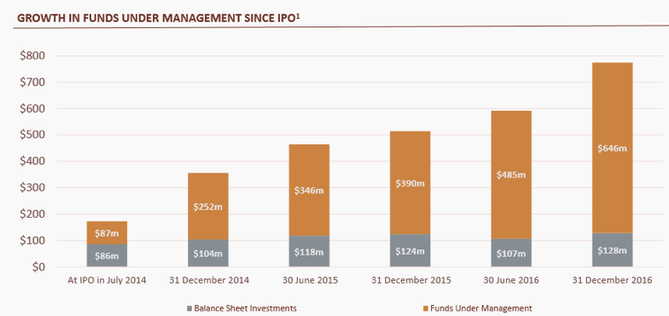

Comment:Fund manager and asset owner ENN reported a solid operating result. ENN’s key strategic objective is to grow its funds management business and since 31 December 2015, total funds under management and balance sheet investments have increased to $774m reflecting a 50.6% increase on PCP. Earnings highlights included a 90% increase in Funds Management earnings to $7.8m, while earnings from Hotels, Tourism and Leisure assets showed significant year on year growth.  Source: ENN Investor Presentation 22 Feb 2017 ENN noted that they have a number of funds management initiatives in progress, though there are challenges associated with securing quality assets in the current environment.

Of interest is the possible announcement over the next several weeks regarding the sale of ENN’s Merrylands investment property – this will be a significant development for ENN, potentially raising $40m - $50m in cash (currently held on balance sheet at $16.6m). Comments are closed.

|

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim