|

As most investors know, retail is a tough game. In the last twelve months we have seen many retailers struggle with sluggish consumer spending, bush fires impacting sales and more recently the drop off in tourism from the coronavirus, COVID-19. But, not all retailers are made the same. Despite all this doom and gloom, three retailers we own delivered strong results recently. But why are these retailers outperforming their peers? Read on to find out.  When investing in retail stocks we look for the following characteristics:

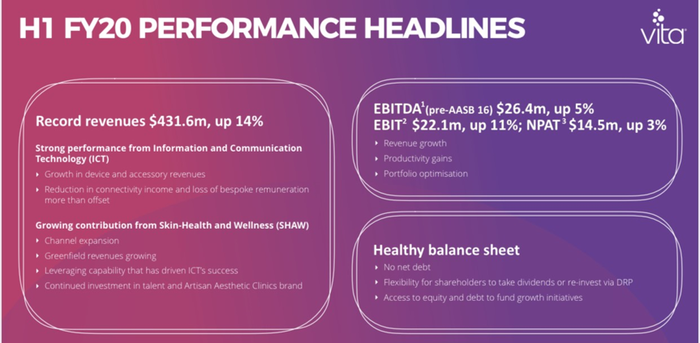

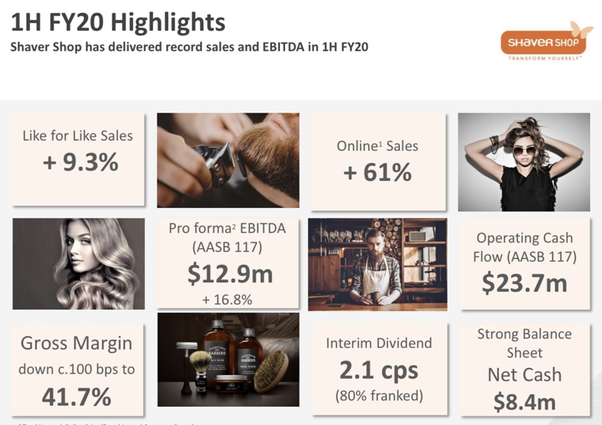

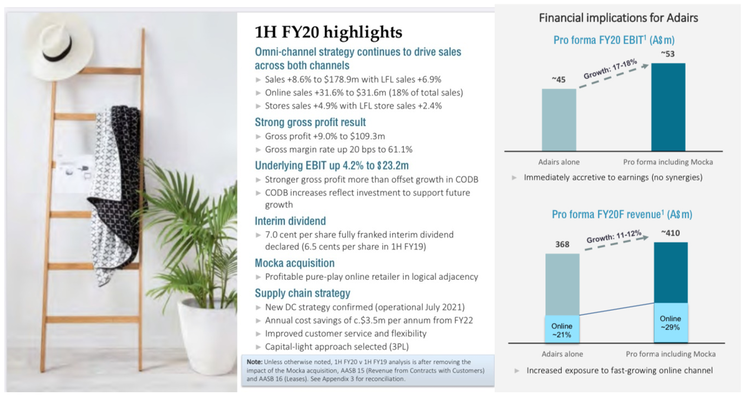

We own three stocks that, in our mind, fit those criteria, reported strong 1H FY20 results and are trading at meaningful discounts to their valuations. Vita Group (VTG.ASX) VTG is the largest Telstra mobile store reseller with a footprint of 100+ stores. The business has been around for twenty-five years and is managed by its founder and one of the best retail executives in Australia, Maxine Horne. The business has gone through a number of transformations over the years and has proven to be resilient in terms of profitability and cash flows. The Telstra relationship provides some risk in terms of changes to remuneration every few years. We see this part of their business as a cash cow that in any given year generates $40m+ of EBITDA and throws off $15-$20m p.a. of free cash. 1H results had recorded revenues of $432m, up +14%, and NPAT of $14.5m.  Source: VTG company filings The more appealing part of the Vita Group growth story is the skin care and beauty brand called Artisan Aesthetics Clinics. VTG launched the brand over eighteen months ago and is on track to have 20+ clinics by June 2020, generating over $25m of revenue. VTG is targeting 60+ clinics in the next 3-5 years and, at maturity and scale, we see this network of clinics generating $30-$40m of incremental EBITDA. VTG is cheap, trading on 9x PE and a 7% fully franked (ff) dividend yield with a net cash position of $24m. We expect the market to apply a growth multiple on the stock as the clinic business begins contributing to profitability over the next twelve months and the telco stores continue to stay resilient. We value VTG at $2.25. The upside scenario in three years is a company generating $85m+ of EBITDA valued at $4.50 or 3x the current valuation. Shaver Shop (SSG.ASX) Shaver Shop the leading hair and body grooming retailer in Australia with 122 stores nationwide. The business has a strong brand, generates healthy cash flows and has a strong balance sheet ($8.3m net cash). SSG provides a great store experience that appeals to all consumers. Over the last year, the company has focused on growing their online channel with great success. Online sales are already at 18% and have grown by +60% in 1H FY20.  Source: SSG company filings SSG reported very strong sales growth of +12% (to $108m) in 1H FY20 but more importantly like for like sales grew +9.3%. Cash NPAT grew to $8.6m and EPS to 7 cents. We see SSG continuing to grow online sales and we see no reason why the online component can’t reach 30% of sales within the next two years. SSG trades on a PE of less than 10x and pays an attractive ff dividend yield of 6%. We value SSG at $1.10 or 50% upside from the current price. Adairs (ADH.ASX) ADH is a homeware and bedding accessories retailer. The business has strong brand awareness and a conservative management team. Sales growth has slowed down in the last twelve months as consumer confidence has been sluggish. Management’s strategy is to open larger format stores alongside a handful of new stores each year. 1H FY20 results came in line with revenues of $179m, up +9%, and NPAT of about $16m. The balance sheet is solid.  Source: ADH company filings In December last year, ADH acquired fast-growing online retailer Mocka, who specialise in furniture, bedding and homewares. Mocka transforms the growth profile of ADH and increases online sales to almost 30% for the group. We see ADH earning over 20 cents EPS this year and 24 cents in FY21. Dividend yield is 6% ff. Following the half year result, investors are beginning to ascribe the business a growth multiple compared to its peers Kogan (KGN.ASX), Temple & Webster (TPW.ASX) and the like. We value ADH at about $3.30.

4 Comments

David K

27/2/2020 04:17:24 pm

I agree Adairs is a quality operation, and Vita (though I recently sold it at a big loss- due to having it prior to the Telstra problem) is interesting due to the cosmetic line (but that is a risk as it’s competitive and they new to it. )

Ron Shamgar

2/3/2020 09:07:35 am

Thanks for your comment.

Ryan

27/2/2020 08:32:32 pm

CCX is the best retail in my opinion.

Steven Heath

28/2/2020 12:24:32 am

Nice piece, will watch them all with interest, especially atmo. Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim