|

This week we look at a small cap telco company that we believe is misunderstood and is offering significant upside. The company has been gaining a significant share of the SME telco market on the back of a strategic M&A plan, leading to transformative acquisitions for the company. Given the synergies made possible by the takeovers, the company is now looking extremely cheap. Vonex (VN8.ASX) Author: Ron Shamgar Author: Ron Shamgar Vonex is an Australian telecommunications company providing innovative Voice over IP (Internet Protocol), or VoIP, solutions. They currently provide mobile, internet, traditional fixed lines, and hosted PBX and VoIP services. VN8 provides these predominately to small to medium enterprise (SME) customers under the Vonex brand. Vonex is employing an aggressive acquisition strategy to grow revenues at scale. SMEs are the core of VN8’s business. There is clearly an unmet need among Australian SMEs for telco services that are reliable, affordable, flexible, scalable and friendly to the new 'work from home' paradigm. Vonex's strong focus on product-market fit, efficiency and customer satisfaction resonates with their SME customers; most SMEs simply don't have the luxury of an in-house specialist to handle things like if their telecommunications are set up properly or if they are managed and utilised to best capacity. Being a smaller telco, VN8 is able to offer a superior customer service experience for SMEs. VN8 is providing customised solutions for business’ telecommunication services, they have NBN and business grade fibre packages. VN8 continue to offer a premium customer service experience whilst growing the business.

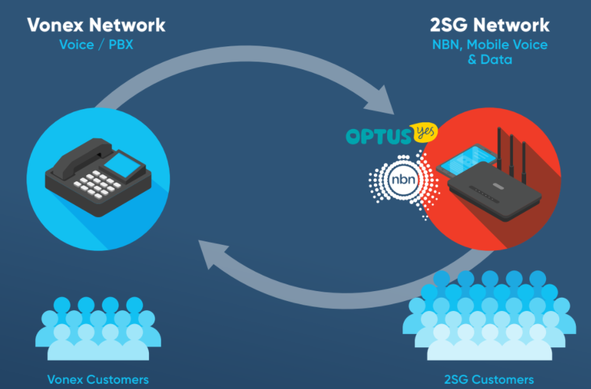

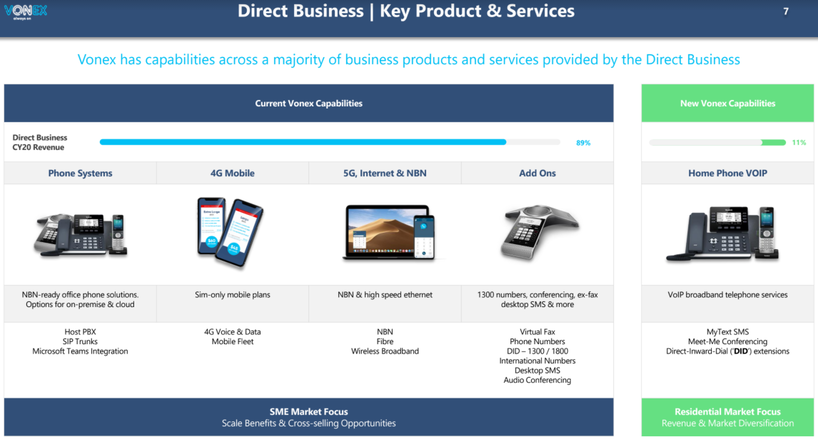

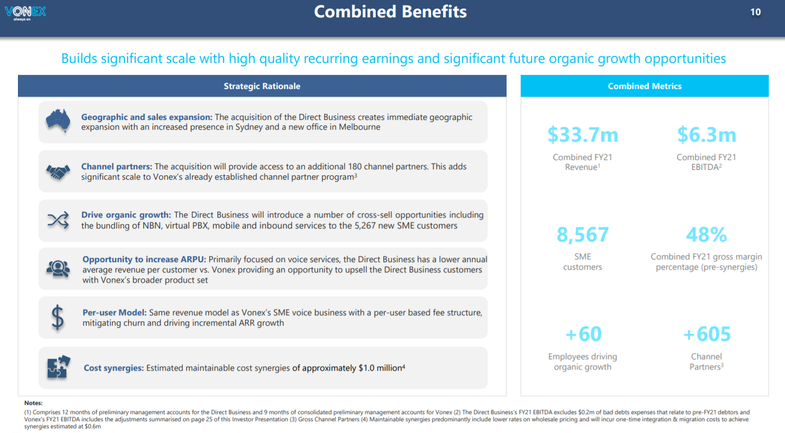

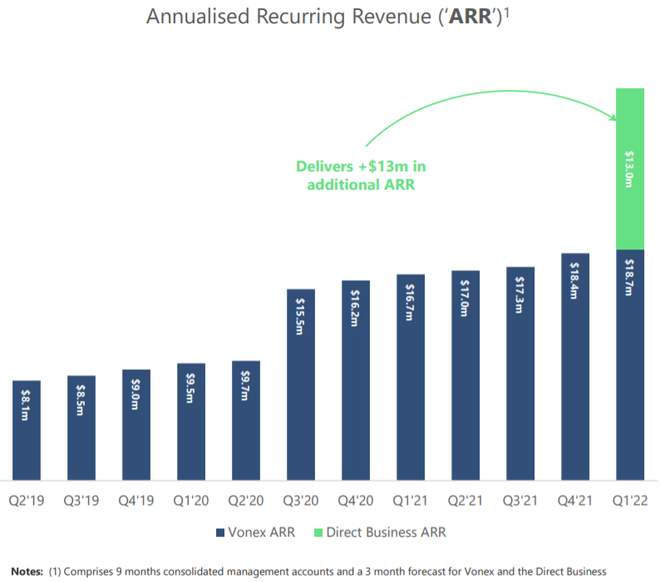

Strategy: VN8’s strategy has been to make acquisitions of small but profitable telcos that give VN8 a greater range of product offerings that also have existing SME customers. This strategy has enabled VN8 to capitalise on significant cross selling opportunities, realise cost saving synergies as well as increase their presence throughout Australia. 2SG Acquisition In March 2020 Vonex completed its acquisition of the 2SG business for a consideration of $2.6m. 2SG is an established wholesale provider of hardware and connectivity solutions. The integration of 2SG has brought a new dimension to Vonex’s business along with 150+ new wholesale customers. This has allowed Vonex to expand its offering to SME customers with new products, including fleet mobile, mobile broadband and NBN with 4G backup.  Source: VN8 company filings Vonex’s provision of fast, secure, business-grade wireless broadband through 2SG has met strong customer demand amid the rise of working from home across Australia and has provided VN8 with a significant cross selling opportunity. 2SG are long term partners with all tier one carriers - including Telstra, Optus, NBN, Vocus and AAPT - which makes delivering reliable and secure connectivity products effortless. 2SG added an additional $7m in annual recurring revenue to the VN8 business.  Source: VN8 company filings MNF Group Acquisition In August this year VN8 announced that they will be acquiring MNF Group’s direct business. This business sells cloud phone, internet and mobile services to SMEs and consumer customers. The rationale behind this deal is compelling and has significant synergies. The deal will add more than 5,250 new SME customers and 180 new channel partners, effectively almost double VN8’s recurring revenue.  Sourrce: VN8 company filings The deal will also provide VN8 with geographic benefits as they will have a larger presence in both of the key markets that are Sydney and Melbourne. MNF’s direct business has the same revenue model as Vonex and will also carry cost saving synergies of around $1m. MNF’s direct business delivered an unaudited FY21 EBITDA of $5.5m. Given the size of the transaction and capacity to substantially increase VN8’s customer base, national reach, recurring revenues and cross selling opportunities, this deal is transformative for Vonex.  Source: VN8 company filings Qantas Rewards Partnership In August 2019 Vonex partnered with Qantas as an official telco provider to the Qantas Business Rewards (QBR) program, offering uncapped Qantas Points to QBR’s database of 250,000 SME members for doing business in the cloud. This partnership is providing VN8 with valuable marketing and outreach to SMEs to further support VN8’s growth. This partnership should get more and more valuable as VN8 increase product range. Valuation

On a proforma basis after realising the synergies from the MNF acquisition, VN8 would be reporting an EBITDA for FY21 of $7.3m and NPAT of $5.3m. This puts VN8 at an EV/EBITDA of approximately 6x, extremely cheap in our opinion. Looking forward, this multiple would be even less when you factor in growth. To put that in perspective over the wire holdings (ASX:OTW) another telco provider is trading at circa 12 times EV/EBITDA. The majority of VN8’s revenue is recurring which provides great earnings visibility for the future. VN8 is already a profitable business (proforma indicates $6.8m of free cash flow post synergies) and they also have $10m in cash; they are well funded to continue their growth accretive acquisition strategy. We believe the market hasn’t yet priced in the synergies that MNF is bringing to the group, VN8’s quarterly figures will look quite different to what the market is pricing in.  Source: VN8 company filings Outlook

We see the upcoming quarterly update (October) as a potentially huge catalyst for VN8. This Quarterly will begin to show the impacts of the MNF acquisition as their customers are integrated into VN8’s platform. In an update earlier this week VN8 reported strong growth in retail customer revenue in the first part-month (August 2021) post-acquisition of the MNF Direct Business; monthly retail/SME customer billings have increased by more than 185% year-on-year to $2.25m. VN8 are well funded to continue their aggressive M&A plan and have proven they can exploit significant synergies and add growth to the business through this strategy. On the back of their partnership with Qantas Rewards, VN8 are in a great position to scale this business. At these prices, VN8 could also be an attractive takeover target. Another of our holdings, Aussie Broadband (ABB.ASX), have recently completed a $110m placement to fund an aggressive M&A strategy; VN8 could make an interesting takeover target for the likes of ABB. When the market starts to price in the MNF acquisition, we can see VN8 trading closer to the 20 cent mark.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim