|

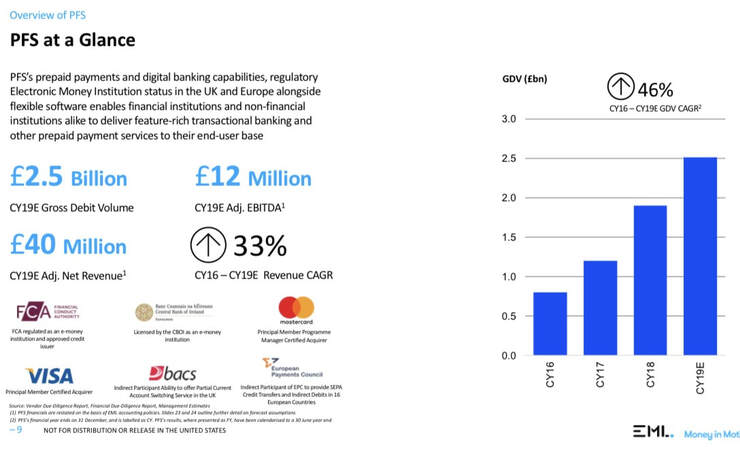

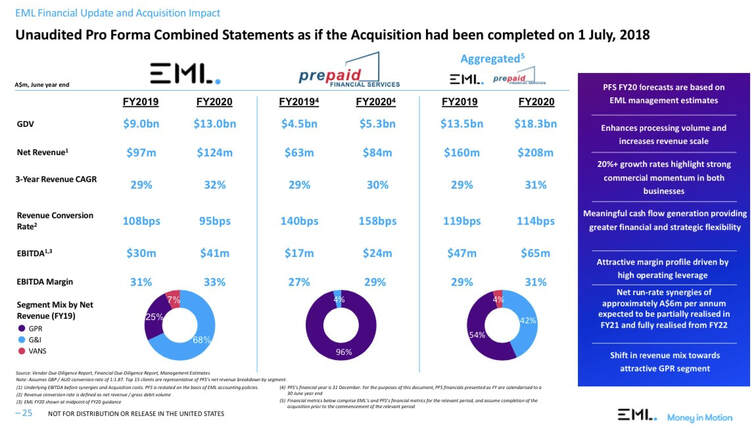

This week we take a look at our largest holding, EML Payments (EML), and the transformational acquisition they have undertaken. EML is now a substantial and profitable global fintech company that we believe is going to double in price over the next twelve months. We first bought into EML at around the $1.40 mark back in December 2018. EML has been our largest holding ever since. We spotlighted the stock back in February and have continued to provide our insights all year. Since day one we have said that, in our mind, EML is one of the highest quality companies on the ASX, having a predictable cash generative revenue stream that is growing fast and enjoying strong structural tailwinds globally. The stock has since tripled to well over the $4.00 mark and, with this week’s game changing acquisition of European company Prepaid Financial Services (PFS), we believe EML is set to double again over the next twelve months. EML is acquiring PFS for $423m which includes an equity raise, debt and vendor equity. PFS is an award winning European fintech based in the UK. The company was founded by Noel Moran and his wife in 2008 and has been profitable and self-funding ever since (it is no wonder the couple have owned over 80% of PFS to this point). Noel Moran has also been awarded the CEO of the year in Europe for the second year running. PFS has grown to become a major European player across the emerging verticals of digital banking services, government disbursement payments, consumer prepaid cards and multi-currency travel cards. Similar to EML, and unlike many global fintechs, PFS has grown profitably year on year. PFS is forecast to generate $84m revenue and $24m EBITDA while processing $5.4bn of Gross Debit Volume (GDV) in FY20.  Source: EML company filings There are currently fifteen million millennial Europeans who are customers of digital banks across Europe. That figure is projected to grow to 85 million over the next 5+ years. We see EML powering these banks and enabling them to grow. PFS not only brings scale and added profitability to EML, but it provides further diversity across different verticals, product solutions and capabilities, and growth optionality that were not available to EML prior. More importantly PFS will reduce the proportion of EML’s revenue derived from gift cards (breakage income) and increase the group cash conversion to over 80% of profits. In addition, there are significant processing efficiencies by combining the two companies and management estimates over $6m of cost synergies will be achieved within two years. Management has emphasized the cultural fit within both businesses and all staff will be retained. We see significant cross sell opportunities available to both companies across different geographies and product suites (no overlap in product set).  Source: EML company filings PFS has been growing at 33% p.a. over the last few years and both the CEO (founder Noel Moran) and COO are incentivised to exceed historical growth rates over the next three years to achieve an earn out of up to $103m. As a combined group and on a pro forma basis for FY20, management is forecasting GDV of $18.3bn, revenues of $208m and EBITDA of $65m. If we take into account the $6m in synergies and apply both companies’ growth rates of 25% for the next two years (actual current growth rates are in excess of 30%), we can see EML generating over $110m EBITDA in FY22. There aren’t too many global fintechs that can generate these growth rates in both top line revenue and, more importantly, bottom line profitability. The peer group that are profitable are seeing growth of about 15%+ p.a. and are trading on forward multiples of 18x. EML, on the other hand, is projected to grow at 25%+ p.a. for the next few years. We believe EML at this point in time deserves a premium of 25x multiple. Apply that to our FY22 forecast and we see an EML valuation of almost $3bn in market cap or, in other words, just under $9.00 per share.  Source: EML company filings With the shares trading around $4.00 prior to the deal (closing at $4.35 yesterday in the wake of the news), we expect a substantial re-rating of the stock over the next twelve months as investors take the time to comprehend the magnitude of the deal, the different growth optionality now available to EML, and the upcoming inclusion into the ASX200 index. All of the above will see the larger funds and index trackers forced to buy the stock as not many companies in the ASX200 present such impressive global growth rates, profitability, and a recurring revenue profile that is so highly diversified and predictable. We took the opportunity this past week to attend EMLcon (what they call their investor day) and listen to some of EML’s global customers presenting about how EML partners with them to help grow their businesses and innovate. We also took the opportunity to meet EML staff and were impressed with the feedback received about how passionate they are working at EML. We came away from the event with the one conclusion - the world is in the midst of a payments revolution. Traditional banks and credit providers are being disrupted by new and emerging fintechs. Consumers are no longer using cash with mobile and debit card payments taking over. EML is helping facilitate this structural shift from the background, powering these companies and providing the infrastructure, innovation and capabilities required to process these payments. EML is the largest holding in the TAMIM Australian All Cap portfolio and will remain so for the foreseeable future. Ron Shamgar is responsible for overseeing both the Australian All Cap and Small Cap Income portfolios. Both have acheived outstanding returns this calendar year to date (CYTD).

Should you be interested in either of these portfolios then please do not hesitate to contact us for a more in depth discussion.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim