|

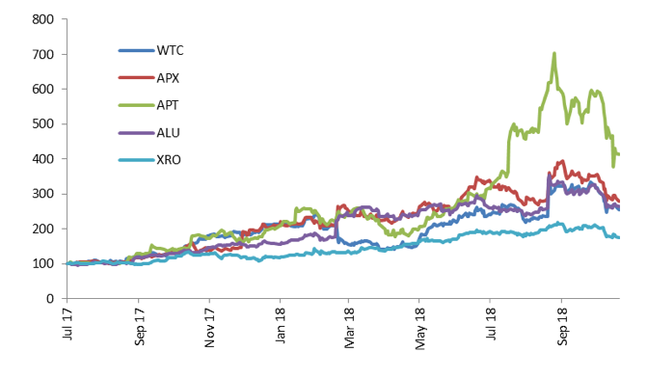

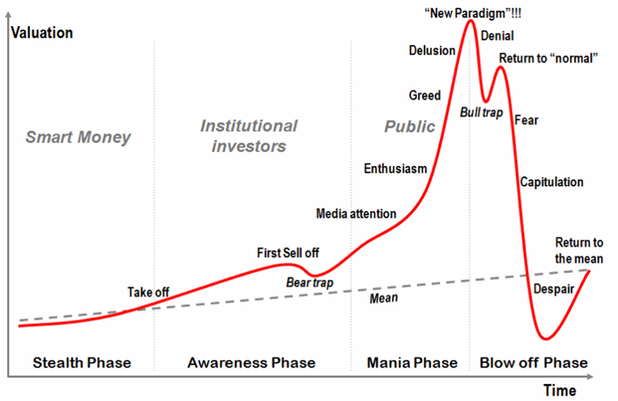

Guy Carson, of Quick Brown Fox Asset Management and the TAMIM All Cap Value IMA, examines the cracks that are beginning to appear in Australia's WAAAX stocks. Global markets in recent times have increasingly been driven by a small number of stocks. These stocks have typically been in the technology sector and as a result many similarities have been drawn to the late 1990s. In the US the most popularised of these stocks have been the FANGs (Facebook, Amazon, Netflix and Google). In Australia we have seen our own version, the WAAAX (Wisetech Global, Afterpay, Altium, Appen and Xero) deliver outsized returns. The chart below shows the performance of these stocks from 1 July 2017. At its high Afterpay shareholders had seen a return of over 7 times in this short time period. The laggard of the group, Xero, has “only” seen its share price appreciate by 75%.  You may notice from the above chart that the dream run has ended. The rally has well and truly stalled. All of the five companies are now well off their recent highs and have experienced significant volatility in recent times; 4-5% daily moves are not unusual. In fact we would suggest that all five are showing, to varying degrees, signs of a bubble that is bursting. If we were to guess where we are it would somewhere between “Return to normal” and “Fear” in the typical bubble chart seen below.  Source: Dr John-Paul Rodrigue, Department of Economics & Geography, Hofstra University We have been vocal in recent months about the excessive valuations. Back in July we wrote about the market as a whole being overvalued (see here). We pointed out at the time that the overvaluation was driven by extreme overvaluation in the Technology and Healthcare sectors. We reiterated our concerns about the Technology sector in September (see here). Some market commentators disagreed with us. Exhibit A:  Source: Livewire Markets We believe the market has now started to come around to our point of view. Last week we saw some major cracks develop, driven by a substantial fall in the Afterpay share price.

This fall came about due to a media story stating that ASIC was finalising a report into the “Buy Now, Pay Later” industry. This report is expected to be released before the end of the year. In our opinion there have always been two key risks with Afterpay.

We held off buying Afterpay due to these risks. Many of the early holders have done well but many late to the party are stuck in a tough position. The company recently took advantage of its surging share price to raise equity at $17.05 per share. With the price now at $12.64 many investors are underwater. The major problem in buying or holding the WAAAX shares recently has been the valuation. Afterpay has traded at a multiple of over 100x earnings, as has Wisetech Global. Everyone is looking for the next Google or the next Amazon with the scalability to grow earnings at 20-30% over a long time period. We are not sure they exist here. Google is a truly global business; it operates the same way across borders. A business such as Wisetech Global may operate in many countries but its product needs to be unique to the legislative requirements in each jurisdiction. At its heart it is an international roll up and we believe the market is overestimating potential synergies. We are not against the Technology sector at all. In fact it remains our largest exposure, although we have reduced it significantly over the course of this year. We like quality companies and from the WAAAX contingent we have owned Altium and Appen in the past. We would own them again at the right price but we are far from there. The Technology companies that we do own currently trade at much more reasonable valuations. Some people might say that you can pay the current valuations if you have a long term view. We would question that approach. If you bought Microsoft at its high in 1999, it took you over 15 years to see a profit. If you bought Intel at its dotcom peak, you would still be in negative territory today including all dividends you had received. Paying the wrong price for a great company can be as destructive to your capital as buying a bad business. When we couple the overvaluation in the hot sectors of the market with the current state of the housing market, we are starting to become increasingly cautious. Our cash levels have risen over the course of this year. Recently we have added a small short position on the index and have added some US Dollar exposure to client portfolios. We expect the Australian economy will start to struggle in 2019 as the housing construction market peaks and we believe it will start to weigh on employment. Just in recent weeks we have started to see the impact of a slowing economy with earnings downgrades from Flight Centre, The Reject Shop and Nick Scali. We continue to avoid the banks, the retailers and companies exposed to the property market. The RBA is in no position to raise rates whilst the Federal Reserve continues to raise their rates higher every three months. The result is an increasing yield gap with US 10 year rates currently at 3.17% versus Australia at 2.66%. This gap makes US Dollars much more favourable and we expect to see further weakness in the Australian Dollar. We believe this cycle is in the process of peaking and that returns are going to be difficult to generate. We believe returns will be more “Macro” driven and that portfolios should be positioned accordingly.

1 Comment

john pearce

26/10/2018 04:58:30 pm

enjoyable reading & a help in reaching general finance position Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim