|

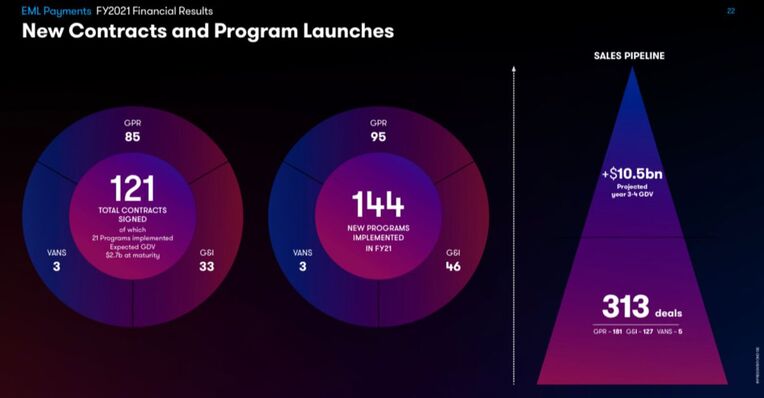

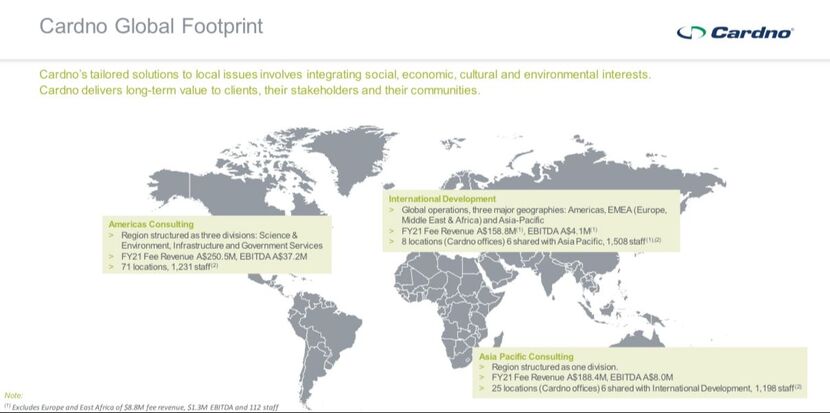

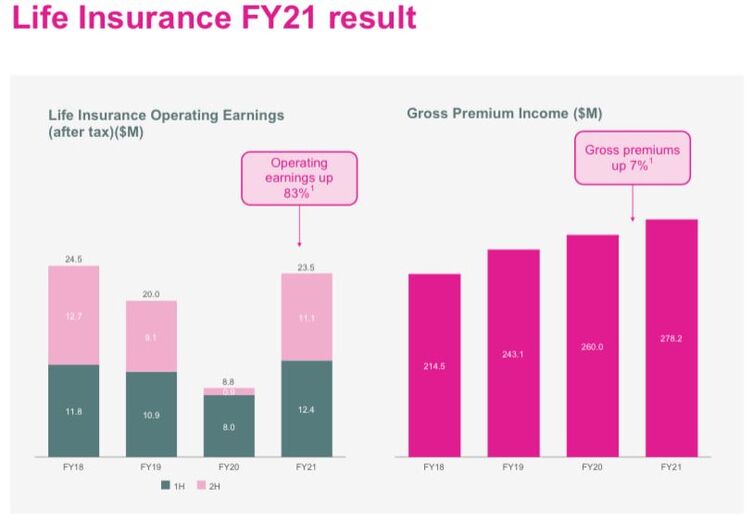

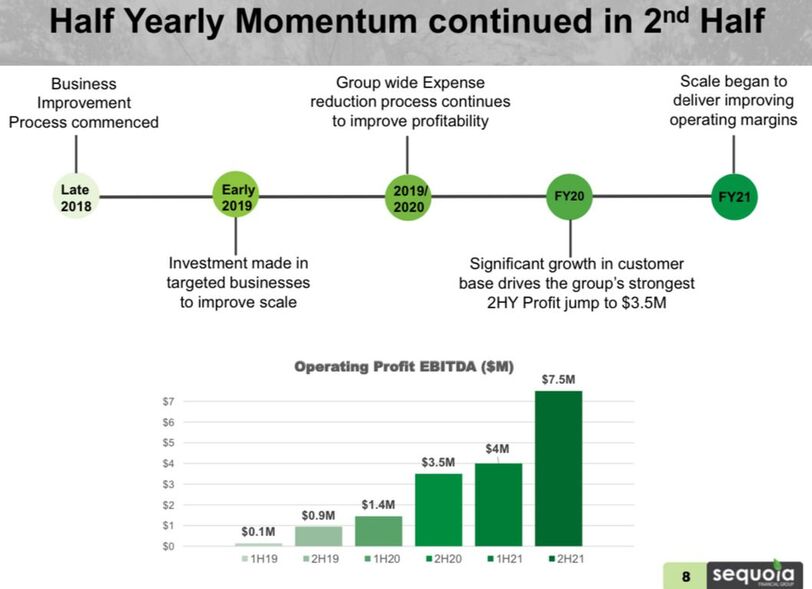

Ron Shamgar provides an update on a number of the companies held in TAMIM's Australian equities portfolios.  Author: Ron Shamgar Author: Ron Shamgar This is an excerpt from the August updates for the Australian equity strategies in the TAMIM Fund, you can access these reports here: TAMIM Fund: Australia All Cap TAMIM Fund: Australia Small Cap Income Uniti Group (UWL.ASX)Uniti Group (UWL.ASX) reported one of the best results we have seen. FY21 EBITDA was $93.7m and above consensus. The June 2021 exit run-rate EBITDA came in at $133.4m. UWL also reported Free Cash Flow at 68% of EBITDA and a contracted FTTP ‘order book’ expanding by 24% to over 250,000 premises in 2H. During the half, 16,000 premises were connected. Finally, net leverage reduced to 1.5x June 2021 exit run-rate EBITDA, allowing management to consider future dividends or further asset purchases.  Source: UWL company filings The current lockdown situation could see some delays in certain developments but, overall, we believe future growth for UWL is all but guaranteed for the next few years. We estimate FY23 EBITDA at $165m, placing the stock on 18x. Pretty good for one of the most defensive core infrastructure business models on the entire ASX. Our valuation is $5.00. EML Payments (EML.ASX)EML Payments (EML.ASX) reported a strong underlying result in FY21. Gross Debit Value (GDV) was $19.7bn (+42%), Revenue $194.2m (+60%) and Underlying EBITDA came in at $53.5m (+65%), all at the top end of guidance. The Central Bank of Ireland investigation update was benign. An $11m provision was made with a remediation program well underway. This will be substantially complete by the end of CY21, with any remaining issues to be resolved by March 2022. Most of the additional ongoing costs will be personnel, at around $5m per annum.  Source: EML company filings Overall, as we predicted, the CBI issue ended up being more of a storm in a teacup situation; at the time the market wiped $800m of value off in one day, so much for forward thinking investors! EML guided to $58-$65m of EBITDA in FY22, 15% below consensus. With more certainty on the launch of new business through the year, we expect guidance to tighten towards the high end. EML’s pipeline has increased to $10.4bn of GDV and we see a clear path for the company to reach $400m of revenues and $140m of EBITDA by FY25. At those levels, we see a valuation of around $10.00. People Infrastructure (PPE.ASX)People Infrastructure (PPE.ASX) reported underlying EBITDA of $38m and NPATA of $25m for FY21. Performance was strong across the group with all industry verticals contributing to growth. Healthcare delivered a 14% increase in billable hours; Community Services grew billable hours by 10% and Technology has exceeded expectations after a difficult pandemic impacted first half. The Industrial and Specialist Services vertical also had a strong half with billable hours up 23%. PPE continues to deliver ahead of market expectations and has now produced 27% p.a. EPS growth over the last five years.  Source: PPE company filings In our view, valuation metrics remain attractive with FY22 PE of 14x and EV/EBITDA of 9x. While lockdowns have had an effect on segments such as nursing, childcare and some blue collar industries, the impact has not been particularly material. Acquisitions will continue to drive earnings higher as PPE now has $50-$70m of capacity. Cardno (CDD.ASX)Cardno (CDD.ASX) reported strong results for FY21, exceeding recent guidance and indicating favourable conditions for government infrastructure spending both here and in the US. CDD reported EBITDA of $51.2m, up 19% on FY20. The company announced a final dividend of 4 cents due to the balance sheet being in a net cash position. Despite the challenges associated with COVID, FY22 commenced with encouraging levels of backlog and a pipeline of future work.  The Board expects that the business will continue to grow in FY22 but has chosen to not provide explicit earnings guidance to the market due to the ongoing Strategic Review process. In other words, a takeover might just be imminent! We expect a deal at around $1.30+. Clearview (CVW.ASX)Clearview (CVW.ASX) is a life insurance provider with about 6% market share of the Australian market. FY21 underlying NPAT was up 54% to $22.7m on the back of strong underlying claims and lapse performance. The life insurance industry is now more focused on profitability in the wake of the APRA reforms. CVW is seeing further growth in FY22 and, due to recent industry consolidation, the company has divested its wealth advice division to Centerpoint Alliance (CAF.ASX) for a 25% holding in the enlarged group. Additionally, the company has put itself up for sale, led by its largest investor (Crescent Capital) wanting to exit the register (the same process as CDD and ITG).  Source: CVW company filings The embedded value (EV) of CVW is 96 cents and most insurance companies get acquired for EV or a premium to EV for growth companies. CVW management have told us that they believe they are in growth mode. We believe a takeover will come from an overseas player and we estimate 6-9 months to completion. We believe a takeover would be in the range of 96 cents to $1.10 (i.e. 50% upside to current prices). Sequoia Financial (SEQ.ASX)Sequoia Financial (SEQ.ASX) provides financial services to advisers in wealth management. Currently servicing 400+ advisors, they also own Morrison Securities which provides trading clearing services to advisors and brokers with volumes growing from $1.5bn to $4bn last year. In addition, SEQ provides professional services, including SMSF administration and insurance broking. FY21 financials were impressive with revenue up 37% to $116m, EBITDA up 138% to $11.5m and the balance sheet sitting with $15m net cash.  Source: SEQ company filings Management is expecting revenue growth of 15% in FY22; we estimate that this will translate to $15m EBITDA or around $10m NPATA. Management is acquisitive and has a 2025 aspiration of servicing 1,000 advisors, doubling Morrison’s clearing volumes, and acquiring further insurance broking businesses. If successful, this could see 2025 revenues of $300m+ and $40m EBITDA. Our valuation is $1.00. Disclaimer: UWL.ASX, EML.ASX, PPE.ASX, CDD.ASX, CVW.ASX, SEQ.ASX are all currently held in TAMIM Australian equities portfolios.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim