|

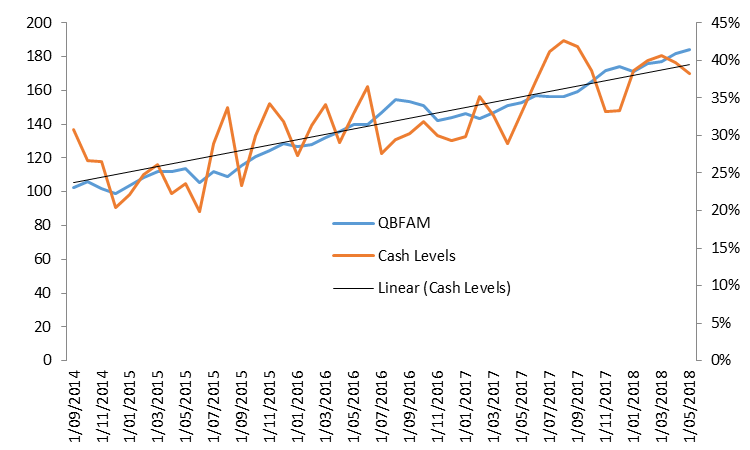

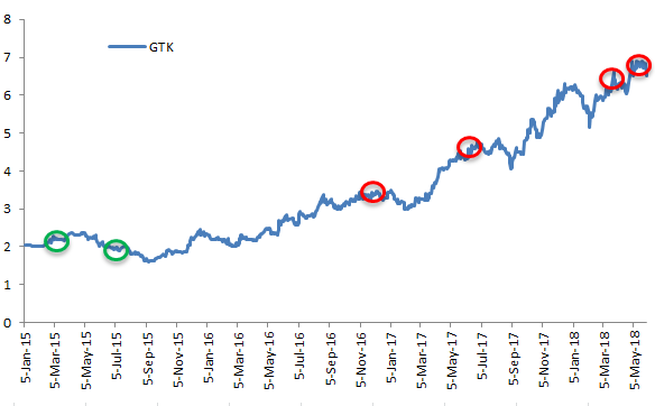

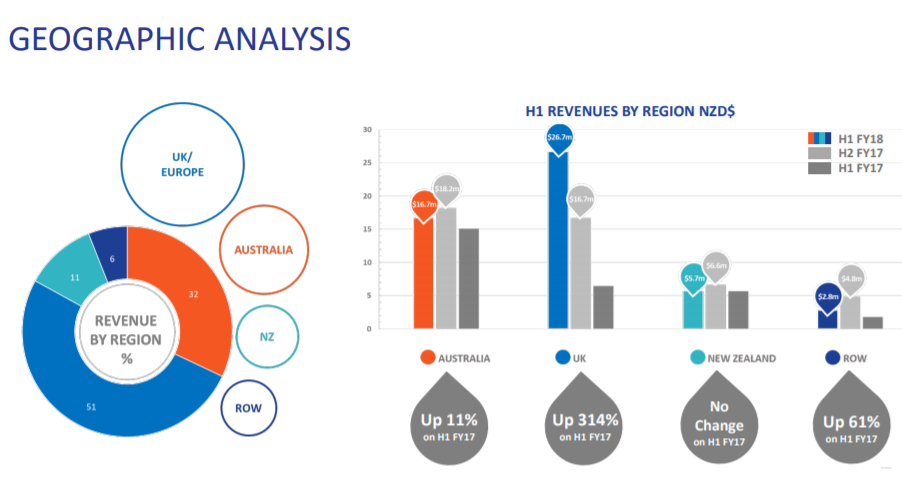

Guy Carson digs into the turnover and transition of his portfolio via the examination of six stocks. This is a must read for those interested in how to best manage a portfolio in transition. Over the last year the cash weighting in the All Cap Value portfolio has steadily risen from below 30% to 38%. Our cash has built up as we have realised or trimmed a number of positions that have done well for us. On the other side, we have added a significant number of new positions. These new positions we have taken are typically smaller, if the investment thesis plays out over time we will likely add to them. However, as of right now there are some obvious risks (why the stocks are cheap) and we are less willing to risk a significant amount of capital. The best way to describe our portfolio at the present time would be as one in transition. The below chart shows the evolution of our cash position over time compared to the overall performance of the portfolio (blue line). This shows that during periods of strong performance our cash levels tend to rise and when we find opportunities it tends to dip. Also, it is worth noting how our cash levels have risen over time as the market cycle has become more mature.  The first part of the recent transition in the portfolio has been the realisation of a number of positions that have worked well for us in recent times. We have written previously about exiting positions in Altium and IMF Bentham. Both were positions we had held for around 3 years and had done well out of. More recently we have begun to trim our holdings in two of our larger positions, Gentrack and AxsessToday. We continue to hold both Gentrack and AxsessToday but have reduced our exposure. AxsessToday (AXL.ASX) is a little different than most of our positions as it was a short term mispricing we thought we could take advantage of. We first acquired a position in September 2017 in the mid $1.50 range. It then became our 2nd largest position following a capital raising late last year. We felt the multiple at the time was significantly underestimating the FY18 growth of the company and the platform for further growth in FY19. The key to the company’s success is in its IT platform which can approve loans in 15 minutes as compared to up to four hours for competitors. In addition, the company has the ability to white label it’s finance offering for the equipment providers whilst others do not. With the shares closing last month at $2.38, we feel our initial view has been vindicated. The price appreciated last month as a number of market participants became very excited about AxsessToday and their future prospects. AxsessToday is a provider of equipment finance to small and medium sized enterprises. With the Royal Commission moving onto to business lending, the consensus view has become that the banks will start to scale back on lending and small nimble players will be able to take advantage. Whilst we agree with this view, we do believe investors are now underestimating the risk of a broad based “credit crunch”. The risk is building that we will see a regulator driven contraction in lending (most notably in the housing sector). In that scenario we don’t believe any financial companies will do well. We still continue to hold AxsessToday and believe the company to be superior to its peers . In an “Everythings OK” environment the company will continue to do well but we have moved to lock in some profits and protect our capital. Gentrack (GTK.ASX) remains our largest position but we have taken some profits in recent times. The chart below shows how we accumulated our position in the low $2 range back in 2015 (green circles represent purchases) and over time we have trimmed it (red circles indicate sales).  With the Gentrack share price closing last month at $6.61, we are currently sitting on a 45.8% IRR for our investment. Over the past few months we have trimmed our position, taking it from 8.8% of our portfolio at the end of March to 6.3% now. The reasons behind this were purely valuation based, we initiated our position at a Price to NPATA ratio of around 16x, this had has drifted up over time into the mid 20’s. We also knew that Gentrack reports at the end of May and that any slight disappointment could lead to a selloff. The end of May came and Gentrack’s result arrived. The result was solid in our view with a 50% lift in NPAT largely driven by the acquisition of Junifer Systems. Operationally the business is performing well and in a significant move they have signed two of the “Big 6” energy retailers in the UK as customers over the last six months. In fact, the UK business is now their largest region with revenue having grown by 314% over the last year. This is an industry where clients rarely change providers; hence these wins are a big deal.  Surce: GTK company filings Despite the strong result, the share price did fall 5.1% on the day. We put this down to two factors, firstly at $6.85, the share price had probably gotten ahead of itself (hence why we had reduced our position) and secondly the guidance given by the company. Management has effectively guided to a flat 2nd half, which was below consensus expectations. We do have reason to believe management are being conservative however and we can see evidence of this in the listed history of the business. When they first listed on the share market back in 2014, the company gave quite aggressive guidance and were forced to downgrade six weeks after listing. Having learnt the fickle nature of public markets the hard way, the company has since then applied a philosophy of guiding low and beating. Due to this, we believe that management have given themselves a low target and should outperform its guidance in the second half. So having taken money off the table in a number of positions, we have been scouring the market looking for new ideas. To date this year we have established four new positions. These positions are small as each has some fairly obvious risks. The four companies we have added are:

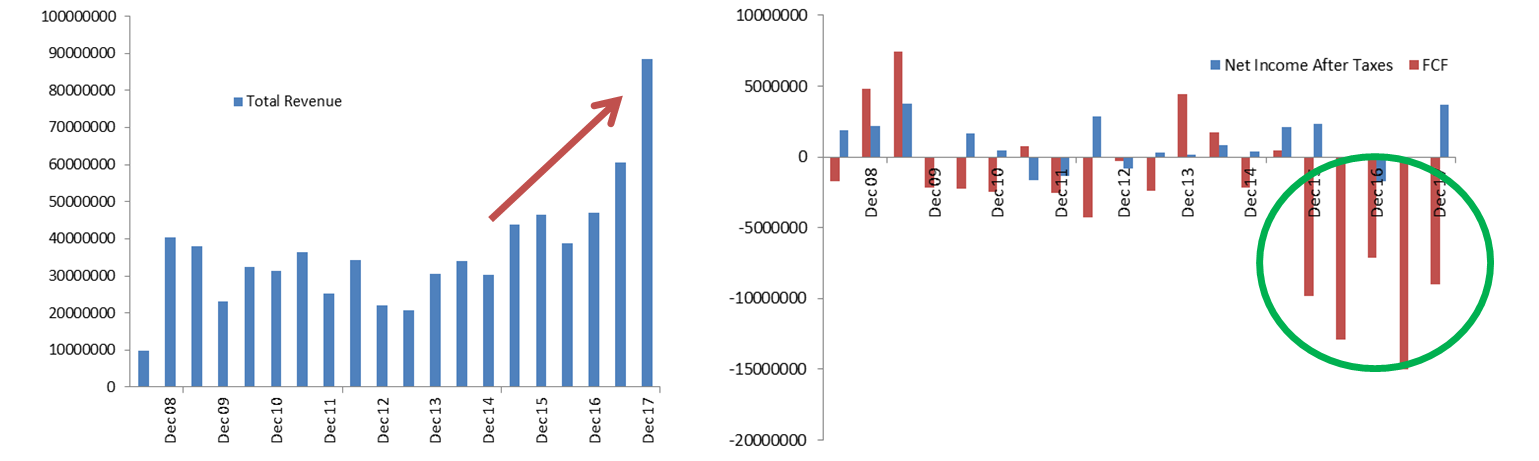

All four of these companies have significant Intellectual Property associated with a product or products. They all appear cheap on a 2-3 year view if the take up for their product meets our expectations. The reason these companies are cheap relative to similar product companies on the ASX comes down a lack of a significant track record. Effectively they are all early stage companies or have early stage products (although still profitable) and the next few years will be key in determining their success.  Source: NetComm Wireless Source: NetComm Wireless NetComm Wireless (NTC.ASX) (portfolio weight: 1.8%) NetComm Wireless is a manufacturer of products for the Telecommunications industry. The company has two main products, a Distribution Point Unit (DPU) and a Fixed Wireless Transmitter. The DPU takes a single Fibre connection and redistributes it to up to four existing copper lines. It is a pivotal component of the “Fibre to the curb” rollout for the NBN. The Fixed Wireless product is designed to provide broadband access to semi-rural areas. It provides an infrastructure grade 4G signal that can be accessed in a 13km radius. The company is in the process of rolling out this product for the NBN as well as the US for AT&T and in Canada for Bell Canada.  Source: NetComm Wireless Source: NetComm Wireless Back in 2015, the NetComm share price surged from below 50 cents to above $3. This was on the back of the agreements signed with the NBN and AT&T. The company used the elevated share price to raise capital. They raised $50m in equity in early 2016 at $2.95 a share. This capital was used to expand their R&D resources as well as their production infrastructure in order to meet the new significant orders. The company has since seen significant investment in their business (as can be seen by the green circle below). The equity raising was well timed by the company as the share price has subsequently fallen from above $3 to $1.16 now. The expected ramp up in revenue has disappointed slightly and the market has lost patience. However, to us the first half result this year showed the first impact of the NBN rollout and could be a sign of things to come. Revenue has risen steadily since 2015 but took a big jump up in the last six months. The company also swung to profitability.  Source: Thomson Reuters, NTC company filings The majority of the recent growth has come from an accelerated NBN rollout. This will underpin earnings over coming periods as well. For the DPUs, the company receives US$430 upfront. Telstra continues to own the copper wires for the next 18 months, and at the end of that period, the household must switch to the NBN. At this point NetComm receives US$120 per connection for a Network Connecting Device. On average there are 3.2 connections per DPU meaning the company receives on average US$834 per DPU over an 18 month period. With the NBN having well publicised problems recently, most notably around “Fibre to the Node” connections, “Fibre to the Curb” is set to have a bigger role. As evidence of this, NBN Co recently announced a further 440,000 premises will be covered by “Fibre to the Curb”. In addition to the NBN rollout, there are other avenues of growth. The fixed wireless rollout with AT&T is live in 18 states and is set to accelerate over the next year. They have also recently announced a fixed wireless agreement with Bell Canada, consolidating their position in North America. The company is also undertaking testing of its DPU for BT. All of this activity shows us that the company is slowly carving out a niche amongst the global telecommunications industry. The great thing about this industry is that the major players aren’t in direct competition as they typically operate just in one country. As they don’t compete, they talk and it appears word is spreading about NetComm’s abilities. We acquired a small position in the company after its most recent result which showed the significant swing to profitability. Consensus expectations have the company making $19.95m in EBITDA this year followed by $40.13m next year. At a market cap of around $180m and with no debt, the market is clearly doubting these numbers. If the company delivers on its current contracts and continues to gain traction with other tier one telecommunications companies, then the shares are well and truly undervalued. MSL Solutions (MPW.ASX) (portfolio weight: 2.5%) MSL Solutions is a global provider of Software to clients in the sport, leisure and hospitality sector. The company has over 2,000 clients across 20 different countries varied across Golf Clubs, Registered clubs, Stadia and arenas as well as other hospitality venues. The company is a recent listing and in 2017 they raised $15m to complete several acquisitions. When they listed, the company put out some aggressive assumptions for the FY18 year expecting 22% revenue growth and 62% EBITDA growth (as can be seen below). Unfortunately for shareholders, shortly after listing the company missed its FY17 EBITDA and NPATA numbers. The revenue line was as expected but the company underestimated acquisition costs and took a hit on their treatment of Employee share based payments. The result has been a share price that has fallen from a post IPO peak of 34.5 cents per share to 20 cents per share.  Source: MSL company filings The situation reminds us a little bit of Gentrack. Both are software companies that missed earnings shortly after listing. The great thing though about software companies is the business model, which typically sees:

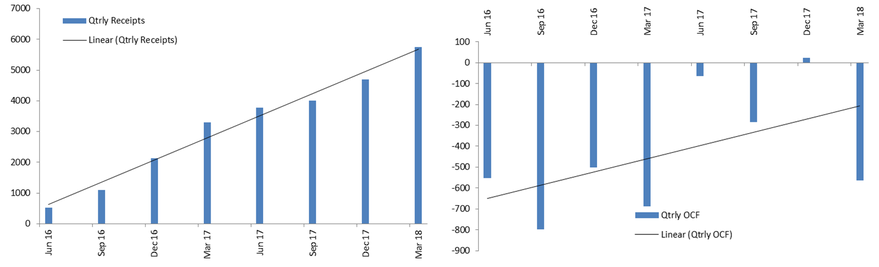

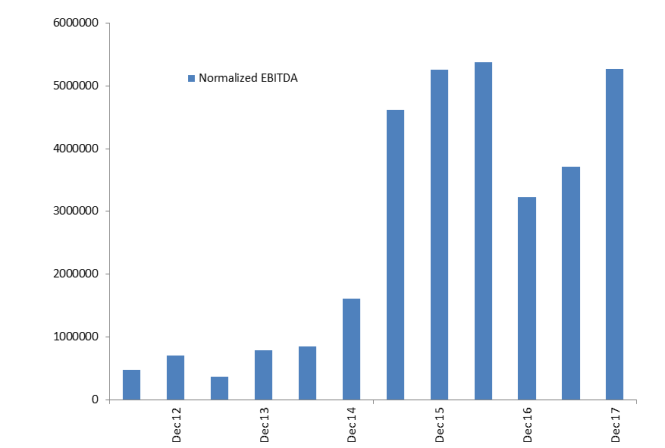

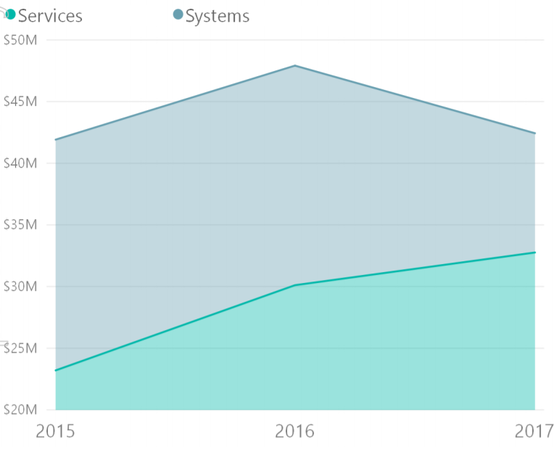

So if the problems that led to downgrade are due to one-offs or project timing then we can have some faith that things will recover. The company continues to maintain its guidance for FY18 but the market quite clearly doesn’t believe it. Based on its NPATA guidance, the stock currently trades on below 9x. In addition the balance sheet is in good shape with $7.3m in cash (no debt) and an asset called “Zuuse” which they have been selling at a price which values their stake at $6.4m. The market clearly believes they will miss their FY18 forecast and that could be true. In fact the company has already quasi-downgraded by announcing they will sell Zuuse shares to reach the guidance. However, when we step look at the business we see it moving in the right direction. The company recently provided its most impressive quarterly update as a listed company with Operating Cashflow swinging into positive territory. They also announced that they had utilised some of the excess cash to make a small acquisition. While it is early days, and our position in the company is a small one, the signs are positive. Locality Planning Energy (LPE.ASX) (portfolio weight: 1.2%) Locality Planning Energy is a Queensland based operator of embedded electricity networks. Essentially they provide energy services to strata communities. When they take on a new strata community, they install a “parent meter” in front of all the existing individual meters. As a result, a single metering and network charge now applies. In total, the company estimates they can save the residents around 20% on their electricity bills. For their trouble, Locality Planning make a gross margin of 18.2%. The company backdoor listed in January 2016 and some early hype saw the share rise, peaking at 5 cents. Since then the market has lost patience and the shares have traded down to 1.9 cents. Despite this the company has made significant process. Quarterly receipts have gone from around $500k to $5.7m and the cash burn has almost disappeared. In fact, in the December quarter the company had its first positive cashflow.  Source: Thomson Reuters, LPE company filings Typically we don’t invest in companies that don’t make a profit but in the case of Locality Planning a few things give us some comfort in the future. Firstly, the company has experienced significant take up and growth over recent years (as evidenced above), and secondly (and probably most importantly) the average contract length they have is 7.2 years. In other words, their current run rate of revenue is locked in for the next 7.2 years and all additional strata communities they add will lead to growth. It’s rare to see such a stable revenue base for a company with a market cap of $45m. With the company more or less at breakeven and still growing, we expect that additional growth over the coming years will lead to profitability and a rerating of the shares. Adacel Technologies (ADA.ASX) (portfolio weight: 1.0%) Adacel is a software company that operates within the aviation sector. They have two primary sources of revenue, their simulation software is used to train air traffic controllers (c. 58% of their revenue) and their air traffic management (ATM) software directs real world flights (c. 42% of their revenue). The ATM software is used primarily in smaller countries such as Fiji, Portugal and the French Territories. Larger countries tend to like bigger players to monitor their airspace so Adacel subcontracts to companies such as Lockheed Martin. Their Air Traffic Control simulation business is incredibly valuable though. It is the most widely used by the Federal Aviation Authority in the US. The company saw significant growth in earnings from around FY13 to FY16. More recently earnings have stagnated.  Source: Thomson Reuters, ADA company filings The reason behind this is that there is a lumpy Systems component to their revenue and that has fallen over the last few years. The ongoing services revenue has continued to grow.  Source: ADA company filings Pleasingly, 2018 will see a bounce back with Profit Before Tax expected to grow 35%. Despite this, shares in Adacel have fallen heavily in recent times. After peaking at $3.30 back in 2016, the shares have fallen to $1.71. The recent pressure on the shares has come despite the company maintaining its earnings outlook. A big part of the reason behind this is the company missed out on a contract with NASA which would have significantly increased its revenue, profit and hence value. Whilst unfortunate, we don’t think this changes the viability of the business going forward. On the current guidance the company trades on below 15x pre-tax profit. With a significant amount of tax losses accumulated, this profit should flow through to cash. We believe the current price under represents the significant amount of IP within this business.

Whilst we like all four of these companies, our positions in them are currently small. Their share prices have all been under pressure in recent times for issues that we have highlighted. At this point we see value but we do acknowledge the risk. We are well aware that as investors we will never get 100% of our buy calls right. The law of averages suggests we are wrong on at least one of the above. Therefore, to minimise the risk, we have taken small positions to start with and will build these over time if the story plays out as we anticipate.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Stock CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim