|

This week Robert Swift gets down and technical and takes a look ESG Compliance in the wake of the ongoing Hayne Royal Commission. This is a brief article and somewhat ‘geeky’. It is not directly about the Hayne Royal Commission although we will cite specific examples. It is more about Environmental Social Governance (ESG) ‘analysis’ and whether it helps investors or whether it is marketing ‘spin’; or at least ‘spin’ as currently commonly used. For those of you not living in Australia, the Royal Commission into the banks (and AMP, an insurance company) has revealed several embarrassing shortcomings and downright infraction of the regulations covering the provision of financial services. The Famous 5 to which we refer in the title, and which are currently embarrassed on a daily basis, are the 4 major banks and the AMP. It seems that shortcomings in process and incentives; ethics and the oversight of financial activities were not confined to everywhere but Australia after all. We have a proposed solution to this and it is not more regulation, we already have plenty of that. It seems that these organisations are:

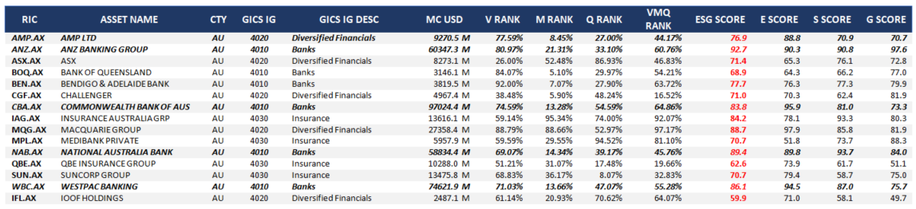

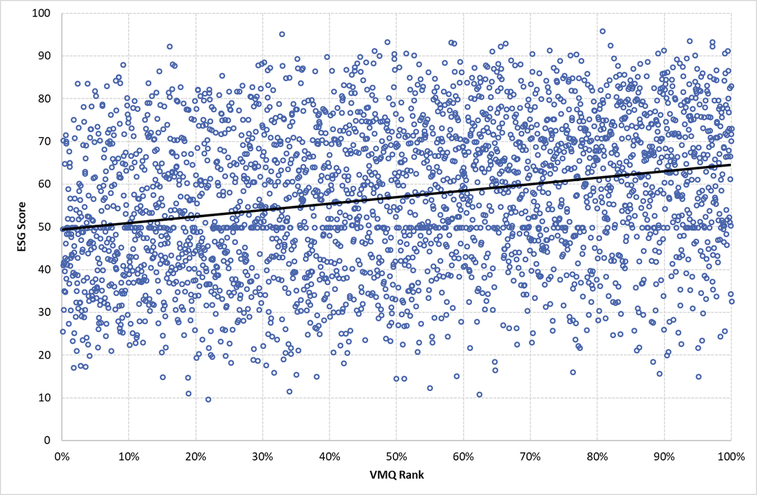

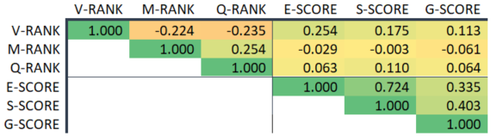

Spot the common factor. For the cynics (and oldies) amongst you we post a clip from the film Casablanca. We too are “shocked” (sic) to find that the inherent conflicts of interest in such large, complex, and vertically oriented organisations haven’t been supervised either by management; the board or the regulators. What a surprise to find that human beings working in financial services in Australia responded in the same way to the same incentives of ‘carrot and stick’ as the human beings in the same industries in the USA and the UK! So often it is not the infraction that is the problem; people everywhere are wittingly or unwittingly committing a ‘crime’. It is the (lack of) response to the infraction that is the problem. This too appears common to the ‘Anglo Saxon’ world. For more on why and how this culture has permeated listed companies then you should seek out work on executive compensation and share option incentives by Andrew Smithers. We can email you a copy if you wish? The problem with being “shocked” at revelations is that you are probably too late and the share price has fallen, or falling precipitously at a rate that makes selling the shares even more expensive to clients? If you are “shocked” then your analysis has not picked up the risk and likelihood of this ESG shortfall ahead of the revelation? You would be shocked if a company was found to be cheating on its accounts but you might admit that you didn’t dig deep enough? Why is ESG any different if it is to be called analysis? Consequently, what is the point of ESG “analysis” if it merely results in a coordinated shareholder vote of protest AFTER all the damage has been done? It’s great to vote against the board after the event but hard to see how ESG compliance provides a competitive advantage if group think is prevalent? It's great to be a signatory of the United Nations’ Principles of Responsible Investing (UNPRI) but not much practical use if you or they don’t speak up BEFORE the event? Let’s move on to the point of the article. It is not about the Australian banks nor the Australian regulators but really about ESG and whether it is effective as currently applied. ESG assessment is the ‘analysis’ of companies (and we hope governments since they issue bonds to the capital markets and take taxes) in the dimensions of Environmental Social and Governance responsibility. It is becoming increasingly important as a fund manager to have an approach to incorporate this aspect of capital stewardship. We do apply ESG in our own way, albeit with a particular emphasis on related G elements and Accounting policies rather than that of religious zealots where evil is everywhere and in everything. We highlight below the ESG scores for the ‘Famous 5’ and show in context to other Australian financial service entities we evaluate as part of our stock assessment model. These have been drawn from Thomson Reuters database and are on a scale of 0 – 100 where 0 is pretty bad. The Thomson Reuters model is a fairly rigorous assessment and evaluates over 70 dimensions to arrive at a final score. There would appear to be no warning signals within all this information. Other approaches may have been better however given that we are all “shocked” at what has recently been revealed we doubt it.  Now for the geeky bit. When we looked at the benefits of adding a new set of ESG factors to our existing model we discovered that there was positive correlation between the model and the ESG score. Having a positive exposure to the VMQ rank also meant we had a better than reasonable chance of having positive exposure to good ESG scores. In simple terms there was a positive non-trivial correlation which we show below. The XY graph shows the trend line which is reasonably positive and the spread around the trend line appears wide but actually isn’t. See us for some more geeky maths if you wish. The R-squared between the VMQ and ESG scores currently is 0.27.  In the following table of cross-sectional correlations, we show the average co-movement between the VMQ and the ESG scores. Not only are the V (Valuation) and E (Environment) scores related but the ESG scores themselves appear to duplicate each other. We have found that where V gets fooled is when G is poor and for this we always look to the accounting policies, auditing choice and board composition for further guidance and support. Some would say this is merely what used to be called sensible research – whatever.  Consequently you can be ESG compliant even without explicitly applying ESG rankings.

If you still want to have separate ESG scores from other factors you consider when selecting stocks, then here is the next conundrum. Having more factors to which you need positive exposure will increase portfolio turnover. If the ESG factors decay, that is if there is a need to keep refreshing your portfolio to get exposure to the ESG factor, you will increase turnover and transaction costs of your portfolio. If there is no decay of the ESG factor, how come it is an alpha factor to which you must have positive exposure? If it doesn’t decay over time, it’s not alpha. It is fine of course to want positive exposure to ESG considerations. Just don’t call it an alpha factor. Our conclusions in a presentation we gave at a recent conference on the practical challenges of incorporating ESG into the investment process were:

We will have to see if there are remedial actions taken by the buyside after this Commission has finished. There probably should be.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim