|

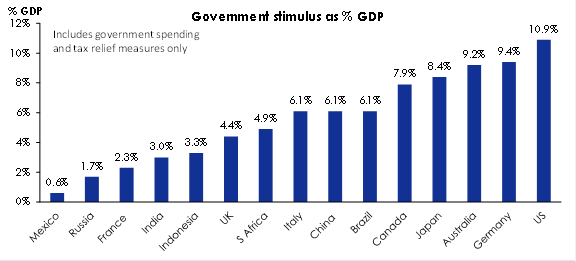

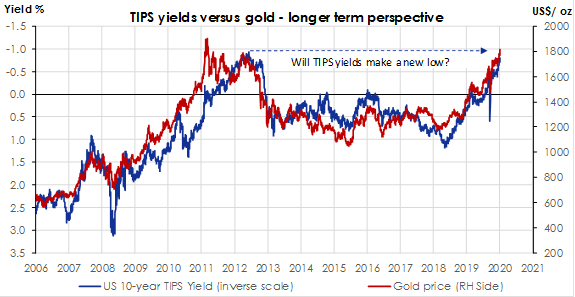

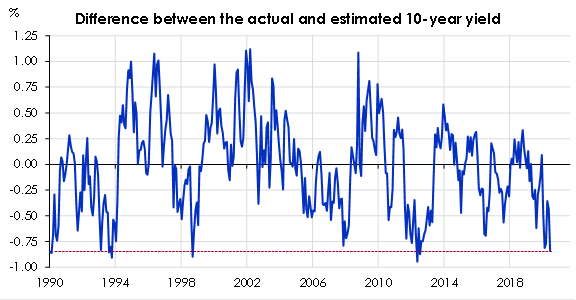

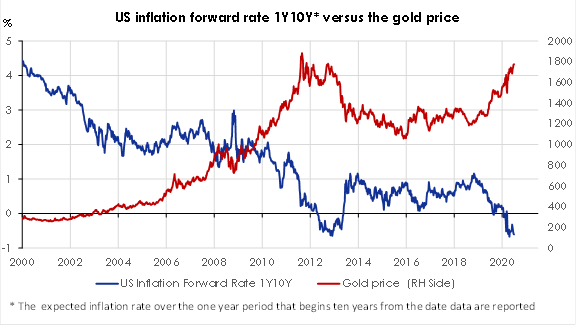

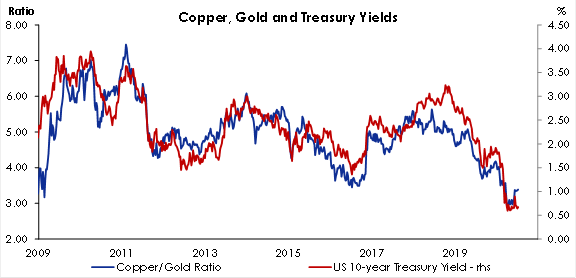

Risk assets continue the long march upward with equities higher and yield spreads lower. Is it really a dead cat bounce as some fund managers (in cash) are saying?  Author: Robert Swift Author: Robert Swift On a simple P/E ratio, equities look extended and certain sectors very much so. Our global equity strategies remained pretty much fully invested but we have reduced the exposure to cyclical stocks and have never really owned the highly rated nor loss making companies. We are not being greedy here! However, this is not 2008 where the response to the GFC was purely monetary and destined to produce little real economic growth. The Covid response has been an enormous FISCAL response which may well produce a better outcome with actual growth and of course an uptick in inflation? As equities tend to be better in mild inflationary periods than bonds, this ‘dead cat’ bounce may not be so moribund? Look at how BIG the fiscal response has been SO FAR.  Investors are rightly concerned about debt levels and ponder their continued confidence in fiat (faith based) money. The performance of Gold is telling us that investors are hedging bets against fiat money. Index Linked bonds are up in price too. They tend to move in lock step which is why we argue that a BETTER growth and inflation hedge lies elsewhere.  Source: Bloomberg If inflation (which is a deliberately targeted outcome) does become visible, then yields will be under upward pressure even as inflation arrives. If so, then Gold tends to underperform! The charts below show the pressures building on USA interest rates through the fiscal deficits; and how over valued the bond market is  Source: Bloomberg  Look more closely at the Gold and Index Linked Bond chart. It is becoming expensive as are the bonds. Gold has zero yield and it costs minus 1% to own an Index Linked bond for the privilege of receiving an inflation adjusted terminal value. This is an expensive hedge when there are better ones around. Now look at what Gold does when inflation is in the system:  Source: Bloomberg

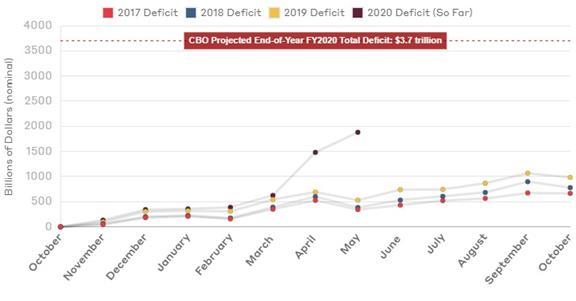

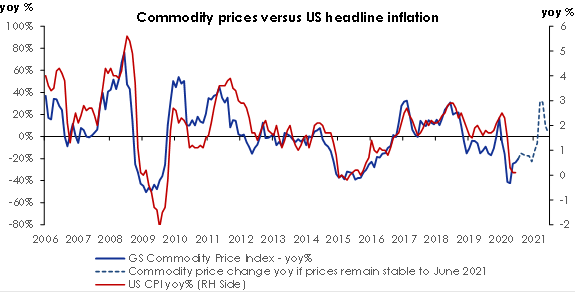

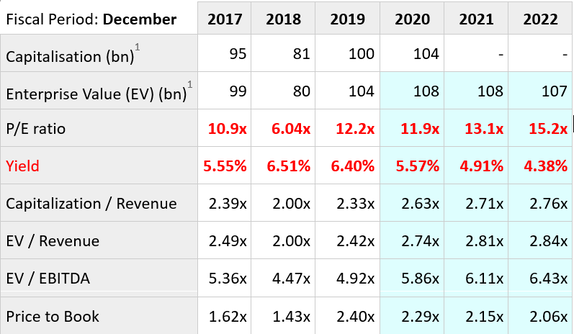

Source: Bloomberg Furthermore, inflation is going to be higher even if commodity prices DON’T rise so if normal relationships hold, we are looking at a bottom in longer term Treasury Yields, especially if more fiscal response is coming – Democrat nominee Joe Biden and President Trump are both calling for an infrastructure renewal (again) and the recent ‘recovery fund’ deal in Europe would indicate this is highly likely to occur elsewhere.  Source: Bloomberg We ARE at a crossroad, where the imbalances have to be resolved rather than allowed to get bigger. So, the risk markets will become jittery from time to time and inflation will re-appear and be welcomed! Rather than forfeit any yield and own a less than perfect hedge, a sensible strategy would be to invest in base materials companies in the expectation that their volumes and pricing recover with these fiscal programmes. One of the more attractive companies in our modelling work is highlighted below.  Strengths: Margins returned by the company are among the highest on the stock exchange list. Its core activity clears big profits. The company is in a robust financial situation considering its net cash and margin position. The company's attractive earnings multiples are brought to light by a P/E ratio at 9.43 for the current year. This company will be of major interest to investors in search of a high dividend stock. Analysts have consistently raised their revenue expectations for the company, which provides good prospects for the current and next years in terms of revenue growth. Over the last seven days, analysts have been revising upwards their EPS estimates for the company. For the last few months, EPS revisions have remained quite promising. Analysts now anticipate higher profitability levels than before. What is the stock?! Take a guess in the comments! We leave you with one horrible thought. If this descent from over indebtedness produces poor policy choices and outright monetisation of the deficits, then we fear inflation, no growth, and financial repression such as capital and dividend controls. This will be a return to the stagflation of the 1970’s. For those of you who don’t remember the 1970’s, we include the picture below.  Source: JC Penney

1 Comment

John Dakin

4/8/2020 06:19:16 pm

Is it Fortescue ? Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim