|

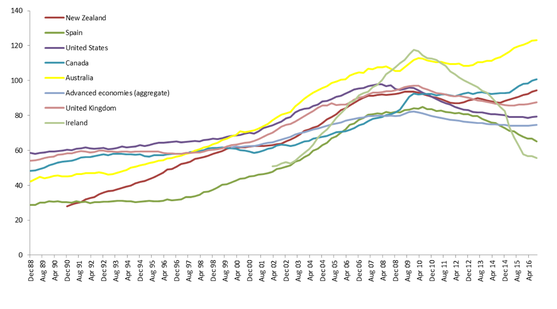

This article by Guy Carson was originally published in the Weekend Wealth section of The Australian under the title "Time to plan for recession as household debt crimps spending" Back in 2007, a US economist called Edward E. Leemer published a paper entitled “Housing IS the business cycle”. In this paper he studied the causes of every US recession since World War 2, of which there had been 10. What he discovered was that 8 out of the 10 were preceded by substantial problems in housing and consumer durables.” The only two US recessions that are exceptions to the above were the end of the Korean War in 1953, caused by a decline in defence spending, and the 2001 “Tech Wreck”. As the paper was written in 2007, we can now improve the success ratio to 9 out of the last 11 recessions following the 2008 recession, something that Leemer warned about. When one reads this paper and looks at the current economic environment in Australia, it is hard not to get nervous. Recently, the retail sector has seen a significant selloff and whilst many observers point the finger squarely at Amazon, we believe there might be more at play. As a case in point, the recent downgrades from the two largest car retailers in Australia (AP Eagers and Automotive Holdings Group) tell an interesting story. As far as I’m aware Amazon does not sell cars and yet sales on a national level are falling. What is causing this? Well, Australia has the second most indebted consumer in the world behind only Switzerland with respect to Household debt to GDP (chart below). The rise in household debt in this country has pushed the level above what was seen in places like Ireland and Spain prior to the Global Financial Crisis. Recent out of cycle interest rate hikes from the banks combined with record low wage growth has put significant pressure on this highly leveraged position.  Source: Bank of International Settlements High debt levels mean the consumer is highly sensitive to small changes like we have recently seen. As a consequence we have seen a fall in car sales on a national basis led by falls in Western Australia and Queensland. AP Eagers indicated that sales were impacted by a 5.9% fall in Queensland whilst Automotive Holdings stated that a 3% fall on the east coast had “reduced the capacity of east coast earnings to provide cover for WA”.

In addition to falling car sales we had construction data out for the first quarter of 2017 and we had the first signs of the residential construction boom slowing. The fall in residential construction for the quarter was 4.7% and was the largest such fall in over 15 years. The fall was driven by a 14% fall in Queensland and whilst this was potentially cyclone impacted, the increasingly oversupplied Brisbane apartment market appears to be having an impact. This fall in residential construction combined with sharply falling car sales ticks both of Leemer’s boxes and suggests Queensland may well be joining Western Australia in a recession. Whilst problems are evident in Queensland and WA, it is probably too early to have the same concerns for NSW and Victoria but the overall economic outlook is slowing. So with that in mind how should one position portfolios? Well, for starters are a long list of companies and sectors to avoid. The three stand out to us as most vulnerable are:

The question becomes where to hide. If we do have a recession, very few stocks will do well. In order to avoid cyclical weakness it is important to look for industries that are going through structural change. The three most obvious examples to us are:

The current consumer strike is sounding warning bells to us. The economies in Western Australia and Queensland appear to be in or heading for recession, it’s only NSW and Victoria (or more accurately Sydney and Melbourne) that are holding the economy up. Whilst we have no perfect insight in the future, we believe that now is the time to be selective with your investments. DISCLAIMER: Guy’s portfolio currently includes the following stocks mentioned above: Altium (ALU.ASX), Gentrack (GTK.ASX), Hansen Technologies (HSN.ASX), Integrated Research (IRI.ASX), CSL (CSL.ASX), ResMed (RMD.ASX), IMF Bentham (IMF.ASX).

6 Comments

john pearce

15/6/2017 04:46:13 pm

interesting reading - enjoyed

john pearce

26/6/2017 05:10:34 pm

very useful discussion - I regret Tamim is only for wholesale investors

Jeff Jamieson

11/1/2018 04:47:48 pm

Poorer Retail performance is also impacted by the large number of new entries coming into Australia while the market size overall is not growing. Meaning less sales per retail company.

Guy Carson

15/1/2018 08:07:22 am

Absolutely agree Jeff. The entrance of low cost international players has and will continue to impact the Australian retail space. That combined with stretched household balance sheets and sluggish retail sales is not a great combination. A side impact of the increased competition has been price deflation which has also weighed on the inflation numbers. The RBA has cited low inflation as a key reason for record low interest rates, but the above scenario is really outside the scope of their influence.

Euclid D'Souza

12/1/2018 07:52:34 am

Hi Guy. Thanks for a well balanced article. However, in a recession I would expect, at a superficial level, companies like Credit Corp and Pioneer Credit involved in purchase and restructure of debt ledgers to benefit from an increase in distressed borrowers. Would appreciate your reasons for saying that these companies are vulnerable to a down turn.

Guy Carson

15/1/2018 08:18:00 am

Hi Euclid, I actually agree with your statement but it comes down to timing. These finance companies are buying high risk loan portfolios at a discount. There is the risk that if we do have a significant recession that the default rates in the portfolios exceed the companies modelling and puts their earnings and future at risk. In previous credit crunches the market has typically taken the shoot first and ask questions later approach. In addition, if default rates rise higher than expected not all of these small finance companies will survive. Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim