|

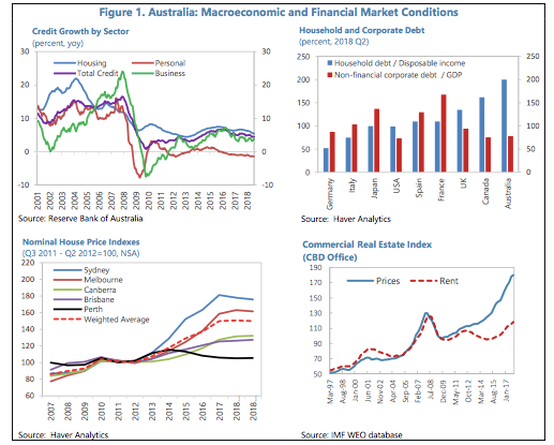

This week we would like to revisit the topic of the Australian banks in the wake of the Royal Commission. It seems that the markets have shrugged off the doom and gloom with bank-bashing relatively out of vogue in the mainstream media. Indeed, CBA has finished, at the time of writing, with its share price back to the pre-Royal Commission days. This brings us to the question, where to from here? We would like to answer this from two perspectives, the first of risk and the second reward (bearing in mind the opportunity cost).  Risk & Reward In a recent conversation with a fellow investor, we were referred to an interesting character by the name Anil Gaba, who happens to be a professor of risk management at INSEAD. The professor categorized risk in two ways, subways and coconuts. Basically, the idea is that you can do research and be reasonably sure that a subway will be predictable most of the time. On the other hand, you know that a coconut will fall from trees, but you cannot predict when it will fall or where it will land. Hence once you can accept the second form of risk, it follows that diversification will be key. When looking at the banks as businesses, let us assess the subway risk first. From a bank's perspective, we are talking about what will be more intuitive. Things that we are more easily able to calculate such as capital adequacy, liquidity, asset quality etc. Here we can give credit where it's due and kudos to the regulators, Australian banks remain some of the most well-capitalised in the world. The regulatory capital ratio remains at 14.2% with the D-SIB’s (Domestic Systemically Important Banks i.e. Big 4) being further required pay a 1% surcharge to keep their Capital Conservation Buffer above 3.5%. In addition, the average asset quality of the banks remains relatively high and with further steps being taken to limit the extent of interest only loans it would be reasonable to expect that this will remain so well into the future. Nonperforming loans (NPL) also remain low. Though the extent to which this has been a self-fulfilling prophecy is something we shall leave for the reader to judge. We have had a bull market in residential property for twenty years and therefore it would be fairly hard to see how we would have had anything other than a low NPL ratio. The only way to judge the effectiveness of a banks credit control processes is for it to actually go through a crisis. This brings us to our first major coconut which is that while NPL’s remain low, provisioning, as a result, is also rather low. To quote the IMF, “Provisions are about 40% of NPLs, which might appear modest, but reflect low historical loan loss rates, loan portfolios that are mainly secured against collateral (with unsecured consumer loans comprising less than 4% of the total).” This means that should there be even slight increases in the percentage of NPL’s, then the hit to profit margins and therefore share prices (one would assume) would be amplified. Another way to put this is that they have an excellent ability and track record of managing their bad debt recognition. Banks are, after all, highly leveraged animals that are very cyclical in nature. One of the biggest misnomers is that banks are fairly good defensive assets, this cannot be further from the truth. Banks in Australia (and Canada) performed so well through the GFC because of the nature of their asset exposure. By and large, Australian banks are not diversified businesses, rather, residential mortgages make up over half the books (a third of which are interest only by the way) and commercial real estate about 10%. In fact, most non-financial corporate debt in Australia is financed primarily by non-residents (including real estate & infrastructure companies). This essentially means that taking a position in the bank is in and of itself a bet on the housing market, in a highly competitive environment. Believe it or not, this is the case. The nature of their business means that they are essentially serving a relatively standardised and commoditised product (a residential loan) that cannot be differentiated apart from price (i.e. interest). Their moves into adjacent categories to provide the value-add has been disastrous (for those of you who have just returned from Mars we are of course referring to the ventures into Wealth and Superannuation). With disintermediation and technology disrupting financial services further (i.e. p2p lending platforms, trade finance and fintech) it is very likely that they will be relegated to becoming simply wholesale providers of balance-sheets. Indeed this seems to be already happening with most of the major banks now looking inwards and honing/doubling down on their residential exposures.  As can be seen in the chart above the bank’s long-term profitability will simply be a function of net-interest margins which continue to have downward pressure and volume growth (there is your second subway). With Australian households the most indebted already, we don’t see substantial catalysts here as we did during the ramp up in immigration from 2005 onwards combined with residential price growth of 70% in the last 10 years. This is not to say that they won't be profitable or their cash flows disappear, we are just suggesting that the future will not be as bright as the past. Their future profitability will also be contingent on liquidity in global wholesale markets. This is perhaps the biggest coconut in that, despite regulatory pressure, one third of bank liabilities are through wholesale markets and two thirds of this is via international sources. While some of this risk has been mitigated by longer duration and prudent use of currency swaps to hedge out currency exposure, this remains concerning since they are not able to finance their continued expansion through domestic markets. This means that the Big 4 banks are domestic banks with international liabilities.  So, coming back to the question of risk vs. reward, while banks still look to be fair value to us from both a P/E and P/B perspective, we don’t think there is a clear and compelling case for further momentum. Unless of course, you believe that somehow banks could triple their mortgage books over the next decade (as they did over the past decade). We think that buying a property in (especially given the low interest rate environment) gives about the same amount of exposure and potentially a greater reward (if one is a relatively discerning investor).

Granted the continued access to Franking Credits and their relatively greater liquidity does make them a more attractive proposition than would otherwise be the case. In addition, there is also the notion of the government put which we’ve previously talked about, the regulatory regime in Australia and globally means that, as “systemically important” animals, some of their risk is publicised while the dividends (hence profits) are privatised. Conclusion - A decent subway but two too many coconuts.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim