|

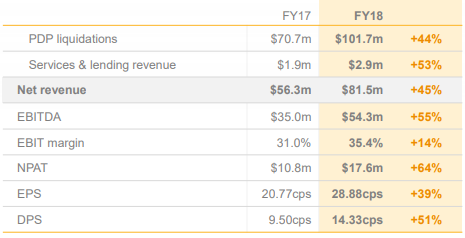

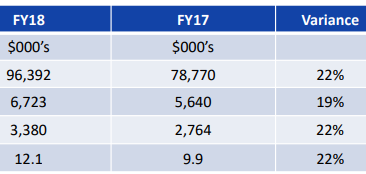

The Small Cap team take a detailed look at some of the movers, both positive and negative, in their portfolio this reporting season. Pioneer Credit Limited (ASX: PNC) Revenue +45% NPAT + 64% EPS +39% Dividend +51% (August return: +7%) Debt purchaser PNC delivered another impressive result with substantial improvements recorded across all key metrics. In particular, strong delivery on its key metric – Purchased Debt Portfolio liquidations, saw PNC collect $102m for the year (up from $71m in FY17), and provide guidance of $120m for FY19. The strong level of collections resulted in a 64% increase in profit after tax.  Source: Company filings Entering FY19, PNC has significant momentum with another solid year of purchases forecast, and PNC’s new personal loan division, Credit Connect, continuing to target a $30m loan book by December 2018. We see upside to PNC’s guided level of purchases and NPAT, and believe the market is likely to reward PNC with further share price increases when it sees earnings emerging from its loan book - which would indicate that PNC’s diversification strategy is taking shape. Blackwall Ltd (ASX: BWF) Revenue +49% NPAT + 125% EPS +125% Dividend +12% (August return: -10%) Blackwall, the property fund manager and manager of the WOTSO co-working business, reported a 125% increase in profit after tax, after recognizing a significant performance fee during the period.

BWF’s fast growing shared workspace business, WOTSO, showed very strong growth with turnover up an impressive 54%. Annualized WOTSO turnover today is tracking at $13.4m (up from $8.4m six months ago), with the existing 14 sites having the potential when mature to generate turnover of over $30m. While it can take up to 3 years for a new WOTSO location to achieve economic maturity, margins at this point are generally more than 25%, suggesting a long runway of significant revenue and margin growth from here. BWF continues to progress the global expansion of WOTSO with two sites due to open in Malaysia later this year. BWF also noted that the take up at Chermside Westfield has been faster than any new site so far, suggesting further partnerships with Westfield may be on the agenda. With net tangible assets of 49 cents per share, BWF has over half its market capitalisation supported by its on-balance sheet investments, with the implied total value of its profitable WOTSO, funds management and property management businesses currently sitting at around $25m. Significant value remains to be unlocked here, particularly in relation to WOTSO. CML Group (ASX:CGR) Revenue +17% NPATA +71% EPS +31% (underlying) (August return: -8%) CGR provides invoice and equipment finance to Australian SMEs through the brand ‘Cashflow Finance’. It is the number two player in invoice factoring after Scottish Pacific. CGR beat its FY18 guidance, delivering a 71% increase in underlying net profit after tax, and upgraded its FY19 guidance from $19.5m to $20-21m. They business had a very strong year with growth from acquisition and organically with 17% growth in invoices purchased.

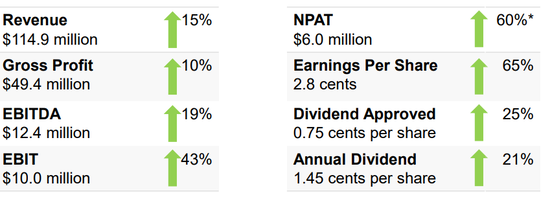

Source: Company filings We met with management post the result to understand their equipment finance strategy and get comfort around their provisioning in light of recent disclosures by Access Today. On both counts we were impressed with their conservatism in provisioning and lending. Any equipment being lent on is being independently valued reducing the risk of loss in the case of default. The outlook provided by management is also conservative and we expect upgrades to those the forecasts as any organic growth has not been factored in. Pleasingly the invoice factoring market has been growing and we expect this to continue in FY19. Legend Corporation (ASX:LGD) Revenue +15% NPAT +60% EPS +65% Div +21% (August return: +17%) Legend provides consumables, tools and equipment for electrical projects, and reported a strong result, increasing its NPAT by 60% to $6m (eps of 2.8c) beating its previous guidance and our expectations.  Source: Company filings A highlight for us was the organic growth across all divisions. As expected, and one of the key reasons for investing in Legend, the result was driven by the Electrical, Power and Infrastructure division which is leveraging the strong East Coast infrastructure spending. LGD’s recent acquisition of Celemetrix did not materially contribute to the result due acquisition and integration costs but is expected to contribute an additional $2m+ in earnings in FY19. With continued growth in the core business and contribution from Celemetrix, we expect a strong FY19 result. Even after rallying after the result, we estimate Legend is trading on a PE ratio of less than 7x FY19 NPAT. Legend is under-owned by institutions. We expect further acquisitions in FY19 which should add to LGD’s revenue diversification and may bring institutional interest to the register and PE multiple expansion. People Infrastructure (ASX:PPE) Revenue +14% NPATA +35% EPS +34% (underlying) (August return: +26%) People Infrastructure provides contracted staffing solutions to its clients, with a focus on high growth sectors where labour is in demand – including childcare, healthcare and disability sector.

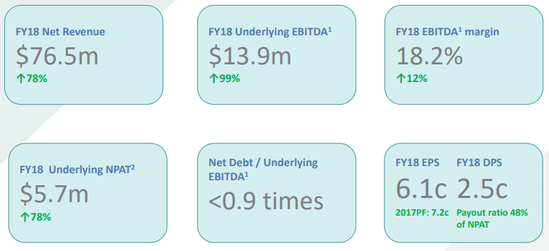

Source: Company filings Pleasingly, PPE exceeded its IPO forecasts and broker expectations, delivering a 35% increase in NPATA to $8.4m, and strong pre-tax (and IPO costs) operating cash flows of $9.5m Earlier in the month, the company acquired a leading NSW Nursing Agency on ~3.5x, providing eps accretive and defensive earnings. PPE is now the largest provider of community services employees in Australia and is the largest provider of nurses in the Sydney market. Whilst the stock has performed strongly since its IPO last November, we still see upside as the company grows organically and through acquisition. With a strong base in Queensland, the company is leveraging its customer relationships to expand into new territories. This has been especially evident with its expansion into NZ. Zenitas Healthcare Ltd (ASX: ZNT) Revenue +78% EBITDA +99% NPAT +78% Maiden dividend declared (August return: +28%) Zenitas continues to execute on its organic and acquisition growth strategy to become a significant national provider of community healthcare services. Consistent with its recent guidance, ZNT delivered a strong result with a 78% increase in NPAT to $5.7m.  Source: Company filings Zenitas highlighted a number of key operational developments to support the ongoing growth of the business. A key focus has been on building out a strong senior management team with the appointment of a COO and senior marketing, IT and HR management. Notwithstanding this investment, organic EBITDA growth of 7.3%, was achieved, and clinics in the ZNT group were up to 70 (from 50 in FY17) and clinicians and care providers increased from 1600 to 2600. As mentioned above, ZNT also announced it was subject to a $1.46 takeover offer from a private-equity led consortium. We believe that the offer as it stands undervalues ZNT, and note that two current ZNT directors are associated with the bidding consortium. Konekt Limited (ASX:KKT) Revenue +67% EBITDA +56% NPATA + 65% EPSA +20% DPS +33% (August return: +6%) KKT, a leading provider of workplace injury management and employment services, reported a 65% increase in NPATA, aided by the FY18 contribution from its employment services acquisition Mission Providence (now known as Konekt Employment).  Source: Company filings KKT delivered a result in the middle of its revised guidance range provided in April, which was helpful in rebuilding some confidence after its surprise downgrade. In line with previous commentary, KKT’s underlying business contracted, with reform in the NSW workers’ compensation market reducing volumes. The Konekt Employment acquisition has proceeded smoothly, with business performing well and in line with expectations. Growth in FY19 will be driven by the 12-month Konekt Employment revenue contribution, property synergies partially offset by labour cost increases, investment in DES establishment and property inflation. The market will now be focused on KKT’s business update at its November AGM, and the announcement in relation to the results of the re-tender of its ADF/Medibank contract. Positive news here will help to further rebuild confidence in the stock and potentially lead to takeover interest. SRG Global Limited (ASX: GCS) Note: GCS and SRG merged in late August Revenue +13% EBITDA +49% EPS +41% Dividend – 7% International engineering and mining contractor SRG reported at the upper-end of its EBITDA guidance, delivering a result of $19.4m vs a forecast range of $18 – $20m.

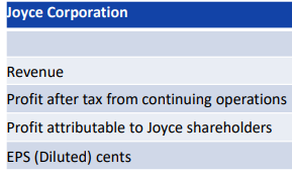

Source: Company filings Work in hand for FY19 of $218m (compared to $160m in pcp) reflects growing revenues into FY19. SRG’s international opportunity pipeline was $600m (compared to $120m in pcp) reflecting the investment into growing SRG’s international operations in FY18. This international strategy that leverages SRG’s specialty expertise in dam and bridge engineering is one of the key reasons for our investment in SRG. While international revenue was up 173% in FY18, albeit off a low base, it is too early to say to judge as to whether this strategy will bear fruit. Now that SRG has merged with GCS, the results of GCS are equally important in determining the prospects of the group. Pleasingly, GCS beat its profit guidance and updated the market with strong work in hand. GCS has already announced 2 contracts where SRG has been subcontracted to perform part of the work, suggesting there are some legitimate revenue synergies from the merger. The share price performance has been weak since the merger announcement, which we believe is due to disaffected shareholders on both the GCS and SRG register exiting. Joyce Corp Limited (ASX: JYC) Revenue +22% NPAT +19% EPS +22% (August return: +4%) Joyce Corporation, an investment company that owns the Bedshed franchise, Australia’s largest kitchen renovation company and a leading online auction company, reported a strong operating result with a 22% increase in NPAT, while net operating cash was $9.1m, up 70%.

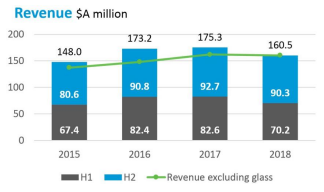

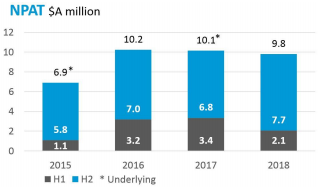

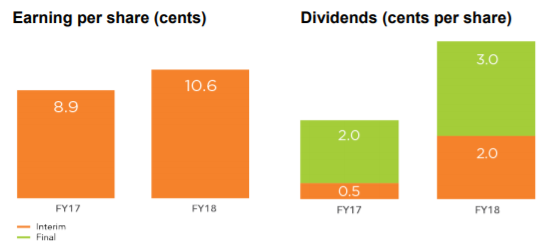

Source: Company filings JYC’s renovation business, KWB, delivered a stand-out result with same store sales growth up 12%, total revenue up 27% to $60m and profit up 40% to $8.4m. In addition to KWB’s core kitchen business, flooring and wardrobe categories are now contributing material revenue. On the back of favourable macroeconomic settings, double digit earnings growth is again forecast for this year. JYC’s online auction business, Lloyds Online grew overall auction turn over by 27% year on year, with growth in niche categories such as classic cars and fine arts offsetting reduced insolvency liquidation activity. Lloyds continued to re-invest in the development of its systems and IT infrastructure to ensure long term sustainable growth. JYC’s smallest unit, Bedshed delivered solid growth with a 44% increase in profit contribution. JYC trades on an 8% fully franked yield and has forecast growth across all its business units in FY19, to build on its strong track record of growth that it has delivered over the past five years. We expect the recent appointment of a COO to drive further organic and acquisition opportunities as well as improved disclosure/communication to the market – which should be positive for the JYC share price. Gale Pacific Ltd (ASX: GAP) Revenue -6% NPAT -3% EPS -flat Dividend - flat (August return: +3%) A record half of profit in H2 ($7.7m) from shade sale and fabric manufacturer and distributor Gale Pacific, was not enough to make up for a poor first half - as a result GAP reported flat EPS growth for FY18.

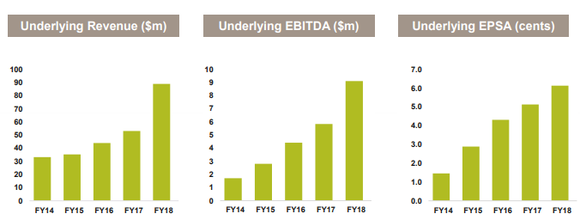

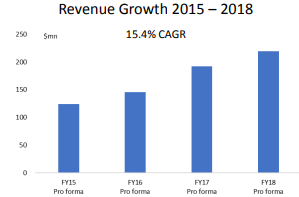

Source: Company filings As illustrated above, GAP has delivered no earnings growth over the last three years. Ordinarily, in such circumstances, we would be sellers. However, we continue to hold as we believe the underwhelming recent results mask some significant progress within the business: the exit of a number of non-core product lines with the core product focus now delivering meaningful cost savings, significant investment and progress in US growth (12 times the size of the Australia market), and China manufacturing efficiencies & service improvements. While the poor grain harvest will again impact sales of commercial fabrics in FY19, sales to the US are getting strong traction. GAP offers a market leading product, a global distribution network, including selling into all major US hardware stores and a strong Amazon presence, state of the art Chinese manufacturing facilities, and a growing R&D capability. At less than 10x FY18 net earnings, we consider this a compelling opportunity, and see GAP as a genuine private equity target given its current valuation. Apollo Tourism (ASX: ATL) Revenue +107% EPS +19% Dividend +100% (August return: -4%) Apollo Tourism is a Campervan rental and retailer. Its operations span Australasia, North America, and more recently, Europe. The FY18 underlying NPAT result came in above markets expectations with impressive 19% eps growth. However, the stock was sold off on the results due to concerns over ATL’s rising debt levels. While ATL has no net corporate debt, the rising debt levels associated with the fleet (owed to the OEM’s of the vehicles) are reflective of the increased investment to support growth initiatives. It is important to note that the debt is more than underpinned by its fleet assets. Geographical expansion continues with expansion into Germany. As always, the company will be leveraging local management from the recent acquisition of Camperco to help with the rollout in Europe. The company is experiencing strong forward bookings across all geographies going into FY19. We suspect the forward guidance provided by management is conservative and upgrades can be expected. Luke Trouchet (CEO) and Karl Trouchet (CFO) collectively own more than 50% of the company. Their shares come out of escrow later this year. During a post-result meeting they expressed full confidence in the company’s progress and committed to hold onto their shares after the escrow period and participating in the upcoming dividend reinvestment plan.

Source: Company filings Paragon Care (ASX:PGC) Revenue +16.5% EPS -38% Dividend + 3% (August return: -9%) Medical products and consumable distributors Paragon Care reported a disappointing result. While the headline numbers read well, the EBITDA numbers were inflated by a non-operating adjustment for $4m meaning the company missed its guidance. This was due to a weak last quarter in its capital equipment division as a result of a lack of large hospital projects. PGC also announced that it had placed 45.2m shares at $0.91 per share to a Hong Kong based entity, China Pioneer, giving it a blocking stake of 15% in PGC. The funds will be used to acquire to new businesses in FY19. In FY19 the company is forecasting a strong up lift in EBITDA to $36m (which was in line with consensus estimates). This includes the full year contributions from acquisitions in FY18, cost synergies, and organic growth. The flagged acquisitions are likely to add an additional $7m to $8m in earnings. The lumpiness in revenues driven by large capital equipment sales is expected to reduce as they become a smaller part of the business. Management has announced a new aspirational target of $500m in revenue, and If management can continue to execute on strategy, it is likely to become a much larger company. PGC is another holding that represents a likely potential takeover target. We note that the Paragon result highlights the importance of undertaking detailed analysis of the accounts and not just relying on company presentations.   Source: Company filings

1 Comment

Bronte DUFFY

21/11/2018 05:28:04 pm

I have added to my holding of PNC, encouraged by your positive review. Will they be affected by the up-coming Senate enquiry covering " debt management firms, debt negotiators, credit repair agencies and personal budgeting services "? Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim