|

This week we revisit a topic we first spoke of when the great Trump Trade War was very much in its infancy. That is the future of global trade and industry and, more importantly, what this means for Australia. The recent moves made by regulators in the US (including blocking off of Tencent and forced sale of TikTok) have brought many of our broader predictions, perhaps unfortunately, to a reality.

This morning the potential for the imposition of import duties on Australian wine by China has made it incumbent upon our government to formulate nuanced policy in an increasingly hostile and uncertain world. What does this mean for Australian investments? What is our world likely to look like over the next decade? These are the fundamental questions we seek to answer this week.

A wee bit of context

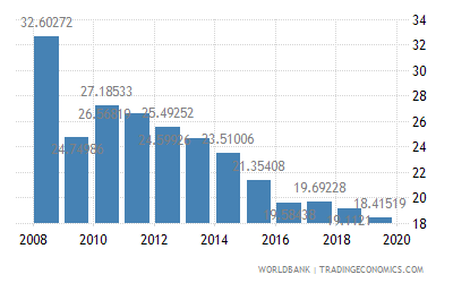

(We'll get to our title later). Let’s begin with the Chinese context. When the US first imposed tariffs on China, it seemed like a rather rational move given the leadup and what seemed like an uneven playing field for American business. The hawks however, including Pompeo, might have miscalculated and we say so because of the below graph, which shows the percentage of overall Chinese GDP that is made up of exports.

Source: Trading Economics

Author: Sid Ruttala Author: Sid Ruttala

China’s reliance on exports has been decreasing at a rapid pace since 2008, now making up less than 14% of overall GDP (the graph shows it as 18% but it has declined even further). This is perhaps the reason why growth continues to surprise on the upside despite the re-building of trade barriers within the global context. So much so that the domestic market is now a substantial buffer, enough to mitigate any losses stemming from American exports. Believe it or not, the best performing index this year was the Shenzhen composite (not the Nasdaq as you might have thought).

This context allows an increasingly hawkish CCP under Xi Jinping, with his freshly minted powers, to have a rather blasé approach to foreign policy and even internally. The new economic model of China is Xiaonomics which allows the partial privatization of previously state-owned enterprises, de-regulation of consumer facing industries combined with an overall tightening of party control over economic decision-making. And so, while Tencent might be a private enterprise, their ability to do business is contingent upon making their products, such as WeChat, effectively under the control of the State when required to do so. Under Xi, the west has perhaps been forced to realise an outcome that wasn’t factored into the calculus when it first allowed China into the WTO. In her exuberance after the fall of the Berlin Wall, the thought process was very much that China would become increasingly like Hong Kong or go through the same process as her counterparts in South Korea, Taiwan and much of SouthEast Asia (from authoritarian modes of government to democracy). What wasn’t factored in was the possibility that things might go in the opposite direction... That the largest economic expansion in modern history might give its leaders enough ammunition to not only export the national goods but also the national governance formula across the planet. Unprecedented economic expansion as a justification for the merits of the status quo/incumbent regime, if you will. Trump has borrowed the rhetoric but has lacked the data to truly back it up (sorry Mr President, the stock market is not the economy). The Belt and Road is probably a sign of more to come too, with many nations across Central Asia and North Africa, also including Pacific islands closer to home, becoming indebted to and reliant upon the Chinese for their own growth. This comes at precisely the time when the US is going in the opposite direction. Increasingly inward looking, undermining the very institutions that she helped create in the last century and which ensured her dominance as a superpower. The last-ditch effort in our region was in the form of the TPP (Transpacific Partnership) which would have fundamentally reduced the reliance on China by the over thirty signatories. The withdrawal from even non-binding deals such as the Paris Climate Agreement has created a vacuum in the global leadership which China is increasingly wanting to fill. The damage is irrevocable, every administration for the last two centuries has ensured at least the semblance of continuity from the previous. Even the EU are no longer willing to trust that an agreement made on an “America First” basis is in their best interests. Unfortunately, if the “leader of the free world” puts itself first, then others could just as well follow suit. Nationalism would be okay if it was unidirectional, it isn’t. The Chinese could be just as nationalistic, so could the Indians, or anyone else for that matter. The problem is that, come November, even if the polls are right and there is a change in administration, no nation is going to be able to trust that an agreement made can be kept once the next administration comes along. (Don’t get me started on the disconnect between the incentive of short election cycles in politics with long-term forward thinking). Unlike individuals, states cannot afford to be temperamental. In economics and political science this is called path dependence. The unfortunate circumstance is that many smaller nations across the planet look toward leadership alternatives and as the saying goes, rather the devil you know... So, while they might not necessarily like making deals with the Chinese regime, at least they know what they’re getting and the agenda won’t change on a whim.

So where does that leave Australia?

Here is the thing, this country has always managed to rely on the other side of the Atlantic to be our largest investor and for security while treading a fine line with our largest trading partner up North. No longer is this likely to be the case, there has always been an imbalance in both relationships. Remember how long it took the then recent administration to even do us the courtesy of posting an ambassador to Canberra? While America might play a big role in our political psyche, unfortunately the relationship is not reciprocal. Never has been and definitely now less than ever. From a security and defence perspective the Five Eyes might still have a big role but this nation must now look to chart its own course. For us to do that, Canberra must, and probably will, look to establish relationships across APAC and ASEAN. We are quite sure that none of the other large players in the region, including Japan, South Korea et al., feel quite comfortable with the notion of having China assume unchallenged leadership in the region, let alone the planet. We will probably look toward the other large trading block, the EU. Many forget that the EU is the second largest economy on the planet on a cumulative basis and they will likely have the same interests as ours in forging the relationships. A post-Brexit UK will also be an important trading partner, along with other Commonwealth nations, making it important for the government to put a new emphasis on a Commonwealth free trade agreement for and with the “ex-colonials” included. We will make the call that Australia’s relationship with China will probably deteriorate going forward unless it decides to change its values fundamentally. This will cause some economic repercussions in the short-run. If the sell-off in TWE (Treasury Wine Estates) is anything to go by, this situation is likely to get worse before it gets better. The way it gets better will rely very much on Canberra and the alternatives in terms of trade destinations, including the ASEAN countries and European markets. The FTA with the EU is still in negotiations but we do see recent trends as having the potential to catalyse the process. The EU is also in a position of being increasingly antagonistic to Chinese expansion, in a weird way thanks to Brexit. Since the UK was the one member that was pushing back on closer integration, this hurdle seems to have been overcome if recent outcomes from the Commissions meetings are anything to go by (the most recent of which is the issuance of common debt).

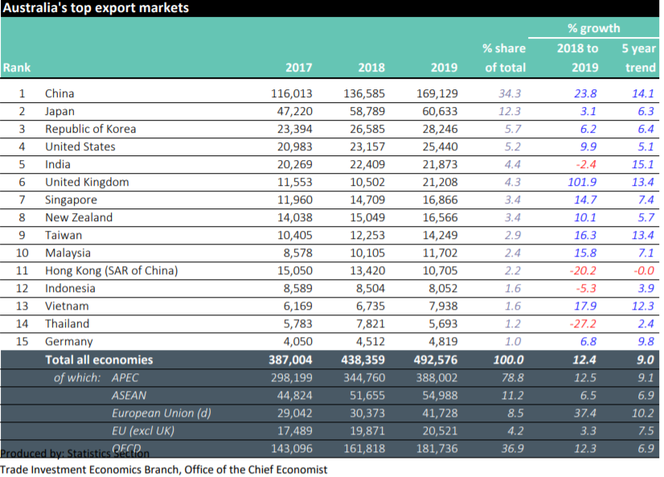

Source: DFAT

Note: Much will be contingent on changing the percentage of the largest export market to find alternatives. Just like an investment portfolio, there has to be diversification for a country's trading relationships.

The Hawkish Case

I am by no means a hawk when it comes to foreign policy, as I’m a tad old-school in believing that statecraft should be a gentleman’s sport (or lady’s). I remain optimistic that there are enough of them left in the world for us to move forward and pen some deals. One must not forget that unlike the US, which has a more insulated economy than one might imagine, China cannot operate in such isolation, despite less reliance on exports in recent years. To put it bluntly, the country has very little arable land and, additionally, is energy dependent on the rest of the world, making the building of cohesive alliances imperative going forward. One could, for example, argue that the Chinese states' increased dominance across the South China Sea is purely a result of oil and fish (securing energy and protein supply chains, not expansion for expansion’s sake). For further understanding feel free to look at what might be termed the second scramble for Africa and Chinese investments in Iraqi oil assets.

Australia, the lucky country, is lucky on this front when it comes to China. In the immortal words of Aretha Franklin’s Respect: “What you want / Baby I got / What you need / Do you know I got it?” We, along with Brazil, make up 70% of the world's iron ore supply, something that will be essential for the Belt and Road initiative as well as additional infrastructure. And so we arrive at the very next lines of the aforementioned song: “All I’m askin’ / Is for a little respect ...”. Some of the largest minerals and energy companies on the planet sit in this nation's jurisdiction or that of allies (even if some of them have become unreliable in recent years). The irony is, we could have potentially avoided the import duties now placed on our firms (probably more to come) if we had allowed more Chinese FDI into agricultural and mineral assets over the years. This would have allowed enough capital to be tied up for tit-for-tat (or at least the threat of) compensatory measures, especially those of state-owned companies which we could theoretically have threatened to seize... for national security purposes of course. Just as the duties on Australian wine were theoretically to prevent dumping; how selling at a premium is considered dumping is rather baffling to us, but economics is rather different for the CCP! No point rehashing the past though.

Going forward, it will be contingent upon our policy makers to make allies and create an alternative economic and security bloc. Through this process however, there will be certain sectors, including agriculture, that may need to be protected from punitive measures while alternative destinations are sought. Consumer discretionary goods, including the likes of Breville, are feeling the pinch on both sides, including US tariffs, but if the Commonwealth finds ways to navigate and create alternative markets, we could continue to mitigate the impact. Basically, the answer to the question of what the future might look like for Australian trade and industry, is that it depends on whether the Commonwealth Government moves quickly enough to 1) diversify our trading partners and 2) build relationships in a post-Brexit and post-pandemic world. One thing is for sure, the undisputed (for lack of a better word) leadership of the planet is vacant for the first time in three decades (the last time it was an actual dispute was the Cold War). This nation's future depends on helping keep it leaderless because the alternative may only suit one nation, and this nation isn’t quite so obsessed with the concept of freedom as the last.

Companies, especially the majors including the miners like BHP and Rio, will undoubtedly be part of any future formulations of policy. If you think this is too much of a stretch, consider the recent play by WPL to block Lukoil from taking a stake in the Sangomar project. Though in that instance it was to de-risk the project given US sanctions against Russia. ASX management teams will have to be a lot more cognizant of geopolitical risk going forward and the government will have to use certain sectors and industries as a means to achieve broader policy outcomes. Including this nation's large endowment of natural resources. For example, a trade deal with India, which has a closed off retail and banking system, could easily be negotiated within the context of that nation’s deficit in energy. My thoughts? Their access to Australia’s refined petroleum (and potential redirection of LNG and uranium exports) could be contingent upon their opening up to Australia’s grain exports and FDI into the banking system. In a similar manner, the creation of new trading blocs will have to take into consideration such nuances, based not just on economics but also security. OPEC is not made up of superpowers but nation-states that control the supply of an essential commodity. From an investors perspective, Geo-Political risk as a metric just got a whole lot more important. There will be winners and there will be losers through this whole process. The winners will be the audacious, as an example, feel free to look up the Australia-ASEAN Powerlink, a risky proposition but the benefits of which could be exceptional. If that is a taste of what is to come, this might be the wake up call Australia needed to finally accomplish Keynes’s dream of establishing a leader-free world of equal nation states.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim