|

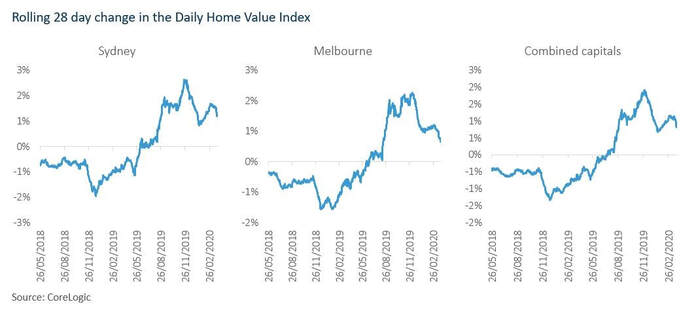

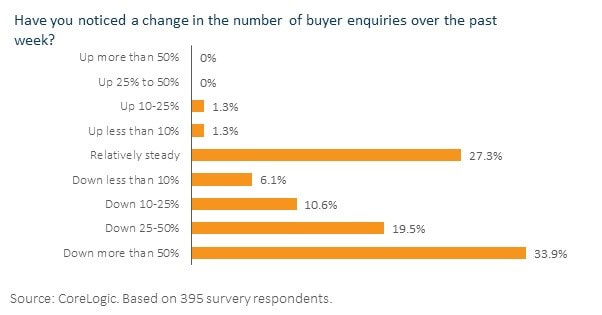

This week we would like to visit the topic of property. Given the unprecedented events of the past month and rapid changes from both the monetary and fiscal side of the equation, we would like to try and grapple with some likely outcomes. Something that is particularly relevant given our exposure to commercial and, more specifically, retail property. Before we start, we might mention that the exposure to supermarkets in our TAMIM Property trusts is keeping us reasonably steady through this all. Again, as seems to increasingly be the norm, the data gets ahead of us constantly. With changes taking place every day and government policies seemingly being made on the fly. Let’s begin with housing, something that remains the single-most important component of Australian household wealth. With unemployment figures likely to reach over 11% in the coming year, this poses an threat not only to the market broadly but the policy environment. We would say that recent policies introduced by the federal government pertaining to a moratorium on evictions are just the beginning. The exact details differ state to state. NSW being the front-runner, announcing a $440m relief package for both tenants and landlords impacted by recent events. The eligibility test is that the tenant would have to prove a on third decrease to their income. In which case a moratorium of six months is applicable, rents are to be renegotiated (reasonably) and the tenants are not liable to pay the differences after the moratorium. Queensland likewise has a six-month moratorium on evictions with any disagreements being referred to the Residential Tenancies Authority for Remediation. South Australia is similar in terms of the longevity of the moratorium but unfortunately no clarity on whether the rent differential is to be paid in full by the tenants following the expiry of the six-month period. Victoria, so far, doesn’t have a policy. WA is still in the process of enacting laws while Tasmania introduced a 120-day emergency period and 90-day extensions under which tenants cannot be evicted under any circumstances unless by mutual consent. ACT and NT have enacted laws without any compensation. So that brings us to our first point. We remain firm believers in the Commonwealth and the rights of states to have freedoms in determining their own laws when it comes to property but it is questionable whether such differences in both the policy and implementation is effective or justifiable given the present situation. We are already seeing repercussions in not only dislocations within the broader market but uncertainty about the status especially when it comes to landlords who often depend on rental yield for a significant portion of their livelihoods. It is one thing to be irritated by changing drivers license every time we move to a new state but this is rather different. CoreLogic’s daily index is already showing a marked decline in rolling 28-day growth with predictions that it will fall into negative territory in the coming days.  Source: CoreLogic We would argue that this does not present the full case though. Properties, being illiquid assets, have exceptionally sticky prices in the event of a downturn. Rather than values being indicated by the buy-price, the market simply freezes with neither buying nor selling happening. To give you an indication, refer to the below graph from CoreLogic around the number of enquiries with regards to residential property over the past week. The vast majority of real estate agents seeing a decline with close to 34% seeing declines of 50% or more. We doubt that there would be many sellers in this environment unless it is forced.

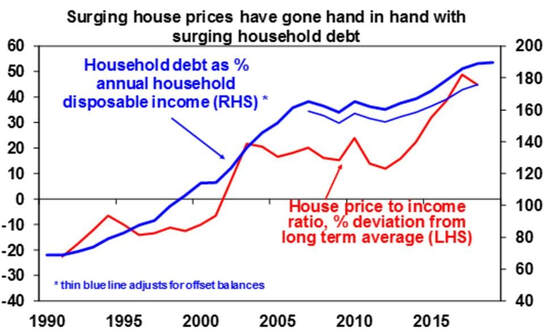

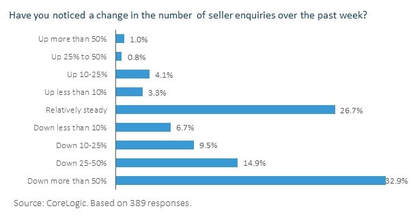

Source: CoreLogic Another way of saying it is this, if there are no buyers or sellers in a market, there is simply no price discovery. Thus, in the short run the key determinant for the broader economy is not the capital growth story but the shift from a yield perspective. The feedback loop created in terms of bad-debts and an inability of landlords to service their debt will have ramifications both in terms of credit markets and the stability of the financial system. Given that price growth within the property market has been driven primarily through credit growth and the accumulation of household debt (combined with stagnant wage growth), this is especially relevant.  Source: OECD, RBA, AMP Capital  Perhaps a buying of Residential Mortgage Backed Securities (RMBS) by the RBA is in the pipeline?

We would expect that governments take a logical approach and deal with the factors they can control, including property tax and council rates, which will provide immediate relief to the market. This, as well as helping landlords who take a proactive approach to the situation by giving rent-relief, should help. There is no reason for either tenants or owners to be paying disproportionately for a situation not of their making. More specifically, it is likely that the hardest hit will be the high-end luxury market, which tends to be non-performing in scenarios of equity crashes, and the bottom-end with blue-collar workers feeling the brunt of the stress via unemployment and low/stagnant wage growth. Middle-class suburbs should hold steady. In terms of the numbers however, it could be anyone’s guess. In the past we could go by history and look at previous market crashes, such as that of 1987 when it didn’t really impact house prices all that much or the GFC where a 55% drop in equity markets correlated with a -7.5% drop in property prices. We do not however have precedent for a situation where the economy is effectively shut-down and unemployment could potentially hit double digits. That brings us to commercial property. The hardest hit during this time have been SME’s and we have been seeing distress, with both frontline retailers and cafes being forced to go out into hibernation. From an overall property perspective, we think that there will be long-lasting implications. Not only has the situation caused irrevocable damage to some businesses who are likely to never reopen but it should create increasing headaches for property managers and owners of commercial property. The most obvious cases have been the likes of Scentre Group, GPT and SCA. Dare we say there will be more distress in the unlisted space as well given the increasing amounts of leverage that has been taken onboard. From our perspective, we continue to work with the small businesses that operate within our own retail centres (anchored by supermarkets and with specialty tenants like pharmacies and medical centres) to create mutually beneficial outcomes. However, here we would like to add that the devil is in the detail. Landlords again cannot be expected to take the full hit especially when the closing up is a choice as opposed to a necessity. A lease is, after all, a lease. For example, we continue to see foot-traffic in the news agency at one of our properties, Elermore Vale Shopping Centre. Thinking outside of the box, we have repurposed one vacant shop to be used as an overflow/waiting room for the medical centre when necessary. We think that businesses can continue to come up with creative solutions whether using take-away only for cafes, for example, or strictly enforcing social distancing when customers do wish to be in store. If they do make it a choice to close, it should not fall upon the landlords to take a total write-off. Again, we cannot forecast or reasonably estimate what impact it will have on underlying values given the diverse regulatory environments across the country. But from firsthand experience from deal-flow, we can say reasonably that the market is holding rather steady with no firesales (yet). Though again, the yields are the big question mark, we expect that recovery is going to take longer and the thing to watch as indicators will be the actions of the listed players. What will also be interesting is whether lasting implications come through in changes to behavior. For example, businesses that have taken to working online through this period may have seen some benefit to working mobile. How does this impact commercial office space in the future? Are we likely to see a marked shift towards less of a physical footprint? Similarly, from a purely retail perspective, we have continued to see the shift towards e-commerce and online. One important question to ask might be whether this will change consumer behavior over the long-run. As an example, a lot of consumers that had previously been light on online shopping have been forced to do so over the past month or so. Do they end up being converted? And if so, how does this impact the future of retail property in spite of the move toward omnichannel experiences. As for us, we have gained several valuable lessons through this process. The most important of these is the behaviour of different industry segments through crises situations. As we have mentioned and as you could imagine, having an anchor tenant like Woolworths or Coles with a consumer staples business is, we think, key to mitigating long-term risk when it comes to property. Yes, this might put downward pressure on the yield since the bargaining power tends to be with the tenant in this instance but we would rather be safe than sorry and lock in a steady cash flow to then have the ability to augment the yield in other aspects. Diversifying the tenant profile and going after more profitable specialty tenants. One of the key things we will continue to watch over the coming months will be the behavior of commercial office spaces and industrial property. In particular, it will be interesting to see what profile of spaces end up performing well and whether there might be opportunities arising as we may reasonably expect some forced selling to occur through the year. Whether it be existing owners re-capitalising or simply trimming down the leverage. We shall continue to watch diligently because the flip side of this equation is that for long-term investors there will be buying opportunities presented over the course of the year and into next year.

3 Comments

Tom Curtis

16/4/2020 05:06:36 pm

This is a really good piece which describes the risks for property investments and which properties might have been the most reliable in this market. 18/4/2020 12:42:11 pm

In NSW is there a mechanism to enable a commercial lessor/owner to get mortgage and statutory outgoings relief as a function of reduced rental income?

Sid Ruttala

20/4/2020 02:32:31 pm

Hi Tim, Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim