|

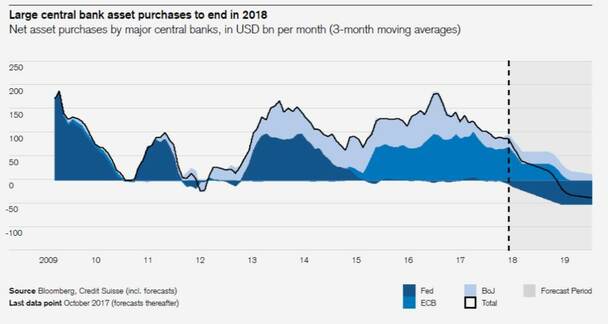

Robert Swift, Head of Global Equities at TAMIM and CIO of API Capital, takes a look forward at the year ahead. What can we expect to see? What would we like to see? How should we position ourselves?  In 2018 we anticipated a shift in sentiment to favour Value stocks and in our Global and Asia Pacific portfolios had a distinct bias to cheap stocks with a catalyst. However, rather than enjoying a simple shift to Value stock outperformance, there was a general and rapid sell-off in all equities in the fourth quarter, and we declined roughly as much as the global markets. We didn’t expect that. We had thought that the Fed’s shrinking balance sheet, which began shrinking well over a year ago, and the inevitable rise in interest rates had been well signaled and discounted. We saw signs of a resolution of the Chinese American trade dispute that would mean avoiding a mutually assured recession, and in Europe we noted the thawing in the Brexit negotiations and the Italian budget submissions. Excluding some of the more exotically priced stocks, which we tend to avoid, the P/E market multiples looked okay even with the expected decline in the growth rate of earnings that we see as both inevitable and desirable. We did not expect the rout that appeared. Our lesson learned? “Never underestimate the impact that the arrival of an event will have, regardless of how well you believe it has been signposted”. It seems another case of being ‘too early’ as a Value investor. If investors are paid to anticipate then this chart shows how a tightening of liquidity was apparent well over 12 months ago; at least to us. This is from October 2017.  We were expecting our diversified portfolio of stocks on low P/Es, with good balance sheets, and reasonable dividend yields would be more defensive than it was. We were disappointed to see our negative returns in line with the market. Our only big fundamental stock mistake was not to sell more, or all, of the Apple position over $200. The rest of the portfolio reported numbers in line with, or in excess of, expectations, but got sold off with the rest of the market.

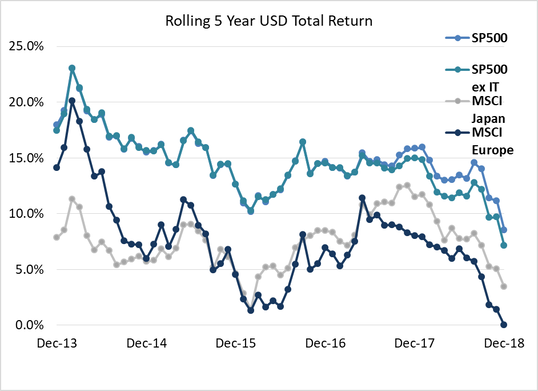

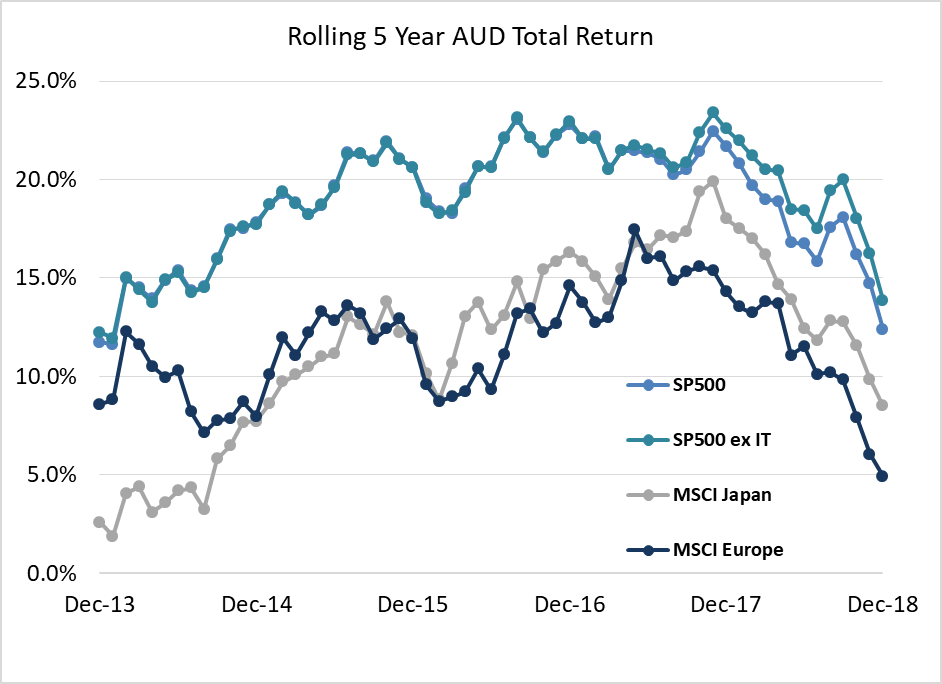

As we begin 2019 what do we anticipate and how are we positioned? We will make this brief because we know a lot of other ‘experts’ will be sending out their thoughts and email inboxes will be full. First we don’t try to make macro economic forecasts and so won’t be predicting a recession, or no recession. We won’t even state a predicted GDP number for 2019 and beyond. Equity returns have no relationship with nominal GDP, so the consensus for a slowdown in global growth in 2019 may not matter? What matters more for equity returns is starting valuation and the absence of inflation and regulation/confiscation which are the real killers of bull markets. Many people are arguing that we are about to see the end of a decades long bull market, but we would argue that there have actually only been ‘normal’ returns for the vast majority of markets and stocks. Strip out the IT Sector (which contains the FAANGS) from the S&P 500 for example, and the annualised returns drop from 15% pa to 11% pa in the last decade. This time period starts at the very bottom of the market and so returns are distorted upwards. In the last 5 years these returns from the S&P ex IT have been only just over 5% pa. For Australian equities the returns for many years now have been barely those from dividend yields at 5% pa. Europe and Japan similarly are hardly coming off an unusually strong bull market. The strongest returns for equities on a rolling basis in recent memory were those from the USA in the 1990’s when the market returned 30% pa for 5 years. We are a long way from that ‘irrational exuberance’ now and so the panicked calls to ‘exit risk assets’ are wrong.

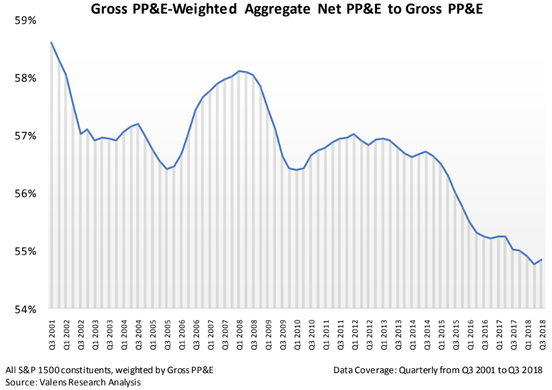

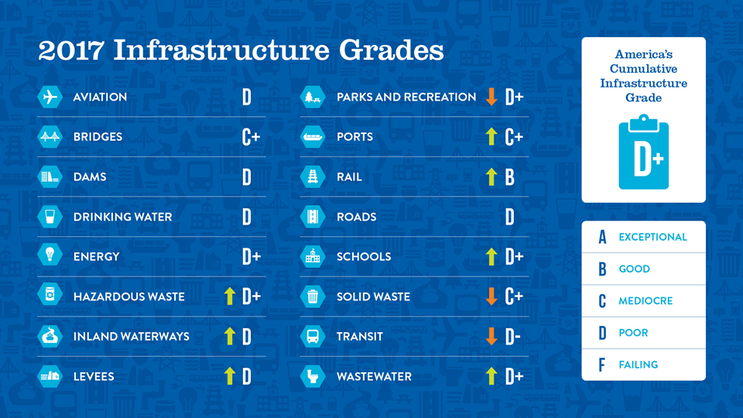

There is not a super bull market that needs to come to an end as a consequence of monetary policy tightening. Calling for an “end to the bull market” could more precisely be seen as calling for an end to the price momentum of the very highly rated stocks? We agree with this! Actually it is the ending of the monetary experiment that may very well provide the grounds for a sustainable level of global growth. 1) Liquidity will continue to be squeezed, or even the mere threat of further restrictive policy, will hang over capital markets. All central banks are now suggesting they will bring an end to easy money. All lending banks are under pressure to avoid irresponsible loans to consumers. Company management have spent years buying back shares in preference to physical re-investment. There is a clear need to end the monetary experiment which has resulted in the assumption of vast amounts of debt and severe under investment. Deflating the asset bubble souffle is not going to be easy or painless. As a result of the monetary incontinence there is a lot of debt that needs servicing in one way or another and this will be more expensive as liquidity is squeezed. To misquote Winston Churchill, “Never in the field of economic endeavour has so much money been owed by so many to so few”. It is unlikely that all debts can be serviced let alone paid back. There will be debt defaults and debt forgiveness required, as well as some serious currency realignments, at least in real terms; and yes, some tax changes. We have just had an unprecedented monetary experiment and we now expect this to be wound back. This unwind is also unprecedented by definition and so it will not be easy and nerves and volatility will be elevated. Consequently we favour companies and countries, with good balance sheets where the debt maturities are staggered, where cash flow net of capital investment is positive, and the asset backing is decent collateral. We like companies that pay dividends and are happy to increase them. In short we like creditor nations’ bonds and currencies such as China, Singapore, and much of the Middle East, and companies like Verizon, Ping An, Singapore Tech, Apple, and AFLAC. Germany is also fiscally strong but its assets are those of the indebted Club Med countries. For more of this please see below. 2) Fiscal strength and balance sheets will increasingly matter as investors decide what to buy or sell. Companies which invest in plant and equipment and R&D may become favoured. This fiscal strength will matter for companies and countries. For too many years, with the exception perhaps of China, public and private capital investment has failed to keep pace with capital consumption or depreciation, let alone increase in line with population or GDP. If you don’t invest as plant and equipment becomes obsolete, then the productivity of the equipment falls and you lose competitiveness and productivity. Since dividend growth is firmly linked to productivity, capital investment is necessary and desirable for equity investors. The chart below shows the trend in USA investment where a falling line indicates investment running below the rate of scrapping or depreciation and a rising line the opposite. Enough said?  So is the USA, Europe or Asia best placed in this regard? President Trump continues to demand that American companies invest in America and in this regard he may be right. For many years the market disliked reinvestment of cash flow and preferred share buy backs and rewarded the latter and penalised the former. It seems wrong to us that a share repurchase which is a sign that management can’t find new projects, and that directly benefits management compensation, is better favoured by policy makers and investors, than physical re-investment. Investment is obviously risky in that it might fail to live up to expectations, but without capital spending there can be no real growth and no maintenance of a competitive position. We believe the need for physical investment becomes apparent and even favoured in 2019 and a positive market theme. Share buy backs may become less desirable, less common and even the subject of a taxation review? Companies that have the cash flow and balance sheets to invest should therefore become favoured. This would be a significant and beneficial change from the last few years of over reliance on easy money. It won’t be without consequences for earnings growth however and this is because the visibility of earnings will fall as depreciation charges increase and the possibility of mal investment has to be factored in. Nonetheless, without any increase in physical or R&D investment, real growth will slow further. So we believe it becomes a market debate during 2019. Likewise the countries that can mobilise public spending quickly and without further stretching debt to GDP ratios will be favoured. Those of you who have attended our presentations have seen this chart below of the report card on USA infrastructure provided by the American Society of Civil Engineers (see more here).  Source: A.S.C.E. It seems pretty clear that USA infrastructure is dilapidated as is much of it in Europe. This would seem a good place to start a fiscal programme? As always the USA tends to do the right thing after exhausting all other possibilities, to borrow from Winston Churchill, but with Democrats in the lower house and Republicans in the Senate, it would be the triumph of hope over experience to expect a coordinated and funded public infrastructure plan in 2019? In this regard Asia seems very well placed to us in 2019 even as growth slows. Listed companies are well capitalised and can re-invest; the household sector reasonably leveraged and able to buy goods and services; and the Asian governments sufficiently able to cover any nasty state owned enterprise ‘shocks’, while continuing to expand public transport, the power grid and schools. They are also less encumbered by the democratic and time-consuming process of planning consent? This is not true for much of the rest of the world.

Currently Germany’s Bundesbank owns almost $1 trillion Euros of paper which represents claims on fiscally weak European companies and governments. The Italian threat to exit the Euro made in 2018 would have repercussions on the German banking system. They are all in it together. We anticipate compromise in the EU but the UK should leave this mess. It needs to retain control over its own economic policy levers and fiscal consolidation in Europe will prevent this happening while it remains bound. 2019 may be the year that the structural flaws in the Eurozone and EU are resolved one way or the other? We hope that there is no melt down. There is no need for one. We ‘merely’ need the Germans to agree that some form of debt forgiveness or relaxation of budgetary constraints is necessary. If this happens in 2019 we will have moved from ‘denial’ to ‘recognition’ to ‘action’ – all very positive. It is not however our central case and so we remain underweight Europe. Consequently we like Value as a style and we like Asia as a region. Value has underperformed Growth for longer than and greater than usual, and the difference in risk premiums is now too wide. We also like Asian companies particularly smaller ones which are less well researched; much cheaper than large cap growth companies; and somewhat immune to any repeat of a trade war, in that they rely on domestic Asian demand for revenue rather than any global supply chain or exports to the USA. Consequently in Q4 of 2018 we launched the TAMIM Asia Smaller Companies Fund. (This is a wholesale trust with monthly liquidity and available to qualified investors. We recommend a 3-5 year horizon.) We titled this ‘The Great Re-Set’. It will be a year of change but we can be optimistic. We have to see government monetary policy re-set; companies re-set investor expectations for capital investment and long term planning rather than share buy-backs; and for countries to re-set their approach to exports and imports and realise that under fair trade, all will benefit. We also need to see an effort to reduce wealth inequality exacerbated by the “monetary policy for rich people’ of the last 15 years. What this means is that equity returns from here will be vulnerable to mis-steps in tightening liquidity; the pain in reducing the size of current imbalances (deficits, debts, and unfunded obligations), and the ability of politicians to understand and navigate the ‘populist’ movements which are born from wealth inequality and the recent inadequacies of politicians to deal with the issues of ordinary people.  Importantly, as part of the Great Re-Set in 2019, we hope that investors re-set their expectations for returns. 8% p.a. from here on is the sort of number we should be expecting from equities. This is a good number and with inflation at maybe 2% or so, represents an historically solid real rate of return. If you stretch for more by using leverage, or high risk expensive investment vehicles, be prepared to lose. We don’t expect to be contacted by President Trump for advice but would like to request 4 things from him in 2019:

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim