|

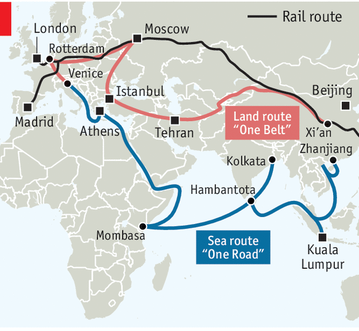

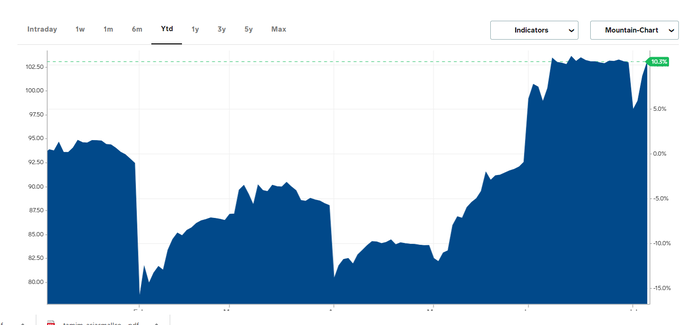

Sid Ruttala delves deeper (pardon the mining wordplay) into Australia's largest export, iron ore. Looking at the future of both the supply and demand side and what this means for mining stocks in Australian's portfolios going forward. Is there a substitute for the banks in there?  Author: Sid Ruttala Author: Sid Ruttala Whether one likes it or not, iron ore is this country's largest export. Currently, it is a commodity that is central to our economy and our collective futures. Recent trends have created a rather bullish scenario, holding up our currency and creating catalysts for the likes of Fortescue Metals (FMG.ASX, which we held until quite recently). More than this, the dividend yields across the iron ore majors make them a viable substitute for the financials given the ever-decreasing net interest margins and the uncertainty of dividends going forward. But where to from here? Is it worth having exposure to this commodity and which companies are likely to benefit? Before we begin though, let me tell you some news that hasn’t necessarily been on everyone's radar recently (who can blame you, there’s A LOT of newsworthy stuff going on around the world these days). Torrential rains in China have resulted in water levels in the middle and lower reaches of the Yangtze River (as well as Dongting Lake) rising as a result of the sustained rainfall. A total of sixteen rivers have been struck by above-warning-level floods and the Three Gorges Dam is under pressure. As of today, the continuous rain has affected 20m people in twenty-six provinces; nearly 20,000 houses have been destroyed and over a thousand reservoirs flooded. Why is this important for iron ore I hear you shout from the back? Let’s come back to this after exploring a little more of the context. But for the more impatient amongst you, a hint. Think along the lines of which sectors iron ore and steel tend to go into. And what damaged infrastructure means. The Three Gorges Dam and the twenty-six provinces (including Wuhan and Shanghai) are, by the way, contributing roughly 30% of China’s GDP.  Some Context (apologies to those well-versed in the ins and outs of iron ore) Iron ore is not a rare commodity by any means, it makes up about 5% of the Earth’s crust. What is rare is the combination of concentration and quality to make mining it commercially viable. And Australia has by far the largest known reserves, followed by Brazil and Russia. In fact, of global production, Brazil and Australia make up 70% of output. These countries are obviously vital to the supply chain. On the demand side of the equation, 98% of iron goes into steel production with China dominating this industry, as many of our readers will be well aware given the Trump administration’s (or is it mostly just his?) rhetoric around this particular issue. In terms of more specific numbers, close to 53% of global steel production is presided over by China, with India coming in a distant second. Asia together makes up over 80% of steel production. In turn the steel is predominantly consumed by the construction sector with the vast majority going into heavy infrastructure followed by automobiles, machinery and other metal products. As a result, iron ore prices tend to be exceptionally pro-cyclical and often driven by underlying consumption. What has held up iron Ore prices in recent years is the surprisingly resistant steel production in China, with even post-Covid demand falling by just -0.5% and expected to be slightly positive going through the second quarter of this year. If one considers ex-China production, the numbers are a little more concerning. That is, if you can call falling by close to -20% (vs -0.5%) a “little” more concerning. Despite the negatives on the demand side of the equation, spot prices have been pushed up by the supply side of the equation with a fall in Brazilian production. For Brazil, years of bad policy environments and under-investment in dam infrastructure has meant that Vale S.A. (VALE3.B3, VALE.NYSE, also listed in Hong Kong, Jakarta, Paris and Madrid). hasn’t had the best of times in terms of production and output. The Post-Covid environment has also seen a lack of proper policy action by the Bolsonaro regime, South America’s very own take on the Trump administration. Brazil’s President Jair Bolsonaro has, until quite recently (after himself testing positive for the coronavirus), insisted that Covid-19 was a non-issue. He has been using hydroxychloroquine on himself as a pre-emptive measure as well as leaving it to God (who, of course, is apparently Brazilian) to handle the situation. All creating a rather bearish production scenario. Recent events have also meant that there has been a shut down in mining across the production regions. Though the expectation is that Vale will be back to its usual output over the next six months, given their centrality to the Brazilian economy and the currency all together.   Source: The Economist Source: The Economist Our Baseline Expectation Again, as we have consistently mentioned, we are by no means banking on a V-shaped recovery in underlying consumer demand, whether one looks at automotive or machinery sales. But we do expect iron ore prices to stay steady at very least at current levels, even with Brazil coming back online in the next eighteen months. So, why do we expect this to be the case? Simply put, fiscal incentives across both China and the West. Even Germany, the last hold-out against aggressive fiscal expansion, has folded. We expect government spending, across both infrastructure and direct spending, to increase drastically. The lead up to elections in November almost makes it a certainty that the Trump Administration will hike spending on infrastructure. Would anyone be surprised if projects were rushed into the construction phase as much as possible given the way this administration operates? There is a very real incentive to move towards the US$3tn spend proposed by the Democrats as opposed to the US$1tn proposed by the Republicans in the run-up. Should the Republicans take the White House once again post-November, the numbers in the Senate (should the Democrats take it) are likely to make further spending boosts a likelihood. Should the Democrats have the Royal Flush and take all three (Senate, Congress, and the White House), then we may as well start talking about an infinite budget. In China, although the export market for steel is likely to come up against hurdles in the short-run due to the current policy environment, the party has a target to hit (6% growth) and it will do so whatever the cost. Direct intervention in terms of the construction of infrastructure is a given, the leaders (and authoritarian regimes in general) do seem to love their mega-projects. The Three Gorges Dam at normal capacity, for example, is big enough in magnitude to shift the orbit of the planet (look it up, it’s truly incredible). Briefly returning to the context of the flooding, the rebuilding process will create some short to medium term demand. There is also the likelihood of further direct stimulus to support the automotive industries, though this element is likely to be impeded in the short-run. In addition, the elephant in the room is the OBOR (One Belt One Road) initiative which should sustain demand for an extended period. One cannot forget the magnitude of this initiative; currently stretching across seventy-odd (70!) countries with a significant portion consisting of rail and road infrastructure, creating a massive catalyst for iron and steel demand. This is not to mention the injection of additional construction and development that will inevitably boost the hubs of this network. This particular initiative is essentially a put on iron ore prices  Iron ore price, Source: Business Insider  Source: DailyFX Note - The above graph’s give an idea of the correlation between AUD and Iron Ore prices What about Geo-Politics? The one sentence summary? Australian iron ore exports are safe, at least for the foreseeable future. Despite Chinese officials doing their best to ramp up rhetoric at our government’s rather rational calls and the United States’ flexing its muscles in both trade and military spheres (most recently, the moving of two aircraft carriers into the South China Sea), this country makes up enough of the supply side that one cannot simply avoid Australian ore without economic ramifications. There might be a concerted effort to diversify supply lines but the only viable alternative, Brazil, is itself not much better when it comes to rhetoric or action (despite its trade surplus with China). One also has to be cognizant of the fact that Brazil is the US’s backyard so to speak and South America has long been a region which the US considers to be within their sphere of influence, despite outside efforts such as those in Venezuela. Would the US prefer China establishing a further foothold in Australia, one of their closest allies (hooray, Five Eyes), or in Brazil, in their backyard. It’s a conundrum that one. We do see potential, perhaps in the very long-run, for China to take on or increase projects across Africa, especially countries such as Nigeria and the Congo - for those of you who still remember, Sundance (SDL) is an interesting story. One must remember that, even though China currently makes up the vast majority of global steel output, as it develops and moves up the wage curve, there is incentive for production to move towards lower-cost nations. The likely outcome being a shift to India and across South-East Asia, most of which (in the absence of incentives) are happy to buy from the lowest cost producers (back to status-quo). We are likely to see iron ore exports move increasingly towards India as a substitute to China. That being said, that particular nation is trying to build domestic capacity albeit still very nascent and nowhere near the volumes or grade of the Pilbara. This is especially relevant in the context of icy relations between the US and China (i.e the US increasingly likely to prefer imports of steel from India over China). There is also a shortage of iron ore in India which is trying to keep pace with its fast growing steel manufacturing industry. That said, the same cannot be said for Australian agricultural goods (primarily beef and dairy), education and wine which actually benefits iron ore exports since the upward pressure on the AUD as a result of increased iron exports is decreased by proportional decreases in other sectors.  Which Companies?

The investment universe when it comes to iron ore is surprisingly limited, which keeps it simple for investors. For one thing, the entire industry is close to an oligopoly with the big players - Vale, BHP Group (BHP.ASX), Rio Tinto (RIO.ASX) and FMG - dominating the sector. Of these, let's limit ourselves to the Australian listed entities. First let me begin with a disclaimer, iron ore is not a growth game, rather it is a margins game. The capital growth of FMG is an anomaly purely as a result of the company hitting its cost-cutting targets under a new CEO. Given the industry dynamics (i.e. consolidated production and fractured buyers) the pricing dynamics are a little more amenable to the producers. This sector should be considered primarily from a yield perspective. Unfortunately for the larger players like Rio and BHP, their diversified portfolio means that it is not necessarily a pure iron ore play. There are substantial issues related to lagging copper and base metal players with iron ore offsetting. BHP’s board and management, however, has taken the ex-China demand into consideration and have been rather conservative with capex (we feel). Copper production is likely to also disappoint due to structural issues and Covid related events. Rio is in a similar position with copper being the laggard and iron once again acting as a buffer for the group. Capex has, thankfully, also been flat and we expect them to be in a good position with ongoing M&A activity going through this year. This is most likely to be in the lithium space though. However, on a dividend yield of 5%, it remains an attractive proposition for ones’ portfolio. Looking at this from a risk perspective, BHP and Rio offer an attractive proposition for their diversification and, more importantly, their juicy dividend; it being unlikely that there will be any dividend cuts in the near-to-medium term. For those that want a pure iron ore play, Fortescue remains an attractive proposition though there is a substantial holding risk given the strong momentum in share price. It currently trades at a considerable premium close to 2.5x to NAV (at $15 p/share). However, it has a robust balance sheet with the primary risks coming from production and project execution ramp-ups at Eliwana. A post script on coal: The recent divergence between the price of iron ore and coal is interesting. Given that the manufacture of steel requires heavy input of coking coal, there has historically been a correlation between the two commodities. Right now, China is using its domestic supplies, and that from Mongolia, at a lower cost base. There might be a long-term play here, but it is not there yet. We would also require India, the second largest maker, to clean up its act.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim