|

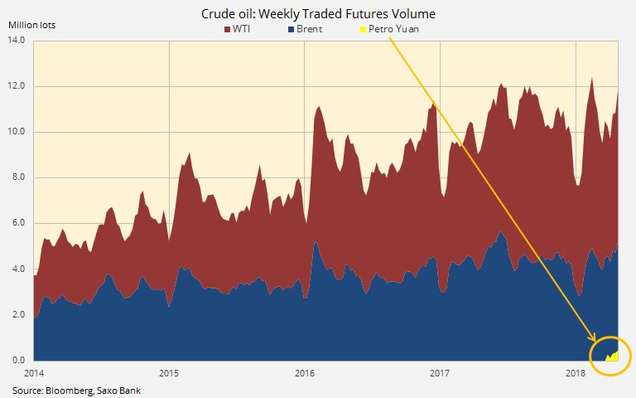

We continue our examination of global oil markets with Part 3 of the series Oil Markets - Evolution of the Body Politic. Click here to read Part 1 and Part 2. This week we continue the saga that is the evolution of oil markets and it seems to be a case of déjà vu. The price of West Texas Intermediate (WTI) recovered back to US$ 55.08 a barrel and Brent US$ 62 at the time of writing. Yet again, it was US foreign policy that led the way, a trajectory that started with the surprise production cuts by OPEC and was catalysed by a new round of sanctions, this time against the Venezuelan government of Nicolas Maduro. Initial reactions were somewhat muted given both the US State Department and US Treasury’s wording. Initially it was thought that the sanctions only pertained to US companies transacting with Petróleos de Venezuela, S.A. (PDVSA, the state-owned oil & gas company), however, officials confirmed that the sanctions would be extended to all transactions within the US Financial System thereby making the implications more broad ranging. Secondly, though Treasury Secretary Steve Mnuchin confirmed that the agency was taking a phased approach in order to enable US refiners to unravel some of the existing contracts, the government in Venezuela demanded upfront payments. This was intended to prevent non-payments or a redirection of payments towards the opposition (since the US has recognised the opposition leader Juan Guaido as the legitimate leader), thus leading to a build-up of inventories in Venezuela. All this has put upward pressure on the price of Oil despite a slowing in global growth outlook and a dovish Fed pivot. We would suggest that, notwithstanding another major geopolitical upset, there are no further catalysts for upward momentum within the current economic environment. The more likely scenario is a consolidation of price within the US$ 45-55 band in the medium term. As it currently stands inventories continue to build globally (refer to weekly inventory numbers at Cushing Oklahoma) and we would suggest that the Venezuelans will likely find a way to supply willing buyers at a deeply discounted rate. The sanctions against Venezuela again illustrate the sheer impact of US foreign policy on oil prices, something which is a direct result of its reserve currency status (which we’ve previously discussed). This week we would like to continue where we left off by looking at the Petro Yuan contract. Petro Yuan Contract In Part 2 of this series we outlined the nature of the relationship between the USD and Oil. In effect, despite the end of Bretton Woods, oil contracts continue to be traded and denominated in US currency. No doubt this has been helped by the historically close relationship between the Saudi’s and successive US administrations, whereby the Saudi’s and, after its foundation, OPEC countries continue to use the USD as the primary currency of trade and surplus’ would be recycled through the US financial system. The recent emergence of China has complicated this picture though. The Chinese government has made no secret of the fact that it would eventually like to see the Yuan as a credible alternative to the USD, beginning of course with the inclusion of the Yuan within a basket of currencies used by the IMF for the purposes of ‘special drawing rights’ in 2014. Though this didn’t gain the traction given the heavy government control of the financial system in China, the second and more recent strategy was the introduction of a new oil futures contract in the Shanghai International Energy Exchange, what we refer to as the Petro Yuan contract in parallel with the colloquial petrodollar.  The above move, though still symbolic and largely ignored by the mainstream media, is perhaps a taste of what is to come. It is well in line with other policy initiatives such as the creation of the Asian Infrastructure Investment Bank and the gradual build-up of regional geopolitical strength. Despite its significance, the policy is rather still in its infancy with no mention of it in the key National Development and Reform Commission documents that followed the pivotal October Party leadership gathering last year (perhaps one of the key reasons it has been overlooked). Ultimately, only 15.4 million barrels of Crude changed hands via the new contract, quite minuscule since the oil markets are US$ 14 Trillion in 2017 terms and amount to two days worth of imports for the Chinese. But given that China has officially surpassed the USA as the largest importer of Oil, it gives Beijing another tool in its arsenal in the case of an escalation of trade tensions. The Trump administration’s increasing tendency to weaponise the US dollar for the purposes of sanctions makes it likely that we will see a gradual uptake of the contract. Initially by countries directly impacted by the sanctions such as Iran, Russia and Venezuela (assuming no change in government) and more gradually could offer a credible alternative to the Brent and WTI contracts.

For the contract to gain further strength Beijing would have to trade-off with the scenario of lessening capital controls and strengthening the exchange market for the Yuan (essentially going towards a full free float). In the short-run there might not be an appetite for this to occur unless they move towards having the Yuan convertible against Gold in which case they might very well run up against the same problems the Americans did in maintaining sufficient reserves (something we spoke of in Part 2).

We think it more likely that as they continue to expand and make additional structural reforms pertaining to the clearing up of corporate debt there is a case to be made for a gradual relaxation of capital controls. At the very least, in the short run, it will allow them to circumvent US sanctions and buy at discounts should the dollar strengthen, given that countries with sanctions have no alternative.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim