|

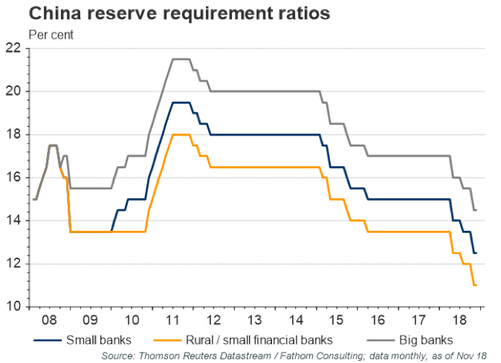

TAMIM Joint Managing Director Darren Katz takes a look at the financial world in the month of December and takes a brief look toward 2019. Welcome to 2019 and to the first update for the year. Before we review the last month and quarter and provide our thoughts on what is in store in 2019 I thought it would make sense to discuss two important lessons I have learned over the past 25 years. They both impact heavily on our ability to make money when investing. Investor Psychology One thing I have learned the hard way over 25 years of investing is that investor psychology has a big impact on how we invest and if we ultimately make money or not. One must not only be mindful of the impact on oneself but also how other market participants may be or are likely to be thinking and therefore acting (reacting?). Going through a very volatile market in December, I was reminded of how important it is to be calm when others (therefore markets) are not. For those that were able to look through the noise and buy when everyone else was selling, December was an excellent opportunity to buy companies at prices 25%, 35% and even 50% below where they had been trading three months prior. While I am not for one second saying that this is the end of the down leg in equity markets, there were/are certainly bargains out there as assets were sold off indiscriminately. Coming into October our absolute return equity portfolios held large cash balances which we began to deploy through December (and into early January). Across our relative return portfolios we were close to fully invested. Over long investing cycles these portfolios have and should continue to return strong results as can be seen in the ten year market returns in the table below. The Government Put Quantitative easing causes much debate in our office and I am sure this is the case in investment meetings around the world. Like it or not, QE did occur in 2008 and we are now dealing with the ramifications of the unwind. In an ideal world we should simply say ignore the consequences of the unwind and let it happen, the strong will survive. We do not live in an ideal world though and we are realists. As much as we would like to believe otherwise, governments worldwide are very vigilant around market volatility and asset prices falling. They will generally do anything in their quite considerable power to avoid significant losses in asset prices for the voting public. Stop for a minute and think about what you have seen in the last few months from a government response perspective: China - lowering bank reserve requirements to stimulate lending. USA - Trump jawboning Powell and Powells seeming capitulation (please do not be naive enough to thing the Fed is independent from the US government in any way). Australia - Frydenberg telling the banks to start lending and APRA removing the Interest Only bank hurdle. France - Macron suspending the fuel tax increase and providing increased tax relief for minimum wage earners. The fear of violent protests across capital cities will motivate a lot of government intervention and therefore the government put stays firmly in place and we should expect to see this implemented when financial markets get unruly.  Overview We may have passed the peak in the global growth cycle but we do not believe that a sharp slowdown in economic activity is imminent. Globally, growth will continue to be solid but not spectacular. Risks to this thesis do exist and are centred around the ongoing US-China trade negotiations and the possibility of a US Fed that retains a hawkish stance while continuing quantitative tightening. We expect that global market volatility will remain elevated in the first half of 2019 mainly as a result of geo-political issues and quantitative tightening. Brexit and the Italian political position versus Brussels could also create issues however we believe their impact to be lower than the risks posed by trade and the Fed. As 2018 unfolded strong growth was accompanied by an increase in inflation measures. Growth then started to moderate towards the back end of the year and the global synchronisation we had experienced to that point started to unravel. Concerns around growth coupled with risk events such as trade tariffs ratcheting up, poor communication between the US and China, the Fed remaining more hawkish than the market could appreciate and Brexit deliberations heading towards an impasse created a de-rating of risk assets and equity markets around the world sold off aggressively. We believe the biggest impact on financial markets has been the withdrawal of liquidity through US quantitative tightening. The EU is expected to follow suit in 2019 (this may be delayed if markets remain weak) although they will continue to keep rates low. Recent commentary from Powell at the Fed has pointed towards a slower pace of rate increases or possibly even a pause. According to UBS, global growth is seen slowing from 4.0% mid-2018 to 3.6% in 2019, before stabilising at 3.7% in 2020. Similarly, in its latest November update the Organisation for Economic Co-operation and Development (OECD) sees growth of 3.5% in both 2019 and 2020. Both the US and Australia expect growth to slow below 3%. Better momentum is expected in Europe and Japan while China is expected to ease policy to stabilise growth at 6 to 6.5%. The moderation in global growth will test the resolve of central bankers world wide in their quest to normalise interest rates. Volatility and extreme market weakness will slow the normalisation process in our opinion.  The final quarter of 2018 was brutal for global and domestic equities. Despite this, when viewed over the long term (in this case 10 years), returns across equity markets in local currency terms remains strong. The sell down across global indices was as follows:

Despite the ~ -10% drawdown in equity markets globally in early February 2018, markets were strong through the first nine months of 2018. The S&P 500, for example, was up around 9% to the end of September. It then fell -17% through the final quarter of 2018 (the worst quarter we have seen since 2008) before a late December rally of about 4.5%. Australian Equities The Australian economy grew a seasonally adjusted 0.3% in the September quarter, slowing sharply from a 0.9% expansion in the previous period and missing market consensus of 0.6%. This was the weakest pace of expansion since a contraction seen in Q3 2016, mainly due to a sharp slowdown in private consumption and a pull-back in non-residential construction. Australian equities (ASX 200) outperformed global peers in Q4, “only” declining -8.2% to finish down -2.8% for the year. Small Caps fared worse, declining -13.7% for the quarter and -8.7% for the year. All eleven sectors were in the red, with financials and energy, driven by sharply lower oil prices, faring the worst. Materials supported by strong iron ore prices fared better. Forward PE ratios are currently 14.1x, just below the long term average of 14.2x. The earnings outlook for Australian companies is less compelling than their offshore counterparts, which offer greater exposure to faster growing secular trends such as technology and healthcare. After 23 years of no recession, the lucky country may be running out of luck. Slowing growth will be exacerbated by slow credit growth, some would argue the strangulation of credit growth as a result of two years of policy moves to try and reduce the high level of Australian household debt. Couple this with increased scrutiny through the Royal Commission on Australian bank lending standards and we have seen credit growth grind to a halt. Recent comments from the Treasurer encouraging banks to lend, the removal of the cap on interest only loans on the banks on 1 January and APRA easing its macro-prudential rules may help ease the provision of credit. This does at least indicate that authorities are aware of the potential issues created by tight credit and are trying to counteract it (the government put?). Risks to growth do remain and this will largely depend on how hard the housing market corrects. A federal election in May and the potential change in government could see uncertainty weigh on a broad range of equity sectors, including health insurance, property, banking and utilities. Australian growth stocks have had an extremely good run until the start of the fourth quarter. The recent drawdown of growth-stocks was an extreme tail event which was helped along by crowded trades in companies which already looked expensive. We believe the last move down does offer attractive entry points to some growth stocks especially in the mid to small cap space but still also points to value as an attractive segment of the market with growth (high PE) stocks having outperformed value (low PE) stocks by the widest levels since the GFC. Growth stocks will display higher risk than others over the course of 2019 and investors need to be aware the following issues: weaker price and earnings momentum, large share issuance, high gearing, large goodwill balances, lower levels of profitability and valuations. International Equities United States Global market woes were triggered in October with Jerome Powell’s comments that the US policy rate was still “a long way” from neutral. This saw US ten year yields above 3.2%. In November Powell moderated his message saying that rates were “just below” the estimates for normal. At the December Federal Open Markets Committee meeting rates were hiked another 25 basis points however guidance for 2019 was lowered from three rate hikes to two. This was less than the market expected. Powell’s comments that the reduction to the Fed’s balance sheet was on autopilot spooked markets with sharp falls triggered in equity markets. This was exacerbated when Trump seemingly indicated he would fire Powell which cast doubt on the Fed’s autonomy. The Fed has since gone out of its way to reassure markets they will be acting on market data and reviewing the environment before making further decisions. Despite recent pullbacks yields in the US have continued to increase which, coupled with earnings per share growth falling from around 24% to mid-to-high single digits, means there will be a compelling reason for investors to view fixed income and cash as a viable alternative to US equities for the first time in years. We expect to see continue US equity market volatility in the first half of 2019 but still view US equities as a good opportunity over the medium term. Asia 2018 was the sixth worst year for the MSCI Asia after a 2017 which was the fifth best year. Company valuations will provide support to Asian equities with a price to book ratio for Asia ex Japan just off the 2016 lows at 1.28x. The Japanese market is experiencing similar with valuations at 11.2x well below the 20 year average at approximately the 20x level. Asia including Japan represents an excellent opportunity in 2019 given the large sell off across the December quarter. Despite the slowing growth rates, Asia still has the highest economic growth levels globally Less developed Asian markets will still need to see a positive outcome from US-China trade talks as well as evidence that Chinese fiscal and monetary stimulus is working. Chinese growth has slowed with imports falling from a level of 37% year on year growth in January to 3% in November. There has been a slow down in the pace of retail sales growth and industrial production. With a slowing of money supply growth following a further clamp down on lending by the shadow banking sector, Chinese authorities launched stimulatory fiscal and monetary measures. Europe Business surveys in Europe have been weakening all year but moved towards contractionary levels this quarter. This was contributed to by political tensions specifically in Italy and France. New export orders for Europe have slowed markedly driven not only by the trade slow down but also by political issues. Higher borrowing costs were the result of the Italian government's showdown with Brussels over its budget. This has been brought to a head with Italy submitting a new budget with a lower deficit. In France, President Macron has come under significant pressure from the yellow vest protests over the price of Petrol .This has caused an issue with business confidence. Macron has reduced duties and launched stimulus measures in an attempt to ease tensions. Targets by sell side analysts for European indices for the end of 2019 are close to levels from 20 years ago. Valuations on a PE basis are at 11.9x below the 20 year average of approximately 15x despite the quantitative easing program which has been in place since 2015. European equities have not been supported over the past 2 years and may offer interesting opportunities in 2019. Fixed Income The gradual rise in interest rates is likely to persist as global central banks look towards monetary policy normalisation in 2019 and 2020. The tug of war between growth and inflation will also persist throughout the coming year. This should create some volatility in interest rates and the end of QE in Europe is likely to add fuel to widening global credit spreads. The weaker Australian domestic economy, lack of wage growth and the momentum of a weakening housing market means the Reserve Bank of Australia (RBA) is expected to remain on hold through 2019. There is an argument that if the domestic banks come under further pressure on funding costs, causing them to raise rates out of cycle, then the RBA could in fact be forced to cut rates. Pre-election political uncertainty is also likely to put pressure on wholesale funding levels. We feel that spreads will widen (in both financial and corporate bonds) from the current low levels. Australian government bond yields are likely to outperform global counterparts (where rate cycles are hawkish) and offer a defensive asset class in volatile markets. We continue to favour private debt as the way to diversify portfolios as opposed to government or corporate debt. Conclusion

Putting together portfolios in 2019 will, as is always the case, be challenging. We continue to favour a focus on higher levels of diversification than usual with a preference for liquidity in the equity segment of portfolios. We also remain skewed towards value as opposed to growth as an investment style. We will however take advantage of broad based equity market sell offs to acquire good quality growth stocks at lower prices. As political risk in Australia increases alongside concerns around the housing cycle we are more interested in global equity than local, with an interest in listed Israeli equities as well as developed Asian markets to help keep portfolios diversified. We prefer to achieve our portfolio diversification through local exposure to private credit as opposed to government or corporate bonds globally and in Australia.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim