|

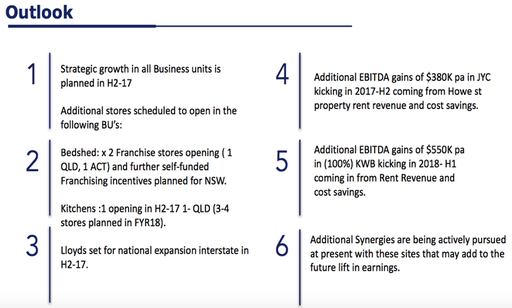

We take a look at the "shopping list" of qualities our small cap team look for in making an investment. They run through each and provide a stock example to illustrate their point. High Quality - A Shopping List Summary: Within our team we are focused upon investing in under-valued, high quality smaller companies. We are often asked how we define high quality so in this article we present our shopping list of attributes we look for in high quality businesses which we can invest in for the long term to generate superior returns for our clients.  Profitability & cash flows: The first deal breaker for us in the high quality search is whether a company is profitable and cash flow positive. In our minds profitability and positive cash flow generation are both core to what a business should be about, and thus we are not willing to speculate on loss-making companies which are aiming to more than cover their costs in the future. And it is not just the short term risks we are aware of: loss-making companies carry longer term risks far beyond the headline losses in our opinion. If a business is loss-making it often indicates an “empire building” mindset in management, poor strategic choices, structural problems with the business model, and cost mismanagement issues. This is obviously not always the case but in our experience the hit rate with these issues is high, and we are not willing to risk shareholders’ funds where these risks are high. When looking at profitability we are interested in comparing a company’s reported earnings with its reported cash flows. In our experience, it is common to come across companies where their reported earnings are significantly higher than their reported cash flows. The difference is usually explained by the company’s accounting choices. For example, we recently did some work on a retirement village owner and operator which looks very cheap on statutory earnings at around 8x this year’s earnings. However, when we analysed the company’s accounts it became apparent that much of this year’s earnings are coming from expected property revaluations and thus the company’s cash flows, and the profitability of the underlying business, are likely to be significantly lower. We decided the stock was expensive as a result. We are looking for the contrary scenario whereby reported earnings are below reported cash flows reflecting conservative accounting strategies. Companies which fall into this category tend to be led by management teams focused upon under-promising and over-delivering. STOCK EXAMPLE: Fiducian (ASX:FID) is a good example of a highly profitable stock in the TAMIM small cap portfolio which tends to report higher cash flows than statutory net profit reflecting its highly experienced and conservative management team. In its recent half yearly report operating cash flows was $3.6m versus a statutory net profit of $3.4m. Visible organic growth drivers: Next on our shopping list is companies which have clear and visible organic growth drivers which management can articulate. We often come across businesses which are focused upon capturing a macro theme or trend. When we read through their presentations we generally find many inspiring charts highlighting the enormous growth potential of this macro trend/theme. However, after reading such presentations we are often left wondering what the company actually does and why it will benefit from these macro drivers. This is not what we are looking for. We are looking for companies which have clear strategies in place to grow their businesses independent of macro trends. We’ll discuss business tailwinds later in this article (these are also on our high quality list) but we need to see clear organic growth strategies from management. And we also need to understand exactly what a company’s growth strategies mean in terms of day to day business activities. STOCK EXAMPLE: Joyce Corp (ASX:JYC) is an example from the TAMIM small cap portfolio of a stock with clear growth drivers looking forward. The following slide from the company’s recent half yearly presentation highlights 6 clear and visible earnings growth drivers in the year ahead – a big tick on our high quality list:  Source: JYC company filings Aligned management & family companies: We have previously written of our preference for companies in which management are personally invested, of which family/founder companies are a great example. Having “skin in the game” is a highly effective means of ensuring management are thinking of shareholders’ best interests at all times. The evidence is compelling:  STOCK EXAMPLE: Dental product supplier SDI (ASX:SDI) commenced operations in founder Jeffrey Cheetham’s garage, producing amalgam fillings and selling the products direct to dentists. By 1975, the company had operations in New Zealand, United States and Greece. Following a decade of national and international success, the company listed on the ASX in 1985. A strong focus on research and development has seen SDI develop an extensive portfolio of innovative restorative and cosmetic dental products including fillings, cements, tooth whitening products and associated dental equipment, with market leading positions in various geographies. We believe the company’s long term successes have been largely driven by the founder’s passion for and stake in the business. Strong balance sheet:There are many reasons why we like companies with strong balance sheets including:

STOCK EXAMPLE: A powerful example of a company with a strong balance sheet within the TAMIM small cap portfolio is Reverse Corp (ASX:REF). As at 31st December 2016 the company held $7.42m in net cash versus its current market cap of $8.6m. The market is currently valuing the company’s reverse calling and online contact lens businesses at a lowly $1.2m. We believe these two businesses are worth far more than this, and the company has the benefit of an extremely strong balance sheet which can be used to build the online contact lens business whilst paying very high fully franked dividends to shareholders. Business tailwinds:In addition to the organic business drivers already mentioned, we like to invest in companies with industry tailwinds behind them. In our experience, being in the right industry at the right time often makes it easier for a company to exceed the market’s earnings expectations. STOCK EXAMPLE: Paragon Healthcare (ASX:PGC) is a standout example within the portfolio. Paragon is a leading provider of medical equipment, devices and consumables to the healthcare market, and provides excellent exposure to the ageing population thematic. We believe the company’s organic growth drivers will be complemented and supplemented by this powerful tailwind in the years to come. Capable, trustworthy & shareholder friendly management:We spend a lot of time getting to know management in order to tick this final box on all our investments. We believe high quality management are even more important when investing in smaller companies than larger companies because each strategic decision tends to carry a higher relative weight in a smaller business. As a result, we will only invest in businesses with management who are:

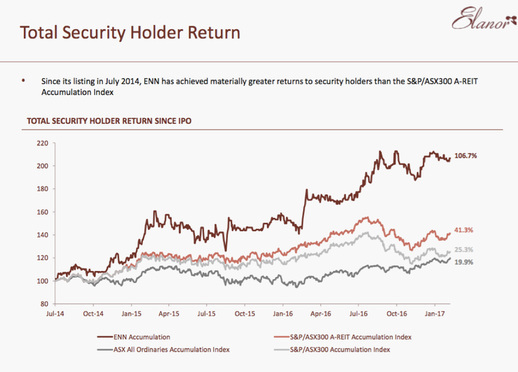

STOCK EXAMPLE: Elanor Investors (ASX:ENN) is an example of TAMIM small cap stock with highly capable, trustworthy and shareholder friendly management who are very conscious of total shareholder returns as per this slide from the recent half yearly results presentation:  Source: ENN company filings Conclusion: It’s a long shopping list and we are very picky. However, we believe ticking all these high quality boxes at the right valuation is why our clients invest with us. The lower the hit rate, the more repeatable and sustainable the process in our opinion. We will remain disciplined in our search for under-valued high quality smaller companies looking forward.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim